Project Finance International September 20 202364

FEATURES

Most US wind and solar projects qualify for

either an investment tax credit (ITC), which

is available when a project is completed, or a

production tax credit (PTC), which is generated

over a ten-year period starting when the

project rst becomes operational. The IRA

introduced signicant changes to accelerate the

energy transition, including extending existing

tax credits through the next decade, creating

new tax credit bonuses for projects in fossil

fuel communities and those that use domestic

components, and creating new tax credits for

emerging technologies, such as battery storage

and hydrogen projects.

But by far the most fundamental of the

changes that the IRA introduced is the right of

project owners to sell their tax credits freely in

the open market. Prior to the IRA, tax credits

could not be bought and sold. Instead, they could

be shared only by equity owners of projects

through structured joint ventures known as tax

equity partnerships. Now, most tax credits may

be sold in the market under a tax credit transfer

programme. This change and a detailed set of

regulations that the Internal Revenue Service

(IRS) released in June 2023 are shaping the

renewable energy project nance market in

the US.

Navigating the tax credit sale rules

Financing projects that will sell tax credits

involves new considerations and opportunities.

The rst is how best to structure bridge nancing

against the future sale of a project’s tax credits.

A second consideration is how project owners

can protect against the risk of ITC recapture,

as described below, which could result from a

lender foreclosure at any time in the ve-year

period after an ITC is claimed.

• Payment limitations – Buyers and sellers of tax

credits must follow two specic payment rules.

First, the payment must be made in cash. Second,

the payment must be made in a window of time

starting at the beginning of the year in which

the credit is generated and ending on the date

the tax return is led for the credit. For example,

if a ling is made to extend the tax return ling

deadline, the buyer is able to pay from January

of a given year up to midsummer (or later) of the

following year.

The inability of buyers to prepay for

credits effectively means that tax credit

buyers cannot provide bridge capital to

developers that have not yet earned their tax

credits. Project owners, therefore, turn to

banks or other capital sources to bridge to a

tax credit purchase commitment. In the case

of a sale of PTCs, the purchase commitment

will likely call for payment instalments to be

made over a period that could be as long as

ten years.

• ITC recapture – Although an ITC is claimed

in full when a project is completed, the credit

vests over a ve-year period, in equal 20%

instalments per year. If a project loses its tax

credit qualication status at any point during

this ve-year period, the unvested part of the

credit is recaptured and must be repaid to the

IRS. This rule applies not only to ITCs claimed by

project owners but also to ITCs purchased by tax

credit buyers in the open market. Recapture is

most commonly caused by a casualty event that

destroys the project, a systemic design failure

AFTER THE IRA – A NEW

FINANCING LANDSCAPE

AS WE PASS THE FIRST ANNIVERSARY OF THE INFLATION REDUCTION ACT, THE PROJECT FINANCE MARKETS

ARE BEGINNING TO COALESCE AROUND NOVEL FINANCING STRUCTURES DESIGNED TO MAKE OPTIMAL USE

OF THE NEW TAX CREDIT SUBSIDIES THAT THE US CONGRESS ENACTED. THIS ARTICLE EXAMINES SOME OF THE

KEY STRUCTURAL CHANGES IMPLEMENTED UNDER THE IRA, WITH A FOCUS ON HOW THESE CHANGES ARE

SHAPING THE WAY US RENEWABLE ENERGY AND ENERGY TRANSITION PROJECTS ARE CAPITALISED, AND THE

WAY PROJECT FINANCING FOR THESE PROJECTS IS EVOLVING. BY KELLY CATALDO, PARTNER, AND ELI KATZ,

PARTNER AND VICE-CHAIR, ENERGY & INFRASTRUCTURE INDUSTRY GROUP, LATHAM & WATKINS LLP.

FIGURE 1 - TAX EQUITY BRIDGE LOAN STRUCTURE

ECCA

Construction

loans

Tax equity

bridge loans

Sponsor

Parent

Class B Member

Tax equity

partnership

Tax equity

Investor

Lenders

Project company

(Borrower)

Project

Collatera

l

package

06 Features p64-68.indd 6406 Features p64-68.indd 64 19/09/2023 16:42:0619/09/2023 16:42:06

Project Finance International September 20 2023 65

IRA FINANCING LANDSCAPE

that renders the project inoperable, or a sale of

the project assets or equity during the ve-year

recapture period.

Historical structures

Historically, to raise capital for the construction

of projects, sponsors have obtained loans from

lenders and binding commitments from tax

equity investors. Tax equity investors typically

do not take construction risk and fund their

commitments only once the project has achieved

specied completion milestones. Tax equity

bridge loan (TEBL) facilities have become a

commonly used technique to raise capital against

a future tax equity commitment. The structure of

a typical TEBL facility is depicted in Figure 1.

Like a construction loan, a TEBL is drawn

during construction, used to pay project costs as

incurred and secured by all assets of and equity

in the project company. The TEBL is sized off of,

and repaid with the proceeds of, the tax equity

investor’s future funding commitment. As a

result, lenders focus on the credit quality of the

tax equity investor and any conditions to its

funding obligations.

Generally, a tax equity investor memorialises

its commitment in an equity capital contribution

agreement, which is signed concurrently with

or shortly after the closing of the loan facilities.

Once the project is operational, the tax equity

investor funds its commitment and repays the

TEBL. Any remaining construction loans are then

typically repaid with proceeds of a term loan, the

“term conversion”.

Tax equity investors generally do not permit

the tax equity partnership to have secured debt.

Accordingly, asset level liens are released at term

conversion. The term loan is secured by assets of

and equity in the term borrower, and the term

lenders are structurally subordinated to the tax

equity partnership. This structure is known as a

back-leverage loan, and the associated collateral

package is depicted in Figure 2.

Bridging to tax credit sales

• Bridge loans – Bridge nancing structures for

tax credits sales borrow heavily from TEBL

structures, but with signicant differences and

new considerations. Like the timing mismatch

that created the need for a TEBL, project owners

require signicant capital for construction before

tax credit buyers are permitted to pay for the

credits. Tax credit transfer bridge loan (TRABL)

facilities, which are sized based on the projected

sale price of the tax credits, can be used to bridge

this gap.

TRABL facilities for ITC transactions are

structurally similar to TEBL facilities, with loans

during the construction period repaid on a

lump-sum basis with the proceeds of the sale of

ITCs. Because the sale is not tied to construction

completion milestones, the repayment of the

TRABL, which depends on when the tax credit

buyer agrees to pay for the credits, may be

misaligned with when term conversion can

otherwise be achieved.

In contrast, repayments under PTC TRABLs

are likely to occur over a multi-year period

as the PTCs are generated and sold. Loans

will be sized against the projected aggregate

payments from the sale of credits, and repaid

on an amortisation schedule sculpted to

the PTC instalment payments under the tax

credit purchase agreement. Similar to ITC

sales, there will be a mismatch between term

conversion and repayment of the TRABL

facility for PTCs.

The lenders in tax credit sale transactions will

evaluate the creditworthiness of the buyer given

that they are bridging to its commitment to buy

the credits. The credit analysis for PTC sales will

be even more important given the long tenor of

the TRABL bridge. Lenders may insist on nancial

covenants and credit support to ensure their

source of repayment will remain creditworthy

over the purchase agreement term.

FIGURE 2 - BACKLEVERAGE LOAN STRUCTURE

Bank-levered

loans

Bank-levered

Lenders

Class B

Membership

Interest

Class B Member

(Back-leverage

borrower)

Class A

Membership

Interest

Class A

(Tax Equity

Investor)

Tax Equity

Partnership

Project

Company

Project

LLCA

Sponsor

Parent

Collateral

package

FIGURE 3 - PROJECT FINANCE VARIATION

Construction Collateral Package

Class A

Interest

Class B

Interest

Borrower Affiliate Partner

Project Company

Tax Equity Partnership

Lenders

Tax Credit

Purchaser

06 Features p64-68.indd 6506 Features p64-68.indd 65 19/09/2023 16:42:0919/09/2023 16:42:09

Project Finance International September 20 202366

While the mature TEBL market has settled

around a 95% to 100% advance rate against

a tax equity commitment, debt sizing in

the nascent TRABL market continues to

evolve. Debt sizing for PTC sales is further

complicated by the longer-term repayment

period, and the fact that PTCs – and therefore

the corresponding payments from a tax

credit buyer – uctuate based on a project’s

generation prole.

Some near-term projects may not have

arranged tax credit sale agreements at

nancial close, as the demand for construction

nancing is outpacing the ability of project

developers to source tax credit buyers on

attractive terms. Some lenders are advancing

TRABL commitments against the value of

uncommitted credits, at advance rates that

range from 50% to 75% of expected credit

value. Other lenders are requiring full

or partial sponsor credit support during

the period before a tax credit purchase

commitment is executed.

Structure and recapture – There are at least

two key variations on the conventional project

nancing structures discussed in the historical

structures section. The rst, depicted in Figure 3,

is similar to a conventional tax equity partnership

and is designed to avoid a recapture event if the

lenders foreclose.

Lender foreclosure on the assets of or equity in

the project company during the ve-year period

after a project is placed in service may result in

a recapture of the unvested portion of the ITC. A

recapture event would cause a tax credit buyer

to lose its tax credit and would likely trigger an

indemnity obligation from the project owner that

sold the credits.

In a conventional tax equity partnership,

after an ITC asset is placed in service, the term

lenders do not have liens on the investor or

on the investor’s interests in the partnership.

A foreclosure will be on the borrower or

on the sponsor member’s interests in the

partnership, which will not result in a

recapture of the tax credit allocated to the tax

equity investor.

To achieve a similar result in a tax credit sale

structure, the project owner may choose to hold

the project in a joint venture between the term

borrower and an afliate and allocate the ITC

to the afliate. The afliate’s equity and assets

are not part of the lenders’ collateral, thereby

avoiding recapture if the lenders foreclose on the

term borrower.

This structure is easily adaptable for a

tax equity partnership or tax credit transfer

arrangement. It may, therefore, be attractive to

both sponsors and lenders, because it provides

the exibility to toggle between a bridge loan

repayment from a tax equity investor or a tax

credit buyer.

For transactions in which this exibility is

desired, lenders and borrowers should determine

the base case assumption of the value of the

credits for debt sizing purposes, and provide

exibility for prepayments and incremental

borrowings to toggle to the correct advance rate

once the nal take-out structure is known.

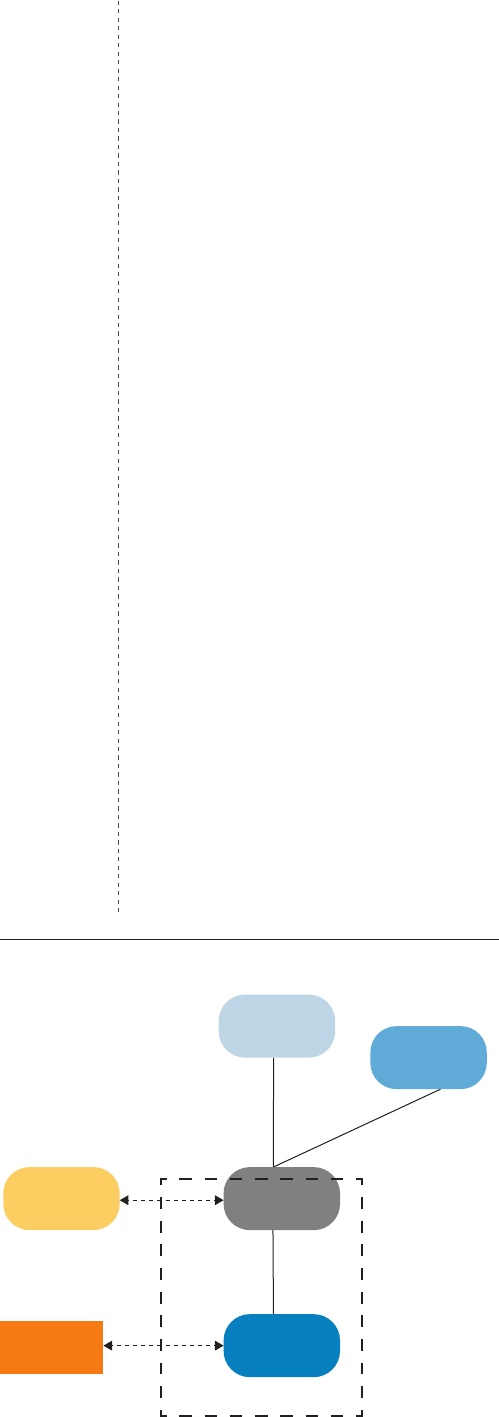

In a PTC sale transaction, in which tax credit

recapture is not a concern, the term lender may

negotiate to maintain asset-level collateral for the

tenor of the loans. One variation of this structure

is depicted in Figure 4.

This structure is more favourable for lenders

than the conventional back-leverage structure,

as it permits the lenders to maintain asset-level

liens throughout the term of the nancing, and

to remain structurally senior to obligations under

the tax credit transfer agreement. Lenders may

also require a pledge of the tax credit transfer

agreement and associated deposit account (for

example, if they are bridging to payments under

such agreement).

• Intercreditor terms – TRABL lenders will evaluate

certain due diligence terms in the tax credit

sale agreement, including remedies for under-

performance, liquidated damages for credit

shortfalls, and the scope of indemnities offered

by sellers. Lenders will attempt to ensure that

they are shielded from or have seniority over the

project owner’s obligations to a tax credit buyer.

Interparty agreements between the lenders and

tax credit buyers may provide certain terms that

apply prior to foreclosure (such as forbearance

and cure rights), and specify the lenders’ rights

to enforce the tax credit buyer’s commitment to

purchase tax credits.

Conclusion

The IRA has heralded new opportunities to

monetise tax credits and arrange project

nancing for renewable energy and energy

transition projects in the US. The nancing

landscape will remain dynamic as market players

adapt to new transaction structures that enable

optimal use of the new subsidy regimes.

n

FIGURE 4 - PTC VARIATION

Collateral Package

Borrower/Project

Company

Affiliate Partner

Sponsor Entity

Tax Equity Partnership

Lenders

Tax Credit

Purchaser

06 Features p64-68.indd 6606 Features p64-68.indd 66 19/09/2023 16:42:1119/09/2023 16:42:11