The Anatomy of Monetary

Policy Transmission in an

Emerging Market

Kodjovi M. Eklou

WP/23/146

IMF Working Papers describe research in

progress by the author(s) and are published to

elicit comments and to encourage debate.

The views expressed in IMF Working Papers are

those of the author(s) and do not necessarily

represent the views of the IMF, its Executive Board,

or IMF management.

2023

JUL

* The author(s) would like to thank Andrés Fernández, Hou Wang, Katharina Bergant, Lamin Leigh, Modeste Some, Nada Choueri,

Tidiane Kinda, and Yan Carriere-Swallow and other participants to IMF seminars for helpful comments.

© 2023 International Monetary Fund WP/23/146

IMF Working Paper

Asia and Pacific Department

The Anatomy of Monetary Policy Transmission in an Emerging Market

Prepared by Kodjovi M. Eklou*

Authorized for distribution by Lamin Leigh

July 2023

IMF Working Papers describe research in progress by the author(s) and are published to elicit

comments and to encourage debate. The views expressed in IMF Working Papers are those of the

author(s) and do not necessarily represent the views of the IMF, its Executive Board, or IMF management.

ABSTRACT: Monetary policy transmission in EMs has been found to be weak historically due to under-

developed financial markets and heavy central bank intervention in FX markets that undermine the exchange

rate channel. Against this background, this paper investigates the transmission of monetary policy, including

the role of external factors, in Malaysia and highlight findings that could be relevant for other EMs. We find an

important role for the credit and the exchange rate channels. Further, we also find a complementary role for

policy tools including Foreign Exchange Intervention (FXI) and liquidity tools such as Statutory Reserve

Requirement in shaping the transmission of monetary policy. We then explore the spillover effects of external

global factors including global monetary policy and global commodity prices on monetary policy transmission in

a small open economy such as Malaysia. The results show that while global commodity prices do not impair

monetary policy transmission, global monetary policy tightening could complement domestic efforts to achieve

price stability by inducing a global disinflation. Finally, monetary policy transmission is delayed and weakened

in high inflationary environment, with the implication that more aggressive and preemptive policy actions may

be needed in such cases.

JEL Classification Numbers:

E3, E43, E52, E58, F4; O11; O22.

Keywords:

Monetary Policy; Emerging markets; Exchange rate; Credit; Inflation;

Economic activity; Global monetary policy.

Author’s E-Mail Address:

WORKING PAPERS

The Anatomy of Monetary Policy

Transmission in an Emerging

Market

Prepared by Kodjovi M. Eklou

1

1

“The author(s) would like to thank” footnote, as applicable.

IMF WORKING PAPERS

Title of WP

INTERNATIONAL MONETARY FUND

2

Contents

Introduction ......................................................................................................................................................... 3

I. Identification of Monetary Policy Shocks .................................................................................................. 5

II. Empirical analysis of monetary policy transmission in Malaysia ..................................................... 8

A. Testing the channels of monetary policy transmission in Malaysia ...................................................... 8

B. Testing nonlinearities in monetary policy transmission in Malaysia: the role of domestic and external

factors ........................................................................................................................................................... 12

C. Testing the role of other policy levers: Foreign Exchange Interventions (FXI) and the Statutory

Reserve Requirement (SRR) ....................................................................................................................... 15

III. Conclusion ........................................................................................................................................... 18

Appendix. ........................................................................................................................................................... 19

References ......................................................................................................................................................... 25

IMF WORKING PAPERS

Title of WP

INTERNATIONAL MONETARY FUND

3

Introduction

Inflation has risen sharply to levels unseen for almost four decades in many economies, driven by a confluent

of factors including COVID-19 pandemic-related supply chain disruptions and rising commodity price shocks

amid Russian invasion of Ukraine.

1

After decades of loose monetary policy, central banks around the world

face important policy trade-offs such as striking a balance between managing inflationary pressures and

supporting nascent economic recovery. However, monetary policy transmission in emerging and developing

economies (EMDEs) has been found weak historically due to under-developed financial markets, heavy central

bank intervention undermining the exchange rate channel in FX markets (see Mishra et al, 2012), but also data

and methodological issues (see Berg et al., 2013). However, Brandão-Marques et al. (2021) shows that once

the exchange rate channel is explicitly accounted for, interest rate hikes reduce both inflation and output in

EMDEs. Further, monetary policy transmission in EMDEs depends on the policy framework, which is often

complex and opaque with multiple instruments and objectives (Berg et al, 2019), calling for the need to have

granular analyses on emerging economies to explore the potential peculiarities that may not be fully captured in

a cross-country sample.

This paper investigates monetary policy transmission in Malaysia, an emerging market economy that has

shifted to a market-based interest rate framework since May 2004. Following Romer and Romer (2004), we use

Monetary Policy Committee (MPC) meeting level data of the Bank Negara Malaysia (BNM), the central bank of

Malaysia, to estimate monetary policy shocks over the period May 2004 to July 2022.

2

We then use these

estimated shocks to investigate the transmission of monetary policy to inflation and economic activity in a local

projection framework (Jordá, 2005), similarly to Holms et al (2021). We ask the following research questions:

What are the main channels of monetary policy transmission in Malaysia? Is there any nonlinearity in the

transmission of monetary policy, including the level of the policy rate, the level of inflation, global supply side

pressures on inflation and global monetary policy tightening

3

? Is there a complementary role for other policy

tools such as Foreign Exchange Intervention (FXI) and liquidity tools such as the Statutory Reserve

Requirement (SRR) rate?

1

Headline CPI Inflation rate in Malaysia reached 4.65 percent in October in 2022 driven by food prices from a low-level pre-

pandemic (about 1 percent in December 2019).

2

The IMF (Country Report No. 2020/057) describes the policy reaction function of the BNM as “a multi-instrument reaction function

responding to multiple-indicator variables, including the exchange rate.” The principal tool for monetary policy in Malaysia is the

Overnight Policy Rate (OPR) with the Statutory Reserve Requirement (SRR) and open market operations also used to manage

liquidity. Further, the Bank Negara Malaysia’s (BNM) principal objectives are to preserve monetary and financial stability, with

the ultimate objective to promote sustainable growth. See IMF (2020) for additional detail on the monetary framework. The BNM

tightened monetary policy by increasing the overnight policy rate (OPR) five times since May 2022 by a total of 125 bps to 3.00

percent. Malaysia is not an Inflation targeter.

3

There is a large literature on the spillover effects of monetary policy in advanced economies, mainly the US, on emerging markets

(see for instance Rey, 2016; and, Miranda-Agrippino and Rey, 2020), which is outside the scope of this paper. The focus of this

paper is to investigate how global monetary policy affect domestic transmission in an emerging market economy.

IMF WORKING PAPERS

Title of WP

INTERNATIONAL MONETARY FUND

4

Using monthly data and explicitly modelling different channels of monetary policy transmission over the period

2004-2019, we find that the exchange rate and credit channels stand out. In particular, the exchange rate

channel features a strong, quick (about 7 months) and persistent transmission of monetary policy shocks to

inflation. The finding on the exchange rate channel is consistent with Brandão-Marques et al. (2021), as the

exchange rate plays an important role in emerging market economies given its large influence on demand in

small open economies and as a key variable for private sector expectations about inflation (see BIS, 2008).

We find similar results for economic activity (measured by industrial production index and unemployment rate),

with a low implied sacrifice ratio, that is the cost of output loss relative to price stability. The small sacrifice ratio

is also consistent with the relatively rapid pace of monetary policy transmission (in particular through the

exchange rate channel) but also given that the BNM is an independent central bank, and that Malaysia is an

open economy as identified by the literature on the determinants of the sacrifice ratio (see for instance,

Mazumder, 2014 and, Magkonis and Zekente, 2020).

Regarding nonlinearities, the paper shows that, while monetary policy transmission does not depend on the

level of the policy rate (OPR) or not affected by global supply side pressures on inflation

4

, the level of inflation

as well as the global monetary policy stance matter. More specifically, the paper uncovers that, monetary policy

transmission is delayed and weakened in high inflation context with the policy implication that there is a need

for a more aggressive and preemptive policy response in such contexts. Further, it shows that global monetary

policy tightening could complement domestic efforts toward price stability, but only if the former leads to a

global disinflation. Finally, it shows that policies such as liquidity tools and FXI can complement monetary policy

(in achieving price stability) in an emerging market economy such as Malaysia, as these strengthen

transmission. Consistent with the role of bank liquidity in shaping monetary policy transmission in Malaysia

(Rashid et al, 2020), the results show that tightening liquidity requirement through the SRR strengthens the

transmission. Finally, given the role of exchange rate channel, FXI plays an important complementary

especially when they lean against depreciations. FX purchases are found to amplify the credit channel of

monetary policy, consistent with Hofmann et al (2019) who find that FXI can affect domestic credit as

purchases could dampen credit to firms (in particular those vulnerable to currency movements). However,

these purchases tend to weaken the exchange rate channel. FX sales (that often takes the form of drawdown

in reserves), on the other hand, preserve the exchange rate channel with broadly neural impact on the credit

channel.

This paper brings novel insights on monetary policy transmission in EMs with important policy implications at

the current juncture characterized by high inflation and global tightening. The paper is closely related to Holms

et al (2021) and Brandão-Marques et al. (2021). It extends the framework in both papers to explicitly account

for different channels of monetary policy transmission and focuses on an emerging market to explore granular

4

Ha et al (2019) shows the importance of external shocks to domestic inflation dynamics in developing countries. Our finding

suggests that monetary policy can nevertheless deal with inflationary pressures originating from external supply side shocks.

IMF WORKING PAPERS

Title of WP

INTERNATIONAL MONETARY FUND

5

aspects of monetary policy including the role of complementary policy tools and global monetary policy stance.

To the best of our knowledge, this paper is the first, to investigate the implication of global monetary policy

tightening for domestic monetary policy transmission in an emerging market economy. Further, focusing on an

emerging market economy allows us to highlight the role of complementary tools as many EMs use multiple

tools to address shocks. Recent work by Cavallino (2019) emphasizes the role of FXI as a complementary

policy tool, but in the context of managing capital flows.

The paper contributes also more broadly to the literature on monetary policy transmission in emerging and

developing economies, including on Malaysia (see for instance Mishara et al, 2014; Khaw and Sivabalan, 2016;

Abuka et al, 2018; Poon, 2018; Barajas et al, 2018; Rashid et al, 2020).

5

For instance our results are consistent

with Abuka et al (2018) and Mishra et al (2014) who show the importance of the bank lending channel in

developing and emerging economies. Further, Barajas et al (2018) shows that remittances can weaken the

bank lending channel of monetary policy transmission by increasing liquidity in banks with their marginal cost of

loanable funds de-linked from movements in the policy rate in developing countries. Our finding on the SRR

suggests that central banks in developing countries could use liquidity tools to circumvent this challenge posed

by remittances. We also contribute to this literature by providing granular estimates of competing channels of

monetary policy channels, with an emphasis on the role of exchange rate channel, while previous work focused

on the bank lending channel in a cross-country sample. Recent empirical investigations on monetary policy in

Malaysia show the importance of the credit channel (Rashid et al, 2020)

6

, the asset price channel in particular

equity prices as captured by the stock market index (Khaw and Sivabalan, 2016) while Poon (2018) finds that

Capital Flow Measures (CFMs) reduced the transmission of monetary policy. These studies however do not

investigate explicitly the monetary policy transmission under the OPR regime as it is the case in this paper.

The remainder of the paper is organized as follows. Section I focuses on the identification of monetary policy

shocks, while section II is dedicated to the empirical analysis of monetary policy transmission in Malaysia

including the test of various channels, the nonlinearities, and the role of other policy levers. Finally, section III

concludes.

I. Identification of Monetary Policy Shocks

The first step in investigating the transmission of monetary policy is to identify monetary policy shocks.

Monetary policy decisions are usually endogenous because these decisions are made in response to current or

future economic conditions. To identify a causal effect of monetary policy, we need to isolate the component of

5

See for instance Mishra and Montiel (2013) for a comprehensive survey of the literature.

6

The authors use data on credit supply by banks to show that the credit channel is important in Malaysia, but Islamic banks respond

less to monetary policy compared to commercial banks. Further, they also find that small-sized banks respond more to the

increased interest rate as compared to large-sized banks. This finding holds for both Islamic and conventional banks. Finally,

less-liquid banks respond more to the tightening of monetary policy as compared to more-liquid counterparts.

IMF WORKING PAPERS

Title of WP

INTERNATIONAL MONETARY FUND

6

the change in the OPR that is not driven by the Central Bank’s expectation about key variables such as inflation

and growth. In this paper we follow the approach used in Romer and Romer (2004) and Holm et al (2021) to

identify these monetary policy shocks that are plausibly purged from expectations about economic conditions.

We exploit therefore the BNM monetary policy statement level data since the introduction of the market-based

interest rate framework in May 2004. Figure 1 shows historical OPR and changes in OPR by the BNM. Our

specification is similar to Holm et al. (2021) using data on policy meeting frequency as follows:

Where

is the change in the policy rate (OPR) at meeting m,

is the level of the OPR in the previous

meeting. Meeting m takes place in year t, and control variables include inflation forecasts for the current year (

and the next year (

, growth forecasts for the current and next year respectively

and

but

also the MYR/USD bilateral exchange rate from previous meeting month

.

7

Data on inflation and growth

forecasts were taken from the consensus forecast for the corresponding month of each meeting and the

bilateral exchange rate from CEIC. Finally,

is a measure of monetary policy shock associated with meeting

m obtained as a residual from equation (1).

Our estimates cover the meetings from May 2004 to July 2022. Table 1 shows the results of our estimates with

coefficients having expected coefficients and close to those found for the US and Norway by Romer and Romer

(2004) and, by Holm et al (2021) respectively. Further, similarly, the model explains about 30 percent of the

variation in the change in OPR (see Romer and Romer, 2004 and Holm et al., 2021). We find that, when the

BNM expects a strong growth in the current year, monetary policy rate is likely to be increased while it is likely

to hike the OPR when next year inflation is expected to be high. Figure 2 shows the estimated monetary policy

shocks (

from specification (1) in Table 1.

8

Following Romer and Romer (2004) and Holm et al (2021), we

obtain the monthly estimates of monetary policy shocks over January 2004 to July 2022, setting them to zero in

months without a monetary policy meeting.

7

We also use the lagged growth in the NEER (data from Haver) in an alternative specification and found very similar results.

8

The monetary policy shocks from specification (1) and (2) in Table 1 are very similar (correlation coefficient of 0.996).

IMF WORKING PAPERS

Title of WP

INTERNATIONAL MONETARY FUND

7

Figure 1: OPR and Changes in OPR

Table 1: Determinants of the changes in the OPR

(1)

(2)

-0.110***

-0.112***

(0.030)

(0.029)

0.024***

0.022***

(0.008)

(0.008)

0.029

0.024

(0.025)

(0.024)

-0.024

-0.020

(0.019)

(0.017)

0.113**

0.105***

(0.050)

(0.039)

0.011

(0.032)

0.002

(0.002)

-0.207

-0.122

(0.283)

(0.148)

N

115

115

R-squared

0.271

0.274

Robust standard errors in parentheses.

* p<0.10, ** p<0.05, *** p<0.01

IMF WORKING PAPERS

Title of WP

INTERNATIONAL MONETARY FUND

8

Figure 2: Monthly Monetary Policy Shock

II. Empirical analysis of monetary policy

transmission in Malaysia

A. Testing the channels of monetary policy transmission in Malaysia

Monetary policy transmission works through various channels including the interest rate channel, the exchange

rate channel, the bank lending (credit) channel and asset price channel.

9

First, an increase of nominal rates by

translating into higher real rates and user cost of capital lead to deferred consumption and reduction in desired

investment, thus exerting a downward pressure on prices through the interest rate channel. Second, the

exchange rate channel is also important in the context of open emerging markets and operates as follows. An

increase in domestic rates by leading to an appreciation puts downward pressure on prices of tradable goods in

the consumption basket. The exchange rate appreciation will also reduce both aggregate demand and net

exports. Third, through the credit channel, a tightening of monetary policy reduces deposits and liquidity from

the banking system and induces a reduction in lending. Finally, higher interest rates increase the discount

factor for future dividend income and could also reduce expected future cash flows and stock returns and thus

would reduce equity prices. Given the positive correlation between asset prices including equity prices and

consumption through a wealth effect, an interest rate hike would therefore reduce consumption and inflation.

9

The BNM highlighted these four channels as the most dominant for its monetary policy in a BIS survey (BIS, 2008).

IMF WORKING PAPERS

Title of WP

INTERNATIONAL MONETARY FUND

9

To test, the transmission channels of monetary policy in Malaysia, we use the previously identified monetary

policy shocks, and follow a specification similar to Holm et al. (2021) in a local projection framework (Jordá,

2005), robust to misspecification. We estimate the following equation:

Where

is the outcome variable (either the logarithm of the CPI index or the logarithm of the industrial

production index, as a proxy for output, or the unemployment rate), at time t (monthly data),

, is the

change in the logarithm of the nominal effective exchange rate (NEER),

is the year-on-year growth rate of

the stock market index,

is the change in commercial banks’ base lending rate and is a set of control

variables including the contemporaneous conditioning factors (

and

), two months of

lagged values of the dependent variable (logarithm of the CPI index and logarithm of the industrial production

index), 2 months of lagged values of the monetary policy shock

, two months of lagged values of

commodity price index, two months of lagged values of a proxy for foreign exchange intervention (FXI) and of

an index of US monetary policy uncertainty.

10

Finally, h=0,1..,24 is the horizon of cumulative response of the

dependent variable and

is the error term.

This specification augments the approach in Holm et al. (2021) and Brandão-Marques et al (2021) to explicitly

test the main competing channels of monetary policy transmission in Malaysia. Brandão-Marques et al (2021)

show that explicitly modelling the exchange rate channel of monetary policy allows to capture the effect of

monetary policy in emerging markets in a similar fashion to advanced economies. However, as previously

discussed, the BNM highlighted four main channels of monetary policy transmission including interest rate, the

exchange rate, the bank lending (credit) and asset price. We extend the specification in Brandão-Marques et al

(2021) by explicitly modelling two additional channels (asset prices and credit). In equation (2),

, captures the

cumulative impact of monetary policy shock on inflation, output, or unemployment rate at horizon h, when the

three channels of monetary policy transmission are shut down. Further, one can obtain the total impact of

monetary policy accounting for i) the exchange rate channel at one standard deviation in the change in the

NEER (σ) – about 1.2 percent appreciation – as

at horizon h, ii) the asset price channel at the 25

th

percentile of stock market index price growth (p25 ) – about -2.9 percent – as

and, iii) the credit

channel at a one standard deviation(φ) – about 7 basis points increase – in the base lending rate as

.

10

The lag selection was based on the Akaike and Bayesian information criteria. Further, the specification on industrial output uses 3

months of lagged values of the monetary policy shock and accounts for a structural break in the series around 2009:M2.

Following Holm et al. (2021), we smoothed the industrial production index. Data on industrial production index, CPI index, were

taken from International Financial Statistics, stock market index (FTSE Bursa MYSA composite) and base lending rate of

commercial banks from CEIC, FXI proxy data is taken from Adler et al. (2021) and US monetary policy uncertainty index from

Husted et al (2020). See Lakdawala et al (2021) who find a stronger spillover of US monetary policy uncertainty to bond yields in

EMs compared to US policy rates. Note that BNM counts FX market operations as part of monetary policy instruments with the

aim to mainly smooth ringgit movements (see BIS survey).

IMF WORKING PAPERS

Title of WP

INTERNATIONAL MONETARY FUND

10

Throughout the paper, we measure the outcome variable in deviation relative to its initial level in the month

preceding the shock and thus impacts shown should be interpreted as percent of initial month’s value. More

specially, outcome variables are the log change times 100. The policy shocks are measured as 1 percentage

point or 100 basis points (bps) change in month 0. The only exception is in the case of unemployment rate,

where the results are presented as a deviation in percentage points compared to the initial’s month value.

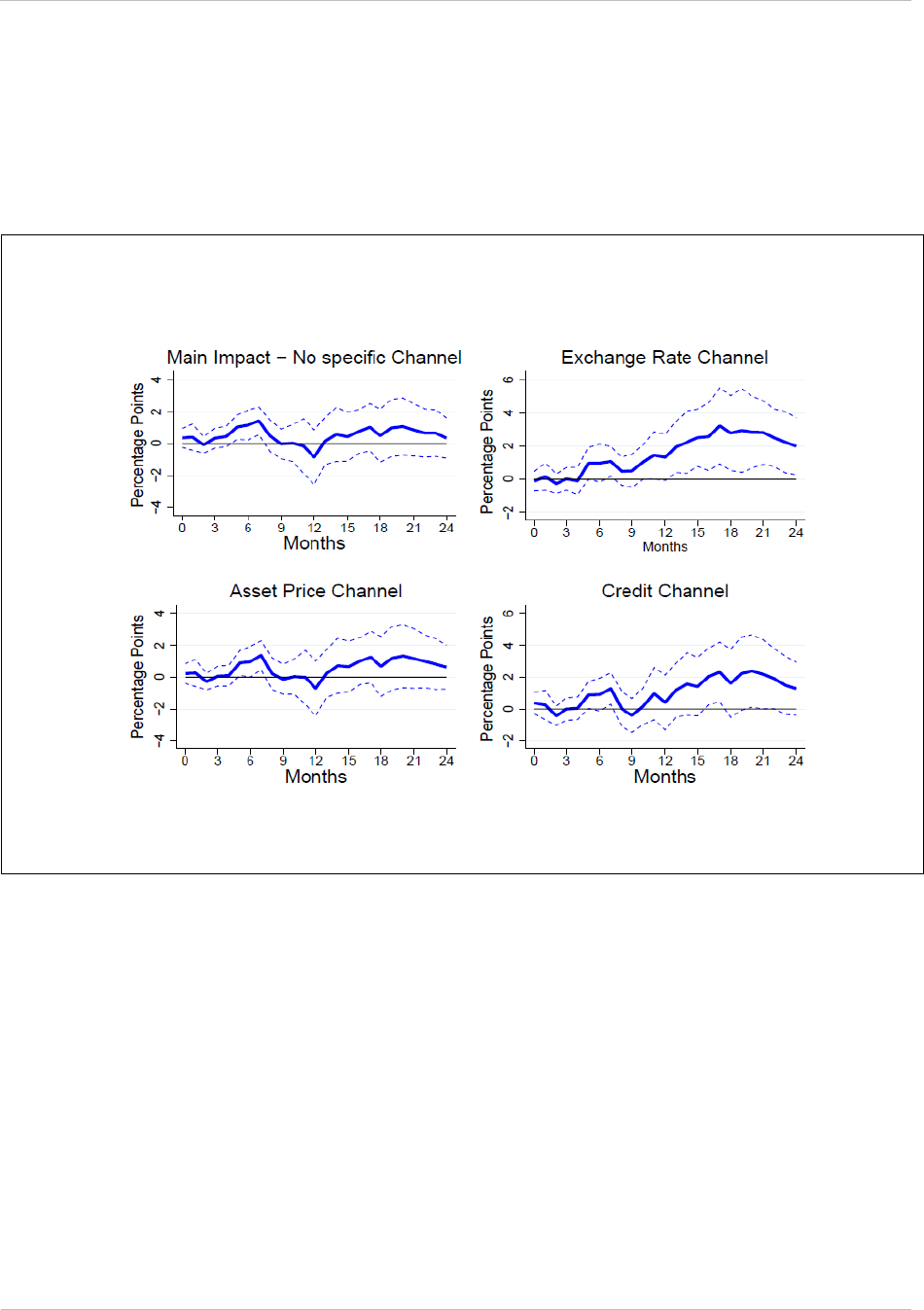

The impulse response functions (IRF) in Figure 3 show that, the effect of a 100bps increase in monetary policy

shock shutting off all channels, is negative and statistically significant only about 14-15 months and this effect

persists up to 21 months and can reach about 2.5 percent reduction in inflation. Focusing on the asset price

channel and testing for a potential amplifying effect of asset price movement yields a very similar IRF as in the

main effect. This suggests that the asset price channel is relatively muted. However, the IRF focusing on the

exchange rate channel shows larger impact on inflation in the short and long term. We find that in about 7

months, the same monetary policy shock could reduce inflation by 5 percent cumulatively. These effects could

persist and be larger in the long term (13 months – with a cumulative peak impact at about 8 percent). These

results imply that for an initial inflation rate of 3 percent, a 100bps tightening could lead to an inflation rate of

about 2.75 percent in 13 months. The credit channel on the other hand shows a cumulative reduction in

inflation by 3 percent in 18 months for the same magnitude of monetary policy shock. Overall, our finding is

similar to Brandão-Marques et al (2021) showing that the exchange rate channel is important for monetary

policy transmission in EMs.

11

The finding on the credit or bank lending channel is consistent with previous

literature (see for instance Mishra et al, 2014 and, Abuka et al., 2018).

11

The exchange rate plays an important role in emerging market economies given its the large influence on demand in small open

economies and as a key variable for private sector expectations about inflation (see BIS, 2008). We use credit growth as an

alternative measure to the base lending rate and found similar results for credit channel.

IMF WORKING PAPERS

Title of WP

INTERNATIONAL MONETARY FUND

11

Figure 3: Cumulative Impulse Response Function of a 100bps Monetary Policy Shock on

Inflation

Note: 90 percent confidence interval in dashed lines. Newey-West standard errors (robust to

autocorrelation) are used

Figure 4 shows our results for output response to monetary policy shocks. Our results show that a 100 bps in

monetary policy shock could reduce industrial production cumulatively by between 2 percent (main impact) to

about 3 percent in 24 months (when accounting explicitly for the credit channel or exchange rate channel).

These estimates, imply based on a back-of-the envelope calculation a reduction in real GDP by between 3.6

percent and 5.4 percent over 24 months respectively.

12

These estimates imply a sacrifice ratio close to one for

24 months.

13

Our results are close to Khaw and Sivabal (2016) who also found a low sacrifice ratio in

Malaysia. We also investigated the impact of monetary policy on unemployment rate (Figure A1 in Annex). We

find an increase in unemployment by about 2 percentage points in 24 months. Our finding on the small sacrifice

ratio is also consistent with the relatively rapid pace of monetary policy transmission (in particular through the

exchange rate channel) but also given that the BNM is an independent central bank, and that Malaysia is an

open economy.

14

12

Using quarterly data, we regress the logarithm of real GDP on the logarithm of industrial index production and found that industrial

production account for about 80 percent of the variation in real GDP over the period. Further, we found that a 1 percent increase

in industrial production implies a 1.8 percent increase in real GDP.

13

We calculate the sacrifice ratio as the ratio of the reduction in output over the reduction inflation.

In a shorter period (13 months),

the sacrifice ratio is below one. The sacrifice ratio is even lower considering the impact of monetary policy on unemployment

rate.

14

See for instance Mazumder (2014) and, Magkonis and Zekente (2020) showing that high speed of disinflation, greater central

bank independence and greater openness reduce the sacrifice ratio.

IMF WORKING PAPERS

Title of WP

INTERNATIONAL MONETARY FUND

12

Figure 4: Cumulative Impulse Response Function of a 100bps Monetary Policy Shock on

Industrial Production

Note: 90 percent confidence interval in dashed lines. Newey-West standard errors (robust to

autocorrelation) are used.

B. Testing nonlinearities in monetary policy transmission in Malaysia: the role

of domestic and external factors

In this section, we investigate the role of external factors (commodity prices and global monetary policy) as well

as domestic factors (high inflation and the level of the OPR) in shaping the transmission of monetary policy.

Focusing on the main channels of monetary policy transmission in Malaysia as identified in the previous

section, we consider the following equation:

Where

is a set of domestic factors (high inflation rate and the level the OPR) as well as external factors

(global commodity prices and global monetary policy), with now including two months lag values of these

domestic and external factors in addition to other controls consistently, while other variables retain the same

definition. We use the global commodity price index (as well as global food, energy and input price indexes as

a proxy for global supply side inflationary pressure) from the IMF. Drawing from the BIS policy rate statistics,

we measure global monetary policy as the average of change in policy rates weighted by each country’s

IMF WORKING PAPERS

Title of WP

INTERNATIONAL MONETARY FUND

13

currency share in global foreign exchange reserves.

15

We also investigate whether the monetary policy

transmission is affected by the level of policy rate and high inflation rates.

Our results in Figure A2 and A3 in the Appendix show that external supply side pressures on inflation as

captured through international commodity price dynamics (see Ha et al, 2019 on the role of external shocks in

driving inflation in developing countries), do not impair the ability of monetary policy to achieve price stability in

Malaysia. We test the impact of a 100 bps monetary policy shock conditional on a one standard deviation in

global commodity price inflation and found that there is no significant change to the baseline transmission

whether focusing on the credit or the exchange rate channel. We found similar results for global industrial input

price, global energy price and global food price inflation.

16

Our finding suggests that external supply side

pressures on inflation as captured through international commodity price dynamics, would not impair the ability

of monetary policy to achieve price stability in Malaysia.

Next, Figure 4 shows that global monetary policy tightening amplifies monetary policy transmission in Malaysia.

Our estimates of the impact of monetary policy shock in Malaysia conditioning on a 1 standard deviation –

about 13bps – hike globally shows that inflation could be cumulatively reduced by between 8 percent in 7

months (exchange rate channel) and about 10 percent (credit channel) in 18 months. Our findings suggest that

a synchronized tightening could have a persistent reduction effect on inflation up to 24 months, with all major

channels of monetary policy transmission amplified. We further investigate the channels through which global

monetary policy tightening could complement domestic effort to mitigate inflationary pressures in Malaysia. To

do so, we include global growth and global inflation among controls at different horizons.

17

We find that, once

we control for global inflation dynamics, the complementary role of global monetary policy is weakened (See

Figure A4 in Annex). This suggests that global monetary policy tightening would complement domestic efforts

only to the extent that it reduces global inflation. This finding is consistent with Ha et al. (2019) who show that

global inflation dynamics play an important role in shaping domestic inflation in developing countries. Further,

while there is a large body of the literature showing the negative spillovers of monetary policy in advanced

economies to EMs (see for instance Rey, 2016; and, Miranda-Agrippino and Rey, 2020), the paper shows a

novel result on how global monetary policy could affect domestic monetary policy effectiveness in maintaining

price stability.

15

This approach is similar to the Council on Foreign Relations’ methodology for their global monetary policy tracker. Our indicator

includes Australia, Canada, China, Euro area, Japan, Switzerland, United Kingdom, and United States. The currencies of these

countries represent about 97 percent of global foreign exchange reserves with the USD representing about 61 percent (data as

of 2022Q1).

16

We have also found (results not shown here) that while in general, monetary policy does not affect supply side inflation as

captured by the producer price index (PPI), considering the exchange rate channel, monetary policy can reduce PPI inflation in

Malaysia.

17

We applied Spline extrapolation to quarterly data from the IMF World Economic Outlook database to obtain monthly figures.

IMF WORKING PAPERS

Title of WP

INTERNATIONAL MONETARY FUND

14

We then, turn to test whether the impact of monetary policy depends on the level of the OPR and on the level

of inflation. We test the impact of a 100bps hike in the monetary policy shock conditioning on the median level

of the policy rate (of 3 percent) and found that there is no impact on the transmission compared to our baseline

finding (see Figure A5 in Appendix). This suggests that the transmission of monetary policy in Malaysia is

independent of the level of the policy rate. Further, we examine the role of high inflationary environment by

estimating the impact of a 100bps hike in the monetary policy shock conditioning on the level of inflation rate.

The estimates using the 75th percentile of inflation rate (3.2 percent) as a proxy for high inflation is shown in

Figure 6. The IRF shows that monetary policy transmission is weakened in high inflation environment. More

specifically, we find that the monetary policy transmission through the exchange rate is now delayed as we find

a statistically significant impact only around 13 months. In terms of magnitude, our results imply that the

effectiveness of monetary policy transmission could be reduced between about 20% (credit channel) and 30

percent (exchange rate channel) based on peak impacts. One implication is that in a period of high inflation,

monetary policy tightening may need to be more aggressive and preemptive to achieve the same result under

normal conditions but there could be also a delay in the transmission.

Figure 5: Synchronized Tightening and Monetary Policy Transmission to Inflation in Malaysia

Note: 90 percent confidence interval in dashed lines. Newey-West standard errors (robust to autocorrelation) are

used.

IMF WORKING PAPERS

Title of WP

INTERNATIONAL MONETARY FUND

15

C. Testing the role of other policy levers: Foreign Exchange Interventions

(FXI) and the Statutory Reserve Requirement (SRR)

In this section, we explore the role of other policy levers in shaping monetary policy transmission in Malaysia.

We employ a specification similar to equation (3) to investigate the role of FXI (one month lag) and SRR. As

discussed earlier, the BNM acknowledges FXI as being part of primary instruments of monetary policy albeit

with the sole aim to smooth ringgit movements. Given the importance of the exchange rate channel we test

how FXI interacts with monetary policy transmission in Malaysia. Further, while the BNM emphasizes that the

SRR should not be seen as a signal on the monetary policy stance it however stated that SRR can be used to

support the transmission of monetary policy rates to retail rates (see link). In addition, recent evidence (Rashid

et al, 2020) shows the importance of the liquidity condition of banks in shaping the transmission of monetary

policy in Malaysia.

Figure 6 shows the results for the role of changes in the SRR rate. Our IRF with the impact of a 100bps hike in

monetary policy shock estimated for 1 standard deviation in the change of the SRR – about 19bps – shows that

while the change in the SRR does not have material impact on the transmission through the exchange rate

channel it amplifies the credit channel, in particular in the medium term. We find a cumulative reduction in

inflation by 4 percent in 18 months compared to about 3 percent in the baseline estimates. This finding

suggests that liquidity tools could complement monetary policy in taming inflation in developing countries where

liquidity at banks play an important role in the transmission of monetary policy, as shown for countries highly

dependent on remittances (see for instance Barajas et al, 2018). Further, our finding is consistent with previous

finding that tightening of SRR leads to increased lending rates (Glocker and Towbin, 2012; and Kim and

Mehrotra, 2022).

Figure 6: High inflation environment and Monetary Policy Transmission to Inflation Malaysia

Note: 90 percent confidence interval in dashed lines. Newey-West standard errors (robust to autocorrelation) are

used.

IMF WORKING PAPERS

Title of WP

INTERNATIONAL MONETARY FUND

16

Finally, Figure 7 shows our results regarding how FXI affect monetary policy transmission with differentiation

between sales and purchases.

19

We find that FXI purchases amplify the credit channel, leading to a persistent

reduction in inflation with a cumulative impact (for a 1 percentage point of GDP increase) reaching about 4

percent reduction in inflation in 14 months (see Figure 7). This result is consistent with Hofmann et al (2019)

who find that FXI can affect domestic credit as purchases could dampen credit to firms (in particular those

vulnerable to currency movements). At the same time, by leaning against exchange rate appreciations, FX

purchases tend to weaken the exchange rate channel of monetary policy (see Mishra et al, 2012). Finally, we

find that sales preserve the exchange rate channel, by leaning against depreciations, with a broadly neutral

impact on the credit channel. Overall, consistent with Cavallino (2019) our finding suggests that FXI are a

complementary policy tool to monetary policy.

20

19

Figure A7 in Appendix shows FXI series.

20

Note however that Cavallino (2019) emphasizes the role of FXI as a complementary policy tool, but in the context of managing

capital flows within a DSGE framework with an application to Swiss data.

Figure 6: Statutory Reserve Requirement and Monetary Policy Transmission to Inflation in Malaysia

Note: 90 percent confidence interval in dashed lines. Newey-West standard errors (robust to autocorrelation) are

used.

IMF WORKING PAPERS

Title of WP

INTERNATIONAL MONETARY FUND

17

Figure 7: Foreign Exchange Intervention (FXI) and Monetary Policy Transmission in Malaysia

Note: 90 percent confidence interval in dashed lines. Newey-West standard errors (robust to

autocorrelation) are used.

IMF WORKING PAPERS

Title of WP

INTERNATIONAL MONETARY FUND

18

III. Conclusion

This paper investigates the transmission of monetary policy in Malaysia, a small open emerging economy over

the period 2004-2019 using monthly data. It shows that both exchange rate and the credit channels are

important for monetary policy transmission in this economy. While we find that monetary policy tightening

reduces both output and inflation, the relative cost of output loss to price stability is found to be low.

The paper uncovers important nonlinearities. First, the results show that in a high inflation context, monetary

policy transmission is weakened and delayed suggesting that a more aggressive and a preemptive policy rate

adjustment would need to be considered to have an impact similar under normal conditions. Second, global

monetary policy tightening amplifies monetary policy transmission with a larger reduction in inflation compared

to only a domestic policy tightening, driven by global disinflation. Third, in line with the importance of banking

sector liquidity in the transmission of monetary policy in Malaysia, we find that tightening the Statutory Reserve

Requirement (SRR) could amplify the impact of monetary policy tightening particularly through the credit

channel. Finally, FX purchase could strengthen the credit channel (although weakening the exchange rate

channel) while FX sales preserve the exchange rate channel.

This paper is the first, to the best of our knowledge to provide empirical evidence on the implication of global

monetary policy tightening for monetary policy transmission in a small open EM. It also brings novel insights on

monetary policy transmission in EMs with important policy implications at the current juncture characterized by

high inflation and global tightening. Further, it shines some light on whether global supply side pressures could

impede monetary policy transmission in a small-open economy. Finally, the paper brings also novel insights

regarding the complementarity of other policy tools in enhancing monetary policy transmission in an emerging

market.

IMF WORKING PAPERS

Title of WP

INTERNATIONAL MONETARY FUND

19

Appendix.

Figure A1: Cumulative Impulse Response Function of a 100bps Monetary Policy Shock on the

Unemployment Rate

Note: 90 percent confidence interval in dashed lines. Newey-West standard errors (robust to

autocorrelation) are used.

IMF WORKING PAPERS

Title of WP

INTERNATIONAL MONETARY FUND

20

Figure A2: Global Input and Energy Price - Monetary Policy Transmission to Inflation

Note: 90 percent confidence interval in dashed lines. Newey-West standard errors (robust to

autocorrelation) are used.

IMF WORKING PAPERS

Title of WP

INTERNATIONAL MONETARY FUND

21

Figure A3: Global Commodity Prices - Monetary Policy Transmission to Inflation

Note: 90 percent confidence interval in dashed lines. Newey-West standard errors (robust to

autocorrelation) are used.

IMF WORKING PAPERS

Title of WP

INTERNATIONAL MONETARY FUND

22

Figure A4: Channels of Global Monetary Policy Transmission to Inflation in Malaysia

Note: 90 percent confidence interval in dashed lines. Newey-West standard errors (robust to

autocorrelation) are used.

Figure A5: The Level of the OPR and Monetary Policy Transmission to Inflation in Malaysia

Note: 90 percent confidence interval in dashed lines. Newey-West standard errors (robust to autocorrelation) are

used.

IMF WORKING PAPERS

Title of WP

INTERNATIONAL MONETARY FUND

23

Figure A6: The Response of the Policy rate (OPR) to Monetary Policy Shocks

Note: 90 percent confidence interval in dashed lines. Newey-West standard errors (robust to

autocorrelation) are used. This Impulse Response shows how the level of OPR responds to a 100bps

monetary policy shock over the period 2004-2019 using monthly data.

IMF WORKING PAPERS

Title of WP

INTERNATIONAL MONETARY FUND

24

Figure A7: Foreign Exchange Intervention

Note: Data is taken from Adler et al. (2021) and Author’s calculation. Monthly series as percent of GDP.

IMF WORKING PAPERS

Title of WP

INTERNATIONAL MONETARY FUND

25

References

Abuka, C., Alinda, R. K., Minoiu, C., Peydró, J. L., and Presbitero, A. F. (2019). Monetary policy and bank

lending in developing countries: Loan applications, rates, and real effects. Journal of Development

Economics, 139, 185-202.

Adler, G., Chang, K. S., Mano, R., and Shao, Y. (2021). Foreign exchange intervention: A dataset of public

data and proxies. International Monetary Fund.

Bank for International Settlements, BIS. 2008. “Transmission Mechanisms for Monetary Policy in Emerging

Market Economies,” BIS Papers No. 35.

Barajas, A., Chami, R., Ebeke, C., and Oeking, A. (2018). What's different about monetary policy transmission

in remittance-dependent countries? Journal of Development Economics, 134, 272-288.

Berg, M. A., Charry, M. L., Portillo, M. R. A., and Vlcek, M. J. (2013). The monetary transmission mechanism in

the tropics: A narrative approach. International Monetary Fund.

Berg, A., Charry, L., Portillo, R., and Vlcek, J. (2019). The monetary transmission mechanism in the tropics: a

case study approach. Journal of African Economies, 28(3), 225-251.

Brandão-Marques, L., Gelos, G., Harjes, T., Sahay, R., and Xue, Y. (2021). Monetary Policy Transmission in

Emerging Markets and Developing Economies. CEPR Discussion Paper.

Cavallino, P. (2019). Capital flows and foreign exchange intervention. American Economic Journal:

Macroeconomics, 11(2), 127-70.

Ha, J., Ivanova, A., Montiel, P. J., and Pedroni, P. (2019). Inflation in low-income countries. World Bank Policy

Research Working Paper, (8934).

Hofmann, B., Shin, H. S., and VillamizarVillegas, M. (2019). FX intervention and domestic credit: Evidence

from high-frequency micro data., BIS Working Papers.

Holm, M. B., Paul, P., and Tischbirek, A. (2021). The transmission of monetary policy under the

microscope. Journal of Political Economy, 129(10), 2861-2904.

Husted, L., Rogers, J., and Sun, B. (2020). Monetary policy uncertainty. Journal of Monetary Economics, 115,

20-36.

International Monetary Fund, 2020), Malaysia: 2020 Article IV Consultation-Press Release; Staff Report; and

Statement by the Executive Director for Malaysia, Country Report No. 2020/057.

Jordà, Ò. (2005). Estimation and inference of impulse responses by local projections. American economic

review, 95(1), 161-182.

Glocker, C., and Towbin, P. (2012). Reserve Requirements for Price and Financial Stability: When Are They

Effective? International Journal of Central Banking.

Khaw, D., and Sivabalan, R. (2016) “The Monetary Policy Transmission Mechanism in Malaysia: Evolution over

the Past Two Decades”.

Lakdawala, A., Moreland, T., and Schaffer, M. (2021). The international spillover effects of us monetary policy

uncertainty. Journal of International Economics, 133, 103525.

IMF WORKING PAPERS

Title of WP

INTERNATIONAL MONETARY FUND

26

Kim, S., and Mehrotra, A. (2022). Examining macroprudential policy and its macroeconomic effects–some new

evidence. Journal of International Money and Finance, 128, 102697.

Magkonis, G., and Zekente, K. M. (2020). Inflation-output trade-off: Old measures, new determinants? Journal

of Macroeconomics, 65, 103217.

Mazumder, S. (2014). Determinants of the sacrifice ratio: Evidence from OECD and non-OECD

countries. Economic Modelling, 40, 117-135.

Miranda-Agrippino, S., and Rey, H. (2020). US monetary policy and the global financial cycle. The Review of

Economic Studies, 87(6), 2754-2776.

Mishra, P., Montiel, P. J., and Spilimbergo, A. (2012). Monetary transmission in low-income countries:

effectiveness and policy implications. IMF Economic Review, 60(2), 270-302.

Mishra, P., and Montiel, P. (2013). How effective is monetary transmission in low-income countries? A survey

of the empirical evidence. Economic Systems, 37(2), 187-216.

Mishra, P., Montiel, P., Pedroni, P., and Spilimbergo, A. (2014). Monetary policy and bank lending rates in low-

income countries: Heterogeneous panel estimates. Journal of Development Economics, 111, 117-131.

Poon, A. (2018). The transmission mechanism of Malaysian monetary policy: a time-varying vector

autoregression approach. Empirical Economics, 55(2), 417-444.

Rashid, A., Hassan, M. K., and Shah, M. A. R. (2020). On the role of Islamic and conventional banks in the

monetary policy transmission in Malaysia: Do size and liquidity matter? Research in International Business

and Finance, 52, 101123.

Rey, H. (2016). International channels of transmission of monetary policy and the Mundellian trilemma. IMF

Economic Review, 64(1), 6-35.

Romer, C. D., and Romer, D. H. (2004). A new measure of monetary shocks: Derivation and

implications. American Economic Review, 94(4), 1055-1084.