Access

Holdings

Full Year 2022

Financial and Operating Results

Presentation

April 2023

Outline

❖ Macroeconomic and regulatory

update

❖ Strategic update

❖ Financial and operating results

❖ Access Banking Group- Capital &

Liquidity Management

❖ Forward Looking Guidance

2

Caution regarding forward-looking statements

The information presented herein is based on sources which

Access Holdings Plc. “ the Holding Company” regards as

dependable. This presentation may contain forward looking

statements. These statements concern or may affect future

matters, such as the Holding Company’s economic results,

business plans and strategies, and are based upon the

current expectations of the directors. They are subject to a

number of risks and uncertainties that might cause actual

results and events to differ materially from the expectations

expressed in or implied by such forward looking statements.

Factors that could cause or contribute to differences in

current expectations include, but are not limited to, regulatory

developments, competitive conditions, technological

developments and general economic conditions. The Holding

Company assumes no responsibility to update any of the

forward-looking statements contained in this presentation.

The information should not be interpreted as advice to customers on the purchase or sale of specific

financial instruments. Access Holdings Plc. bears no responsibility in any instance for loss which may

result from reliance on the information.

Access Holdings Plc. holds copyright to the information, unless expressly indicated otherwise or this is

self-evident from its nature. Written permission from Access Holdings Plc. is required to republish the

information on Access Holdings Plc. or to distribute or copy such information. This shall apply

regardless of the purpose for which it is to be republished, copied or distributed. Access Holdings

Plc.'s customers may, however, retain the information for their private use.

Transactions with financial instruments by their very nature involve high risk. Historical price changes

are not necessarily an indication of future price trends. Investors are encouraged to acquire general

information from Access Holdings Plc. or other expert advisors concerning securities trading,

investment issues, taxation etc. in connection with securities transactions.

The information contained in this presentation is subject to, and must be read in conjunction with, all

other publicly available information, including, where relevant any fuller disclosure document published

by the Holding Company. Any person at any time acquiring the securities must do so only on the basis

of such person’s own judgment as to the merits of the suitability of the securities for its purposes and

only on such information as is contained in public information having taken all such professional or

other advice as it considers necessary or appropriate in the circumstances and not in reliance on the

information contained herein. The information is not tailored for any particular investor and does not

constitute individual investment advice.

3

A leading global financial institution

Our Mission

To build and sustain one global platform, open for anyone to join

where people can be connected to exceptional opportunities.

Our Vision

To create a globally connected community and ecosystem;

Inspired by Africa, for the World.

Our Values

❖ Excellence

“Putting in exceptional effort for exceptional

results”

❖ Curiosity

“Never stop questioning”

❖ Empathy

“Standing in someone else’s shoes and

seeing through their eyes”

4

Macroeconomic &

Regulatory update

5

6

2022 Global Operating Environment

• Global economy on a tight rope – ongoing

global banking crisis (Silicon Valley Bank,

Signature Bank, Credit Suisse with a possible

trickledown effect on emerging economies

including Nigeria.

• Ongoing impact of Ukraine/Russian war

• Knock on effect of supply chain constraints

from China lockdowns

• Crude oil prices rose above US$100 for the first

time since 2014

• Most central banks hiked interest rates to

combat inflationary pressures (particularly

energy & food)

• Monetary policies’ tightening

• The USD strengthened against the World’s

major currencies and the yields on emerging

market bonds spiked.

• Increased risk of recession across key

markets

Global Outlook

Many economies in Sub-Saharan Africa experienced significant

headwinds

Crude oil price stabilized above

$80 per barrel

Real GDP growth rate remained

positive although expanding at a

slower pace

Marginal drop in foreign reserves

but able to finance more than 7

months of import

High inflation due to higher food and

energy prices but prices are

moderating helped by increase in

benchmark interest rate

The official exchange rate recorded

modest depreciation of about 8.5% in

2022 due to FX illiquidity

Monetary policy tightening to dial

back inflationary pressures and

reduce negative real interest rates

Average 90-day T-Bill rate

decreased to 3.94% in Q4,

down from the Q3 rate of 7.29%

driven by an increased demand

for short-term instruments in the

fixed income market.

Oil production dropped to 0.94mbpd in September

2022 but ended the year on an upswing, hitting

1.23 mbpd* aided by measures introduced to

tackle oil theft

Highlights of the Nigerian Domestic Economy in 2022

Like other EMDEs*, Nigeria was not immune from the impact of the Russia-Ukraine crisis as inflation especially food and energy

prices rose. CBN raised interest rates multiple times to slow down accelerating inflation

* mbpd – million barrels per day * EMDEs – Emerging and Developing Economies

New government in Nigeria will be

faced with four key imperatives –

subsidy removal, debt restructuring,

FX rate adjustment and monetary

policy adjustments

Moody’s & Fitch Ratings downgraded the

sovereign on concerns around the macro indices

with contagion effect on 9 Nigerian Banks,

including Access Bank.

2022 highlights of the regulatory landscape (Nigeria)

Banking

• Redesign of the E-Naira by the CBN to control the

money supply and aid security agencies in tackling illicit

financial flows. The new Naira notes became available

to the public from Thursday, December 15, 2022. Under

the policy, the CBN expects to mop up about N2.7

trillion held outside the banking system, out of the N3. 2

trillion in circulation

• The Monetary Policy Committee of the Central Bank

of Nigeria voted to increase the benchmark interest

rate (MPR) from 14% to a 20-year high of 16.5%,

following the rise of inflation.

Pensions

• Due to the opening of the transfer window, the

competition in the industry has grown significantly as

the number of RSA transfers hit a record high in Q2

2022.

• The industry also witnessed some M&A activities in

2022 in it’s bid to meet the required minimum

Regulatory Capital of N5 billion, which was increased

from N1 billion by PENCOM, leading to a reduction in

the total number of PFAs from 22 to 20. M&A is

expected to continue in the Year 2023 as major

players look to acquire increased assets under

management.

MPR rate was 18% as at the end of Mar 2023

2022 highlights of the regulatory landscape (African Subsidiaries)

Ghana:

• Government of Ghana officially announced in December

2022 of plans to restructure its debt, on local

bondholders (of which Ghanian local banks account for

33% of total government debt, the largest group as at

December 2022) have been asked to swap GHS137.3

billion worth of domestic debt for new bonds.

• Parliament passed the e-levy bill in March 2022 at a rate

of 1.5%. The levy was expected to raise about GHS6.9

bn. The levy applies to instant payments, mobile money

payments, bank transfers and merchant payments.

Botswana:

• The Bank of Botswana is replacing the old Banking Act

with a new one. This is still at initial stages (bill stage).

Banking industry is doing its assessment.

Botswana:

• The Financial Intelligence Agency(FIA) has advised that

Botswana will undergo a mutual evaluation by the Financial

Action Task Force in 2024. A committee has been set up

that includes financial institution and regulators to work on

the gaps before the actual evaluation takes place

Kenya:

• Central Bank of Kenya (CBK) announced the reintroduction of

charges for transactions between mobile wallets and bank

accounts which was waived in March 2020. This will lead to

increased revenues on mobile transactions for Banks.

• Increased CBK surveillance on Digital lenders leading to

deregistration of 12 out of 25 small Digital lenders and

registration of 5 new Digital lenders. Being a competitive

environment, Banks are to ensure adherence to digital lending

regulations as prescribed in the Data protection act

Strategic update

10

85%

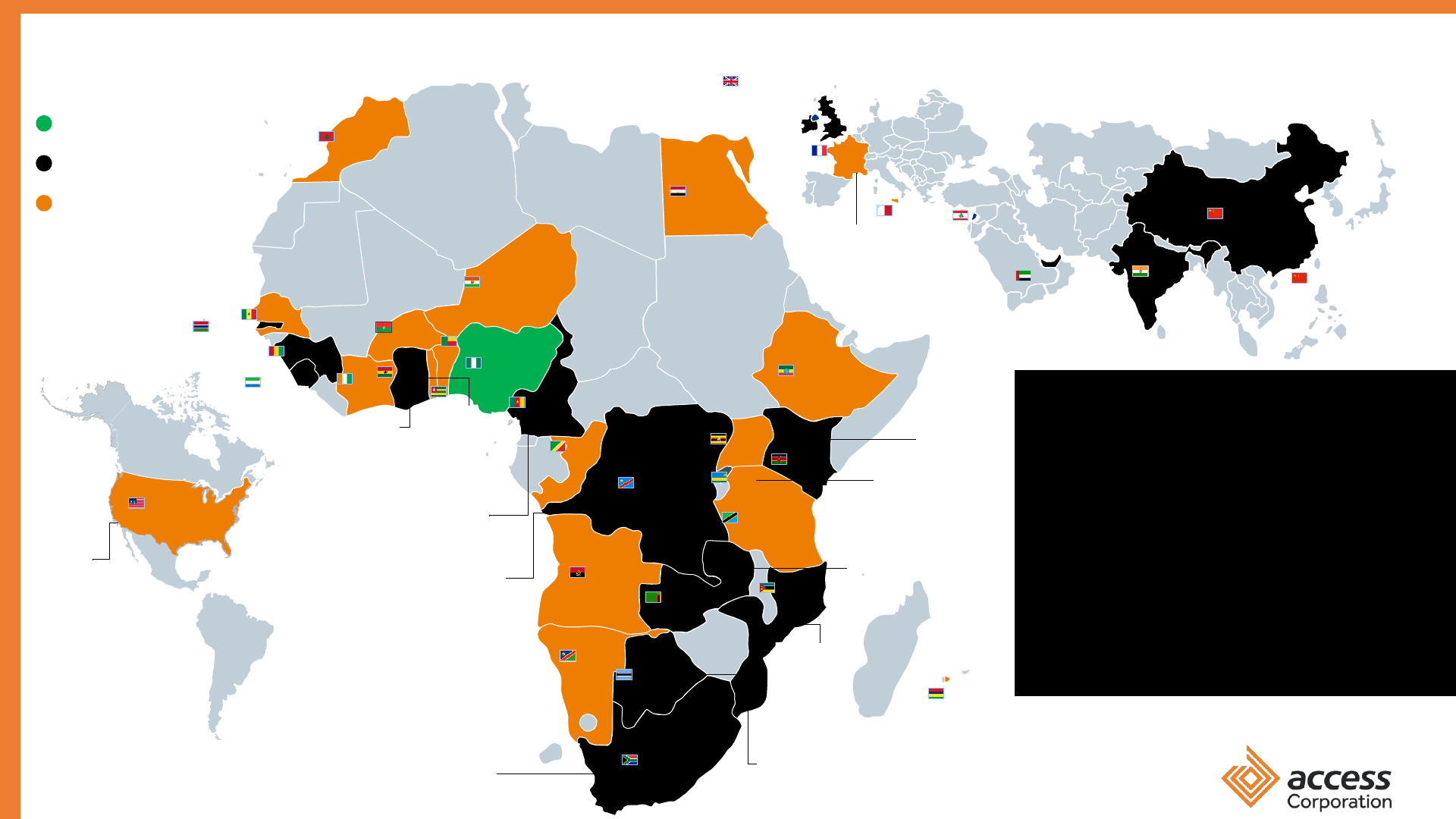

Access Corporation’s Global network and scale

Superior service through four SBUs,

across 17 countries including, the

UAE, UK, and 3 rep offices in China, India

and Lebanon

Corporate Commercial Business Retail

58 Million+

customers

More than the population of

85% (50) of African countries

Large customer base Growing users on our digital channels

18.5mn unique

mobile app and

internet banking

users

633 Branches

2,894+ ATMs

12.5mn + USSD

users

53,164+ POS

200k+

Agents

Consistent financial performance

₦1,388trn

Gross Earnings

(FY ‘22)

₦167.7bn

Profit before tax

(FY ‘22)

13.3%

ROAE

19.6%

CAR

14.7%

Tier 1 ratio

Significant gender diversity

6,824

Professional Staff

53% 47%

Awards & recognitions

2022 International Investors Award - Best Environmental and Social Performance Award

2022 Finance Derivative Award - Best Sustainable Bank Africa

2022 Euromoney Awards - Best Bank in Nigeria

2022 Global Sustainable Finance Awards - Outstanding Leadership in ESG-Related Loans, Africa

2022 Global Sustainable Finance Awards - Financial Leadership in Sustaining Communities, Africa

2022 Global Brands Magazine Awards – Best Digital Banking Brand

Listings

(Primary equity listing)

($400m Tier II bond)

($300m Senior bond)

B3

B-

B-

AA-

• Payments • Pensions

• Consumer lending• Insurance

Holdco verticals

Source: Access Bank Financial Statements

Retail Customers grew by 13mn in the year 2022.

11

A conscious & deliberate ESG strategy continues to be at the heart of our business

$50mn

Reg S Step-Up Green Notes due

2027 in the international capital

market via a private placement

Environment

Social

Governance

Launched the

implementation

Report on the Global

Principles for

Responsible Banking

First Commercial Bank in Africa certified by

Sustainability Standards and Certification

Initiative (SSCI)

World Finance Award -Best ESG Strategy (11

th

time

winner)

Pioneered

sustainability

reporting in the

Nigerian Financial

Sector

Environmental Audit

of all Branches across

Nigeria

Certifications and Memberships

1. SSA - Sub-Saharan Africa

20,500+ children beneficiaries

of a Science Technology,

Engineering, Art and

Mathematics campaign

Championed the Coalition Against COVID-19

(CACOVID)

Human Resource &

Sustainability Standalone

Board Committee

Developed an

ESG

Framework

First Corporate to issue a Certified

Green Bond in SSA

(1)

Board member, UNGC

Minimum of 1% of PBT

dedicated to

Sustainability

Reached 6,232,809

lives through

community

interventions

Impacted over

1,288

communities and

257 Non-

Governmental

Organizations

Employees

volunteered

381,733 hours

in community

projects across

Nigeria

Responsible waste

recycling in 75 office

locations, recycling a

total of 2,225.987kg of

waste recycled of cans,

paper, plastics, and

glass

167 offsite locations/

branches with ATMs

powered by solar

Developed GHG

emission

reduction strategy

for carbon abatement

and offset

By focusing on 6 key strategic priorities

Access has registered successes across its ambition

and vision over the past five years (2018 - 2022)

#1 in Nigeria

Top 10 in Africa

World’s most

respected

African Bank

Strong Franchise

outside of Africa

Access Bank has worked

towards its vision

Success Highlights

Retail banking growth and wholesale

bank consolidation

✓ 01

Focus on being digitally led

✓ 02

Being customer centric and focused

✓ 03

Analytics-driven insights and robust

risk management

✓ 04

Global collaboration

✓ 05

Building a universal payments gateway

✓ 06

Retail banking growth &

wholesale bank consolidation:

Retail grew to ~58M customers

surpassing the original

aspiration of 35M by the end of

2022

Global collaboration: Access

has attained the credit ratings at

the sovereign ceiling and

established a network of 13

subsidiaries

Building a universal payments

gateway: Access has launched

an African payments platform

with c.75% growth in revenues

between 2020 and 2022

Robust risk management:

Access Corporation has a

strong CAR ratio of 19.6%

1. Robust risk management 2. Organizing for growth 3. Flawless execution

Strategic enablers

13

We have reorganized to capture new opportunities

by transitioning to a HoldCo structure

5 Strategic objectives

The HoldCo consist of 5 subsidiaries;

1

Retail,

commercial,

corporate

banking

Asset

management

and pension

fund

administration

Payment &

switching

services

Consumer

lending &

agency

banking

Insurance

brokerage

Access HoldCo

(ecosystem

orchestrator)

Bank Oxygen Hydrogen Insurance

Brokers

Pensions

14

Value accretion

Agility and scale leverage

Best-in-class talent

Targeted consolidation

Enhanced risk rating beyond the

sovereign

2

3

4

5

1

Creation of Financial Technology play:

✓ Creating new market opportunities &

changing consumer lifestyle and

taste

✓ Guarantee customer service & data

analytics

✓ Creation of new income pools

✓ Optimise valuation

Go Live: Q3 2023

Go Live: Q4 2022

Go Live: Q3 2023

Go Live: Q4 2022

Access Corporation’s footprint will grow significantly in the next

strategic period

Countries of Interest

Existing markets

Nigeria

China

U.A.E

India

Lebanon

France

Malta

Hong Kong

United

States

Niger

Gambia

Kenya

Congo

Ghana

Angola

Zambia

Rwanda

Came-

roon

Tanzania

Morocco

Egypt

Burkina

Faso

Togo

Cote

d’Ivoire

Senegal

Guinea

Ethiopia

Uganda

Republic

of Congo

Mauritius

South Africa

Botswana

Nigeria

Sierra

Leone

Mozam-

bique

Benin

We will capitalize on our strong M&A capability and

ability to build organically to create value with

each expansion through disciplined geographic

growth.

The inorganic M&A opportunities would accelerate

scale within markets in a value accretive manner,

prioritizing countries with better sovereign rating

and complementary business landscape.

This expansion strategy will aid in building a less

risky environment, boost our capital conservation

strategy and develop a more resilient People &

Culture strategy across the Group.

Namibia

15

United Kingdom

S&P: AA/A-1+

Moody’s: Aa3

Fitch: AA

Nigeria

S&P: B-

Moody’s: Caa1

Fitch: B-

Congo

S&P: CCC+

Moody’s: Caa1

Ghana

S&P: B-

Moody’s:

B3

Fitch: B-

Cameroon

S&P: B-

Moody’s: B2

Fitch: B

South Africa

S&P: BB-

Moody’s: Ba2

Fitch: BB-

Botswana

S&P: BBB+

Moody’s: A3

Mozambique

S&P: CCC+

Moody’s: Caa2

Fitch: CCC

Kenya

S&P: B

Moody’s: B2

Fitch: B+

Zambia

S&P:SD

Moody’s: Ca

Fitch: RD

Rwanda

S&P: B+

Moody’s: B2

Fitch: B+

United States

S&P: AA+

Moody’s: Aaa

Fitch: AAA

France

S&P: AA

Moody’s: Aa2

Fitch: AA

Nigeria was downgraded by Moodys and S&P in 2023

Financial and

operating results

16

17

FY’2022 – Resilient financial performance, 1

st

financial institution in Nigeria to

cross gross revenues of N1trn

Total Assets

Cost to Income Ratio

Gross Earnings Shareholders’ Funds

₦1.388trn

+42.8% y/y

₦15.0trn

+27.9% y/y

₦1.2trn

+17.3% y/y

Deposit Growth

57.9%

N9.25trn

+33% y/y

₦302.1b

Market Cap

58m+

Customers

17

Markets

17

₦275.1bn

*Market Cap calculated as at Dec’30

th

Share price position of ₦ 8.50, March 01

st

share price position of ₦9.60 gives Market Cap of ₦341.2b

(Ghana Bond impairment – 103.1bn, Nigeria sovereign downgrade 4.3bn)

Profit Before Tax

+55.6% y/y

(Pre-Impairment adjs)

₦167.7bn

(Post-Impairment adjs)

(5.1%) y/y

6,824

Employees

+0.9% y/y

Access Corporation delivered record earnings, with a stronger balance sheet

solid and improved efficiency

₦’billion

%∆

₦’million

FY 2021

%∆

Metrics FY 2021 % ∆

Non-Interest Income 370,184 51.5

Impairment Charges* (83,213) 137.7

PBT(Post - Impairment adjs) 176,775 (5.1)

Loans and Advances

4,446 25.0

Total Assets 11,732 27.9

Customer Deposits 6,955 33.0

Shareholders’ Funds 1,050

17.3

After-Tax ROAE 17.8% (4.5)

Cost-to-Income

58.8% 0.9

Capital Adequacy 24.5% (4.9)

Liquidity 50.7% (11.2)

Loan-to-Funding 50.8% 7.9

Operating Expenses (371,066) 35.4

Net Interest Income 301,459 19.2

Sustainable

revenue across

income lines

Strong

Balance Sheet

Prudential

Ratios

18

Assets Under Management

**

* Impairment on Ghana Domestic & Eurobonds accounts for N103.1bn of charges, Nigerian sovereign downgrade accounts for N4.3bn

** Access Pensions commenced operations in 2022

N/A

PBT(Pre - Impairment adjs)

176,775

55.6

Gross Earnings 971,885 42.8

Cost of Risk (Loans and Advances)

2.0% 0.6

Cost of Risk (incl impairment on Other Assets)

2.0% 0.2

FY 2022

FY 2022

560,646

(197,790)

167,680

5,557

15,004

9,251

1,231

13.3%

57.9%

19.6%

39.5%

58.7%

(502,359)

359,431

FY 2021FY 2022

896,327

275,080

1,387,911

1.4%

2.2%

Key Income Statement Metrics – drivers of shareholder value creation

19

764.7

971.9

1,387.9

FY'20 FY'21 FY'22

Gross Revenue (in Billions)

106.0

160.3

152.2

FY'20 FY'21 FY'22

Profit After Tax (in Billions)

4.9%

4.3%

4.0%

FY'20 FY'21 FY'22

Net Interest Margin

63.4%

58.8%

57.9%

FY'20 FY'21 FY'22

Cost to Income Ratio

15.6%

17.8%

13.3%

FY'20 FY'21 FY'22

Return on Average Equity

9.0%

8.6%

9.2%

FY'20 FY'21 FY'22

Yield on Asset

Key Balance Sheet Metrics – challenging but strong growth across key lines

.

NPL – Non-Performing Loans

20

1.3%

1.6%

1.1%

FY'20 FY'21 FY'22

Return on Average Assets

8,680

11,732

15,004

Dec'20 Dec'21 Dec'22

Total Assets (in Billions)

5,587

6,955

9,251

Dec'20 Dec'21 Dec'22

Customer Deposits (in Billions)

3,611

4,446

5,557

Dec'20 Dec'21 Dec'22

Net Loans & Advances

4.3%

4.0%

3.1%

FY'20 FY'21 FY'22

NPL Ratio

65%

58%

63%

Dec'20 Dec'21 Dec'22

CASA Ratio

21

Total Assets – increased margin pressure from higher CRR , downward impact on

ROAE

Returns on Assets and Equity

4,954

7,143

8,680

11,732

15,004

2.1%

1.6%

1.3%

1.6%

1.1%

FY'18 FY'19 FY'20 FY'21 FY'22

Total Assets Return on Assets

849*

1,309*

1,466*

2,141*

22.5% 22.5%

27.5% 27.5%

32.5%

CRR

• Access Bank restricted deposits with the CBN has grown at

a rate of 39% over the past 5 years. This is non-interest

generating assets of ₦2.1trn, representing 14% of total assets.

• This significant growth in non-interest bearing assets, in addition

to the interest expenses generated from having the largest Retail

deposit in the Nigerian market, continues to increase the

pressure on Net Interest Margin, despite the healthy growth in

overall Net Interest Income.

• Official Cash Reserve Ratio has steadily grown over the past 5

years, rising to 32.5% in Q4 2022 (FY’18:22.5%) This

represents ₦675bn y/y increment in restricted deposits in FY’

2022.

• Return on Average Asset & Return on Average Equity stood at

1.1% and 13.3% respectively.

579*

1.3%

1.6%

1.1%

15.6%

17.8%

13.3%

FY'20 FY'21 FY'22

ROAA ROAE

* - Refers to Restricted Deposits with Central Bank of Nigeria – non interest bearing assets

Restricted Deposits

Regulatory costs – material growth over the years with significant profitability impact

• Access Banking Group has consistently paid the

highest regulatory fees out of all the five Tier 1

Banks since 2020.Regulatory fees CAGR

growth of c.18% between 2019 – 2022

• The regulatory costs includes the AMCON

charges and the Deposit Insurance Premium

• Significant uplift in PBT is expected, once the

AMCON and other regulatory fees are scaled

back.

14%

16%

17%

16%

13%

13%

14%

14%

15%

15%

16%

16%

17%

17%

-

25.0

50.0

75.0

2019 2020 2021 2022

AMCON & NDIC - Regulatory costs

Total Regulatory Charges Total Reg charges as a % of Total OPEX

489.2

601.7

827.3

114.3

145.0

335.5

116.7

159.2

197.6

44.5

65.9

27.0

FY'20 FY'21 FY'22

Interest Income Trading Income Fee and Commission Income Other Income

Diversified growing franchise that has proven resilient during turbulent times

• Gross earnings grew c. 43% y/y to c. ₦1.39trn in the period (FY’21:

₦971.9bn), comprising c. 60% of interest income and 40% in non-interest

income.

• CAGR increase of +35% over the past 3 years, which denotes sustained

growth and value accretion in the business

• Interest income drivers (+37% y/y, FY’22: ₦827.3bn):

− A 21% y/y increase in interest on Loans and Advances to ₦481.2bn (FY’21:

₦399.2bn) despite the high inflationary environment, Increase in interest income

was driven by a corresponding y/y growth of 25% in the loan portfolio.

− A 64% y/y increase in Interest Income from Investment Securities to ₦333.8bn

(FY’21: ₦203.7)

▪ Non-Interest Income drivers (+53% y/y, FY’22: ₦566bn):

− A 131% y/y growth in trading income to ₦335.5bn from ₦145bn in FY’21,

largely driven by growth in FCY & LCY deposits, for which allocation was done

into safe fixed income investments for both private & public sector

counterparties.

− A 24% y/y increase in Fee & Commission income to ₦197.6bn, largely driven

by increased income from credit related fees and commissions up 107% y/y.

− .

*Interest Income figures calculated as an addition of Interest income on financial assets not at FVTPL/not held for trading and

Interest income on financial assets at FVTPL/held for trading

CAGR %

Gross Revenue (₦’bn)

764.7

971.9

1,387.9

+35% p.a.

23

24

Improved Net Interest Income from stronger loan growth, higher securities yield,

dampened by high Cash Reserve Ratio

489.2

601.7

827.3

FY 2020 FY2021 FY2022

Interest Income

Loans(+25%) growth across all markets

Deposits (+33%) growth across all regions

Higher growth rate in non -interest bearing assets – driven by the growth of

Cash Reserves Ratio over the past 3 years

Higher cost of funds. Higher interest expenses (minimum interest on

savings deposit increased from 10% to 30% of MPR rate) for c.2.2m savings

customers from multiple MPR rate increases in 2022.

Active cost of deposit management and loans repricing to support positive

NIM growth

Level of yields from securities still relatively low in comparison to

inflation growth

• xx

Margin

Management

Volume

Growth

Higher

Interest Rates

Key NIM & COF Drivers

9.0%

8.6%

9.2%

3.3%

3.4%

4.1%

4.9%

4.3%

4.0%

FY 2020 FY2021 FY2022

Asset Yield (YOA) Cost of Funds Net Interest Margin

*CAGR %

*+30% p.a.

*+44% p.a.

226.3

300.2

467.8

FY 2020 FY2021 FY2022

Interest Expense

263.0

301.5

359.4

4.9%

4.3%

4.0%

0.0%

2.0%

4.0%

6.0%

0

100

200

300

400

FY 2020 FY2021 FY2022

Net Interest Income Net Interest Margin

2,302

2,568

3,890

1,310

1,492

1,898

1,975

2,895

3,462

Dec'20 Dec'21 Dec'22

Demand Savings Term

Continued focus on better balance sheet mix

Net Interest Margin (NIM)

Customer Deposits (₦’bn)

+29% p.a.

32%

20%

30%

CAGR, %

Customer deposits increased by 33% y/y to ₦9.25trn in

the period (Dec’21: ₦6.95trn), from the positive impact of

our channel optimization strategy on customer acquisition

and deposit mobilization.

Term deposits grew to ₦3.46trn from ₦2.89trn with (20%

y/y growth), as we locked in rates to mitigate the prevailing

interest rate environment

CASA

(1)

account deposits stood at ₦5.78trn (Dec’21:

₦4.1trn), accounting for 63% of customer deposits. This is

due improved customer acquisition, leveraging technology

and innovation and expanded agency network to increase

financial inclusion

1. Current accounts and savings accounts

25

2,565

4,256

5,587

6,955

9,250

50%

58%

65%

58%

63%

0%

10%

20%

30%

40%

50%

60%

70%

-

2,000

4,000

6,000

8,000

10,000

Dec'18 Dec'19 Dec'20 Dec'21 Dec'22

CASA MIX

Total CASA MIX

370.9

17

29.9

7.3

18.8

13.3

24.1

21.1 502.4

2021 FY

Actuals

Admin related Wages related New market

expansion

IT

Infrastructure

Spend

Regulatory

fees

Premises &

Prof Fees

Others 2022 FY

Actuals

26

Operating expenses growth aligned with inflation & targeted growth activities

• Overall Cost to Income ratio improved by c. 92bps y/y to

57.9% (FY’21: 58.8%) as revenues grew, we doubled down on

cost containment strategies, and continued with investment in

Infrastructure & Technology to support scale and next phase of

growth.

• Impact of the continuous investment from the last strategic cycle,

beginning to show in strong growth across all revenue lines

• Growth in operating expense by 35% y/y to ₦502.4bn (FY’21;

₦370.9bn) - driven by the double - digit inflationary environment

pushing up wages, growth in regulatory fees, impact of FX

devaluation, Full year impact of three new banking subsidiaries

recognized in 2022.

• IT Expenses – upgrade and revamp of existing IT infrastructure,

investment in core banking model (Flexcube) and upgrades to the

data warehouse infrastructure.

• Movement in “Others” includes Cash processing fees, security

related fees, Depreciation charges.

• Cost of Risk increased by 20bp y/y to 2.2% (FY’21: 2.0%), on

the back of Ghana sovereign debt impairments. However, Cost of

Risk on Loans and Advances dropped from 2.0% in 2021 to 1.4%

in 2022.

Operating Expenses (₦’bn), CoR and CIR

New Market Expansion relates to full year impact of new subsidiaries, South Africa, Mozambique, Guinea and Cameroon

Inflation driven

Regulatory

driven

+35%

Growth Driven

326.5

370.9

502.4

1.8%

2.0%

2.2%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

-

100.0

200.0

300.0

400.0

500.0

600.0

FY'20 FY'21 FY'22

Operating Expense Cost of Risk

Cost to Income

63.4%

58.8%

57.9%

27

Performance by Business Segments – broad base of profit generation

• Sizeable portion of Holding Company costs relates to professional fees incurred for the M&A transactions during the acquisition of the Pensions business, personnel costs and others

• Impairment from Ghana domestic & Eurobonds accounts for N103.1bn of charges, Nigerian sovereign downgrade accounts for N4.3bn

• Banking Group Entity includes intercompany balances

Notes

PBT- Profit Before Tax

Access Banking Group –

Capital & Liquidity Management

28

Customer

Deposits

62%

Deposits from

Financial

Institutions

13%

Debt Securities

Issued

2%

Interest-Bearing

Borrowings

9%

Other Liabilities

6%

Equity

8%

…..underpinned by a commitment to balance sheet strength

Funding sources (%)

• Capital Adequacy Ratio (CAR) is above regulatory limit of 15% at 20.2%* ,

down 4.3% YoY(Dec’21: 24.5%).

• Risk Weighted Assets (RWAs) grew by ₦1.4trn (+28% y/y), primarily driven by

strong, cautious and quality growth in the group's asset-book (42% y/y growth in

credit risk)

• Customer deposits continue to dominate the Bank’s funding mix at 62%, as we

deepen wallet share of corporates, commercial and retail customers.

• Liquidity ratio remained well in excess of regulatory minimum at 39.5%

(Dec’21: 50.7%)

• Drop in liquidity ratio was largely due to a significant increase in restricted deposits

y/y with the Central Bank of Nigeria

• Access Banking Group is well capitalized with regulatory capital above the

minimum requirement of 15%

Capital and Liquidity (₦’bn)

29

Capital Adequacy Computation - Basel II

Dec’22:

₦15.1trn

3,828

4,892

6,291

19.6%

24.5%

20.6%

46.0%

50.7%

39.5%

Dec'20 Dec'21 Dec'22

RWA (₦’bn)

Capital Adequacy Ratio Liquidity Ratio

Access Banking Group –

Asset Quality

30

12%

11%

11%

9%

7%

7%

5%

5%

5%

5%

4%

4%

4%

3%

3%

2%

2%

1%

General Commerce

Oil & Gas - Services

Finance and Insurance

Government

Construction

General

Others

Oil & Gas - Upstream

Oil & Gas - Downstream

Real Estate

Info. & Comm.

Food Manufacturing

Manufacturing - Others

Transportation

Cement

Steel

Conglomerates

Oil and Gas - Refinery

………….healthy growth in loan book post pandemic lockdowns

Gross Loan Distribution by Sector

Dec’22 Loans &

Advances to

customers:

₦5.6trn

Sector

3,611

4,446

5,557

Loans & Advances to customers

(₦’bn)

+24% p.a.

• Well diversified gross loan book of c. ₦5.6trn as at Dec’22 (Dec’21:

₦4.4trn), reflecting our strategic approach of mitigating concentration

risk with quality credit to critical and growth sectors of the economy.

• The FCY as a share of the loan book increased to 23.7% (Dec’21

19.7%).

• Loan-to-Funding ratio closed at 58.7% as at Dec’22 (Dec’21:

50.8%), reflective of a healthy and cautious growth in the loan book.

Loans by Currency

(1) The following sectors are included in “Others”: Agriculture, Education, Basic Metal Products, Flourmills & Bakeries, and Power & Energy

CAGR, %

31

74.1%

80.3%

76.3%

25.9%

19.7%

23.7%

Dec'20 Dec'21 Dec'22

LCY FCY

3,218

4,161

5,101

393

285

456

Dec'20 Dec'21 Dec'22

Loans & Advances to Customers Loans & Advances to Banks

Dec’22

11.4%

5.2%

14.4%

6.5%

5.7%

4.4%

4.2%

3.5%

2.6%

4.1%

4.0%

2.1%

2.7%

2.2%

0.2%

10.8%

7.4%

8.6%

12.2%

4.8%

11.4%

6.9%

4.9%

4.9%

4.4%

4.9%

4.3%

4.3%

3.4%

2.7%

1.9%

1.9%

0.8%

6.9%

8.8%

10.7%

Dec’21

Continued improvement in our Assets Quality

NPL Distribution by Sector

NPL Ratio by Sector

Dec’’22

Gross NPLs:

₦176.9bn

Oil and Gas Services

Oil & Gas - Upstream

Real Estate Activities

Food Manufacturing

Agriculture

Manufacturing - Others

General Commerce

Dec’21

13.0%

Dec’22

Others

Oil and Gas - Downstream

General

9.7%

6.1%

6.0%

4.1%

6.3%

8.2%

14.5%

8.6%

5.9%

Transportation and Storage

4,4%

Construction

Information and Comm.

0.3%

1.0%

Steel Rolling Mills

• Asset quality continues to improve, with NPL ratio down to 3.1%

(Dec’21: 4.0%).

• This is hinged on proactive post - disbursement monitoring and

robust risk management practices.

• 89% of gross loans in stage 1 classification underpinned by

strong asset performance and minimal credit risk in the loan

portfolio.

NPL Analysis

(1) The following sectors are included in “Others”: Education, Finance & Insurance, Government, Basic Metal

Products, Cement, Conglomerates, Flourmills & Bakeries, Oil & Gas Refinery, and Power & Energy

0.6%

32

161.2

181.5

176.9

121.6%

86.5%

100.4%

4.3%

4.0%

3.1%

Dec'20 Dec'21 Dec'22

NPLs (₦'bn)

NPL Coverage NPL Ratio

0.0%

0.2%

0.3%

3.8%

3.9%

4.3%

4.4%

4.8%

5.4%

5.5%

5.8%

8.0%

8.8%

9.6%

Sector

Dec’22

17.1%

4.1%

13.4%

9.8%

7.2%

5.6%

2.1%

7.3%

3.4%

3.6%

0.7%

8.4%

6.4%

11.1%

Dec’21

16%

13%

13%

11%

10%

8%

8%

7%

6%

3%

2%

2%

1%

0%

General Commerce

Manufacturing - Others

General

Information and Communication

Transportation and Storage

Real Estate Activities

Construction

Food Manufacturing

Oil & Gas - Downstream

Steel Rolling Mills

Others

Agriculture

Oil and Gas Services

Oil & Gas - Upstream

16.5%

2.7%

13.1%

9.5%

8.3%

6.6%

2.4%

6.1%

1.7%

0.7%

0.0%

8.5%

11.2%

12.6%

Access Banking

Group – Subsidiaries

performance

33

34

African & International Subsidiaries’ Performance

Key takeaways

African Subsidiaries

• Revenue: ₦206.6bn up 13%y/y (FY’21:

₦182.8bn)

• Impairments: ₦63.2bn up 329% y/y (FY’21:

₦14.7bn)

• Deposits from customers: ₦1.1trn up 10% y/y

(FY’21: ₦1.0trn)

• Ghana 28%, Botswana 23%, Zambia 10%

contribution.

• Loans and Advances: ₦498.3bn up 9%

(FY’21:455.3bn)

• Ghana Sovereign debt restructuring impacted

subsidiary stand alone PBT by c.132% y/y (FY’

21: N34.2bn

• New Subsidiaries

• Cameroon (operational May 2022)

• South Africa (operational March 2021)

• Botswana(operational Oct 2021)

• Cameroon and Mozambique have broken

even and contributed c.N2.5bn PBT to

African subsidiaries' revenue in FY’ 22

International Subsidiaries

• Revenue: ₦70.0bn up 22%y/y (FY’21: ₦57.2bn)

• Impairments: ₦15.9bn up 8% y/y (FY’21:

₦14.7bn)

• Deposits from customers: ₦577bn up 10% y/y

(FY’21: ₦396.9bn)

• Loans and Advances: ₦1.1trn up 36%

(FY’21:810.1bn)

• France subsidiary approval received – H2 2023

kick off expected .

PBT

PBT

*Banking Group Entity includes intercompany balances of N10.1bn

28.5

47.6

-6.0

FY'20 FY'21 FY'22

Africa Subsidiaries

7.3

22.6

25.1

FY'20 FY'21 FY'22

International Subsidiaries

35

Update on Ghana Sovereign debt situation

Key takeaways

Key updates

Next Steps

Government

of Ghana’s

action timeline

• The Domestic Debt exchange closed on 10

th

of February. Final

results from the Ghana’s Ministry of Finance shows participation in

the exchange was approximately 85% of eligible holders.

• Estimate that the Eurobond debt will have to be reduced in nominal

terms by between 25% and 30%, with the potential for an additional

reduction in the level of the interest coupons, on which the

Government has not been clear

• Unlike the DDE, which has now closed, restructuring of the foreign

bonds is at a much earlier stage and negotiations have barely

begun

• The restructuring will look to adhere to the common framework,

with NPV as the basis and not the asset base of the country,

given Ghana is a low-income country.

• Lazard, working on behalf of the Ghanaian Government is

concluding an economic model which will serve as the primary

basis for the restructuring

• African Group set up by Renaissance Capital alongside other

Africa based Eurobond holders, will begin engaging Lazard & the

Government of Ghana in the coming weeks . Targeted completion

date for restructuring is within 6 months

4

th

Dec 2022

❖ Impact of Ghana Eurobonds on Access

Banking Group

• Access Bank Group Exposure to Ghanaian’s

Eurobond is c.2.3% of Access Banking Group’s

total assets.

❖ Specific Actions Being Taken by Access Bank

Ghana

• Participation in the Domestic Debt Exchange

Programme

• Ongoing Deposit Mobilization

• Diversification of Revenue Lines

• Cost Optimization

• Contingency Funding

• Review of government related borrowing

❖ Group Level

• Independent Market Review

• Market Analyst Engagement

• Internal actions taken to create appropriate

reserves to support potential fallout

24

th

Dec 2022 27

th

Jan 2023

BoG suspends

payments on most of

its’ external debts

BoG launched a

Domestic Debt

Exchange

programme

Provision of range of

discount rates for the

valuation of domestic bonds

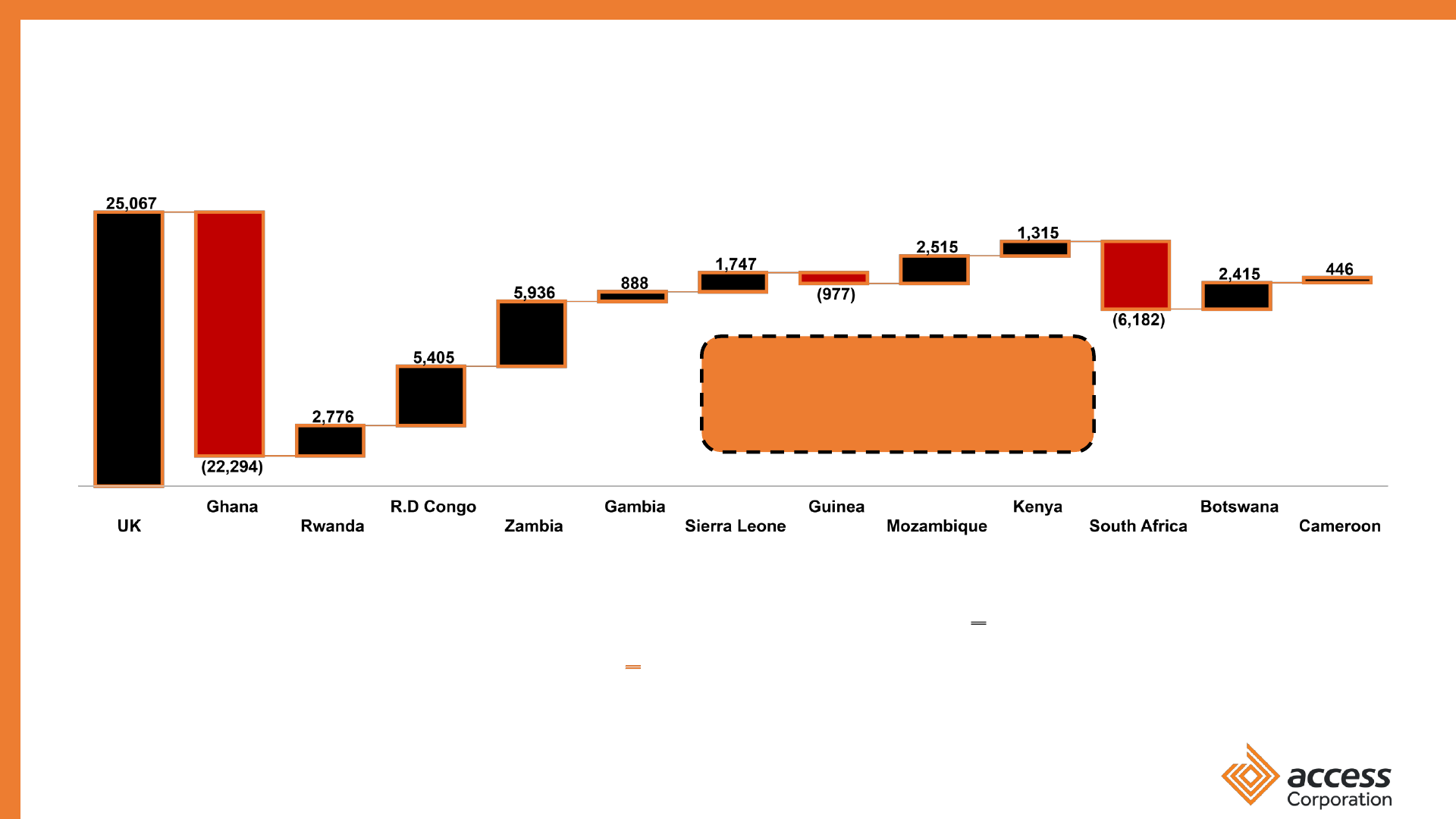

Subsidiaries’ performance dampened by Ghana Sovereign Debt Restructure

PBT (₦,bn)

• Subsidiaries’ contribution to the Banking Group’s performance stood at 11% (FY’21: 38%), with a PBT of ₦19.1bn

• Access Bank UK and Ghana accounted for 59% of Africa subsidiaries’ operating income of N198bn, up 11% y/y

• Access Bank Ghana recorded a PBT loss position of N22.3bn largely due to a c.30% write down in the value of investment securities in the

African subsidiary. We have commenced series of actions to mitigate and minimize future impairments

• Total deposits from subsidiaries amounted to ₦2.67trn contributing c. 23% (FY21: 20%) of total Banking Group deposits

Subsidiary contribution to

PBT : ₦19.1Bn

Access Banking Group:

Digital Lending

37

96,919

145,860

167,896

FY 2020 FY 2021 FY 2022

Increased scale and velocity of our digital lending – unlocking strategic value

Digital lending count, #,Thousand

Digital lending value, ₦’million

32% p.a.

-23% p.a.

~₦167.9bn disbursement, a 15% y/y growth from ₦145.9bn in

FY’21

~2,384,223 digital loans in the year, a 24% y/y decrease from

3,153,466 in FY’21. This is on the back of more stringent

eligibility criteria

~₦23.6bn digital lending revenue generated, 85% y/y

growth from ₦12.7bn in FY’21.

Products

Small Ticket Personal Loans

Pay day Loans

Device Financing

Salary Advance

38

3,997

3,153

2,384

FY 2020 FY 2021 FY 2022

Drove transaction income through enhanced digital channels transaction

velocity

39

Channels

Count FY’22 (mn) Count FY’21 (mn) Value ’22 (₦’bn) Value FY’21 (₦’bn)

YonY Growth YonY Growth

Debit/Credit Card 431 419 5,974 4,0386% 15%

POS 41 71 1,267 1,6872% 17%

Mobile & Internet

Banking

639 447 57,757 36,76254% 34%

ATM 136 159 2,070

2,161

USSD 805 782 2,424 1,92011% 8%

Total 2,055 1,880 69,494 47,02812 % 29%

(2%)

6%

403

39

296

146

590

156,747

Count FY’20 (mn) Value FY’20 (₦’bn)

3,966

783

24,027

1,759

2,377

32,457

Total channels transaction count, ₦’million

Total channels transaction value, ₦’billion

+46% p.a.

+18% p.a.

39

1,476

1,880

2,055

FY 2020 FY 2021 FY 2022

32,457

47,028

69,494

FY 2020 FY 2021 FY 2022

Forward looking

Guidance

40

PROFITABILITY

ASSET QUALITY

EFFICIENCY

PRUDENTIAL RATIOS

Return on Average

Equity

Return on Average

Assets

Yield on Asset

Cost of Risk

NPL Ratio

Cost-to-Income Ratio

Net Interest Margin

Loan-to-Deposit Ratio

Capital Adequacy Ratio

Liquidity Ratio

<60%

>5%

<2%

<5%

>20%

>50%

>65%

18%

>2%

>10%

2027 Targets

<55%

>6%

<1.5%

~3%

>20%

>60%

>65%

25-30%

>2%

>10%

2023 Targets

Access Corporation: Financial Targets

AUM (N’trn)

6.3

1.3

NIM is expected to be at least 6% in

2027, this growth in NIM will be driven

by increased lending within the core

Bank and by the growth in LendCo’s

business which will typically have

higher margins on average.

Healthy ROAE returns expected over

the next 5 year as we continue to

maximise returns for shareholders.

2023 target includes the impact of

the recently added capital to Access

Bank via AT1 .

ROE along with ROA are expected to

grow, as a result of improvements in

CIR and an increase in footprint

across higher efficiency locations

Key Takeaways

Source: Access Corporation Financial Model

Conclusion

The institution has transitioned to a Holdco with 5

verticals to capture the opportunities the African market

provides as the landscape evolves over the next few

years

Capital accumulation and protection over time despite

investments in infrastructure and growth – expected to

continue into the future

Access has positioned itself to be at the centre of

financial flows on the continent – trade, expanding and

deepening financial services and serving corporates with

excellence – creating a self sustaining ecosystem

Access will create a high-performance organization with a

strong bench of talent who are the best African leaders

with capabilities to deliver the corporation’s future

aspirations

Access Bank over the last twenty years has built a

strong financial institution through a disciplined

approach to executing its strategy which has

produced market beating results consistently and has

been value accretive

Access Corporation’s ambitions will be supported by 7 key

enablers. These enablers will ensure Access executes

seamlessly, becoming a Top 5 financial services institution

in the Continent by the end of the strategic cycle in terms

of revenues, asset base and on a balanced scorecard

basis

42

©Access Corporation 2022

Access Corporation

Investor Relations

Contact Information

Webpage: https://theaccesscorporation.com/investor-relations/

E-Mail: Investor[email protected]