Finance and Economics Discussion Series

Divisions of Research & Statistics and Monetary Affairs

Federal Reserve Board, Washington, D.C.

Disentangling the Effects of the 2018-2019 Tariffs on a Globally

Connected U.S. Manufacturing Sector

Aaron Flaaen and Justin Pierce

2019-086

Please cite this paper as:

Flaaen, Aaron, and Justin Pierce (2019). “Disentangling the Effects of the 2018-2019 Tar-

iffs on a Globally Connected U.S. Manufacturing Sector,” Finance and Economics Discus-

sion Series 2019-086. Washington: Board of Governors of the Federal Reserve System,

https://doi.org/10.17016/FEDS.2019.086.

NOTE: Staff working papers in the Finance and Economics Discussion Series (FEDS) are preliminary

materials circulated to stimulate discussion and critical comment. The analysis and conclusions set forth

are those of the authors and do not indicate concurrence by other members of the research staff or the

Board of Governors. References in publications to the Finance and Economics Discussion Series (other than

acknowledgement) should be cleared with the author(s) to protect the tentative character of these papers.

Disentangling the Effects of the 2018-2019 Tariffs on a

Globally Connected U.S. Manufacturing Sector

∗

Aaron Flaaen

Federal Reserve Board

Justin Pierce

Federal Reserve Board

December 23, 2019

Abstract

Since the beginning of 2018, the United States has undertaken unprecedented tariff

increases, with one goal of these actions being to boost the manufacturing sector. In

this paper, we estimate the effect of the tariffs—including retaliatory tariffs by U.S.

trading partners—on manufacturing employment, output, and producer prices. A key

feature of our analysis is accounting for the multiple ways that tariffs might affect the

manufacturing sector, including providing protection for domestic industries, raising

costs for imported inputs, and harming competitiveness in overseas markets due to

retaliatory tariffs. We find that U.S. manufacturing industries more exposed to tariff

increases experience relative reductions in employment as a positive effect from import

protection is offset by larger negative effects from rising input costs and retaliatory

tariffs. Higher tariffs are also associated with relative increases in producer prices via

rising input costs.

∗

We are grateful to Vivi Gregorich for superb research assistance. We thank Ryan Monarch and partici-

pants at the 2018 Mid-Atlantic Trade Workshop at Duke for useful comments. Any opinions and conclusions

expressed herein are those of the authors and do not necessarily represent the views of the Board of Governors

or its research staff.

1

1 Introduction

The unprecedented increase in tariffs imposed by the United States against its major trading

partners since early 2018 has brought renewed attention to the economic effects of tariffs.

While there are already vast theoretical and empirical literatures documenting the effects of

changes in trade policy, it is not clear how prior estimates apply to the present day when

there are virtually no modern episodes of a large, advanced economy raising tariffs in a way

comparable to the U.S. in 2018-2019. Further complicating the process of estimating the

effects of tariffs is the rapid expansion of globally interconnected supply chains, in which

tariffs can have impacts through channels beyond their traditional effect of limiting import

competition.

Another important feature of these tariffs is that they were imposed, in part, to boost the

U.S. manufacturing sector by protecting against what were deemed to be the unfair trade

practices of trading partners, principally China. Thus, while existing research has mostly

documented negative consequences of the tariff increases on the broad economy–including

higher prices, lower consumption, reduced business investment, and drops in the valuations

of affected firms–some might view these effects as an acceptable cost for achieving the policy

aim of ensuring more robust manufacturing activity in the United States.

This paper provides the first comprehensive estimates of the effect of recent tariffs on

the U.S. manufacturing sector. A key feature of this analysis is accounting for the different

ways that tariffs could affect manufacturers in the presence of global trade and supply chain

linkages. On the one hand, U.S. import tariffs may protect some U.S.-based manufacturers

from import competition in the domestic market, allowing them to gain market share at

the expense of foreign competitors. On the other hand, U.S. tariffs have also been imposed

on intermediate inputs, and the associated increase in costs may hurt U.S. manufacturers’

competitiveness in producing for both the export and domestic markets. Moreover, U.S.

trade partners have imposed retaliatory tariffs on U.S. exports of certain goods, which could

again put U.S. firms at a disadvantage in those markets, relative to their foreign competitors.

Disentangling the effects of these three channels and determining which effect dominates is

an empirical question of critical importance.

Toward this end, we construct straightforward industry-level measures of exposure to each

of these three channels. We measure the import protection channel as the share of domestic

absorption affected by newly imposed tariffs. We account for declines in competitiveness

associated with increased input costs as the share of industry costs subject to new tariffs.

Finally, we measure an industry’s potential exposure to retaliatory tariffs by U.S. trading

partners as the share of industry-level exports subject to new retaliatory tariffs. We construct

these measures using detailed data on each industry’s input-output structure, trade flows,

and shipments, as well as information on the set of products covered by both U.S. and foreign

2

retaliatory tariffs. We then relate the measures for these three channels of tariff exposure to

monthly data on manufacturing employment, output, and producer prices.

We employ a differences in differences approach that compares outcomes in industries

that are more subject to each of the three tariff channels to those that are less affected.

We begin by regressing the industry-level outcomes on interactions of measures of the three

channels with a set of month dummies, which allows us to observe the timing of any effects

of tariffs, while also determining whether more-exposed industries were on differential trends

prior to the start of trade tensions. We adopt two approaches to control for potential pre-

trends, including using detrended measures of the dependent variables, and differencing out

the effect of the pre-trends as in Finkelstein (2007). Industry and month fixed effects in the

regressions control for time-invariant characteristics of industries and aggregate shocks. In

addition, we control for industries’ import share of domestic absorption and export share

of shipments to allow for the possibility, for example, that more internationally exposed

industries may perform differently at different stages of the business cycle.

We find that tariff increases enacted in 2018 are associated with relative reductions in

manufacturing employment and relative increases in producer prices. In terms of manufac-

turing employment, rising input costs and retaliatory tariffs each contribute to the negative

relationship, and the contribution from these channels more than offsets a small positive

effect from import protection. For producer prices, the relative increases associated with

tariffs are due solely to the rising input cost channel. We find little evidence for a relation-

ship between industrial production and any of the three tariff channels considered.

In terms of economic significance, we find that shifting an industry from the 25th per-

centile to the 75th percentile in terms of exposure to each of these channels of tariffs is

associated with a reduction in manufacturing employment of 1.4 percent, with the positive

contribution from the import protection effects of tariffs (0.3 percent) more than offset by

the negative effects associated with rising input costs (-1.1 percent) and retaliatory tariffs

(-0.7 percent). For producer prices, we find that an interquartile shift in exposure to rising

input costs is associated with a 4.1 percent increase in factory-gate prices. These estimates

provide information about the responses of more-exposed relative to less-exposed industries,

but do not reflect general equilibrium effects of the tariff increases.

The results point to the importance of increased costs from tariffs on inputs as a mecha-

nism through which tariffs affect the manufacturing sector, with this channel yielding highly

statistically significant effects for both employment and producer prices. The importance

of this channel in our estimates is consistent with the purposeful targeting of intermediate

inputs for early rounds of U.S. tariffs in order to avoid tariffs on consumer goods, as discussed

in section 2. Furthermore, the results point to the relevance of global supply chains when

evaluating the effects of tariffs.

These results necessarily represent short-term effects of tariffs, and the longer-term impli-

3

cations of trade tensions may differ from those estimated here. For example, some adjustment

to the imposition of tariffs may take time as firms complete previously agreed-upon contracts

with customers and suppliers. Furthermore, some effects may dissipate if tariffs were to re-

turn to their previous levels, while others may be longer-lived. We also note that this paper

focuses specifically on realized changes in tariffs, but does not explicitly consider the effects

of increased uncertainty about future trade policy. Indeed, the increase in uncertainty gen-

erated by recent rounds of tariff increases may be one of the ways in which the effects of past

policy persist.

This paper builds on the evolving literature examining the effects of recent global trade

tensions on the U.S. economy. Early work in this literature includes Amiti, Redding and

Weinstein (2019) and Fajgelbaum et al. (2019) who find near-complete pass-through of U.S.

tariff increases to domestic prices, implying welfare losses, though of a relatively small mag-

nitude. Cavallo et al. (2019) show that product composition appears to be a key determinant

in the differences in tariff pass-through between U.S. imports and U.S. exports during the

2018-2019 tariff escalation, while also showing that the majority of U.S. tariff increases are

being absorbed by U.S. retailers. Flaaen, Horta¸csu and Tintelnot (2019) examine the case

of U.S. tariffs imposed on washing machines, showing that tariffs on individual countries can

lead to the relocation of production across borders, while tariffs on a broader sets of coun-

tries lead to substantial retail price increases for both targeted products and complementary

goods. Handley, Kamal and Monarch (2019) find that those firms impacted by U.S. import

tariffs respond by reducing U.S. exports, consistent with our finding of the importance of

the intermediate input channel. Huang et al. (2019) find that the effects of tariffs also carry

through to firms’ financial performance, with firms more engaged in trade with China expe-

riencing lower stock returns and higher default risk after the announcement of new rounds

of tariffs targeting China.

Focusing on the effects of retaliatory tariffs on consumption, Waugh (2019) finds that

counties specializing in industries subject to Chinese retaliatory tariffs experienced reductions

in new auto sales. Blanchard, Bown and Chor (2019) also find that these retaliatory tariffs

can explain a shift in voting away from Republican House candidates in the 2018 election.

In research focusing on uncertainty regarding tariff rates, Caldara et al. (2019) find that

increases in measured trade policy uncertainty reduce investment in firm-level and aggregate

data. Other research (Reyes-Heroles, Traiberman and Van Leemput 2019) notes that the

effects of tariff actions by major trading countries can also have implications for the trade

patterns of emerging market economies.

Although we highlight the recent and rapidly expanding literature on the 2018-2019

tariffs, the ideas of accounting for retaliatory tariffs and supply chain effects of tariffs go back

decades. Early examinations of optimal tariffs given the potential for retaliation can be found

in Kaldor (1940) and Johnson (1953). The counteracting effect of tariffs on intermediate

4

inputs used in further domestic production–the rising input cost channel described above–

was highlighted in Balassa (1965) and also Corden (1966). The scale of the 2018-2019

tariffs, the increased availability of data, and the immensely expanded network of global

supply chains permits a quantitative examination of these channels that was not possible

before.

Our paper makes several contributions to the existing literatures. First, we explicitly

measure and estimate the effects of several channels through which tariffs could affect man-

ufacturers, which we find to be important given that tariffs can simultaneously protect an

industry’s output, while raising prices for its inputs and subjecting it to retaliation in its

export markets. Second, we focus specifically on the manufacturing sector, the sector whose

output and employment were targeted to be boosted by tariffs. We believe this focus is

important, because our results indicate that tariffs have been a drag on employment and

have failed to increase output. Third, we provide the first simultaneous examination of the

output, employment, and price effects of the 2018-2019 tariffs in a particular sector.

The remainder of the paper proceeds as follows. Section 2 describes the timing of recent

trade actions by the U.S. and its trading partners, lists the data sources used in the analysis,

and details the calculation of the three measures of exposure to tariffs. Section 3 presents

our empirical strategy and results and Section 4 concludes.

2 Background, Data, and Industry-Level Measurement

2.1 Recent Trends in U.S. Manufacturing

We begin by providing some brief background on recent trends in manufacturing activity

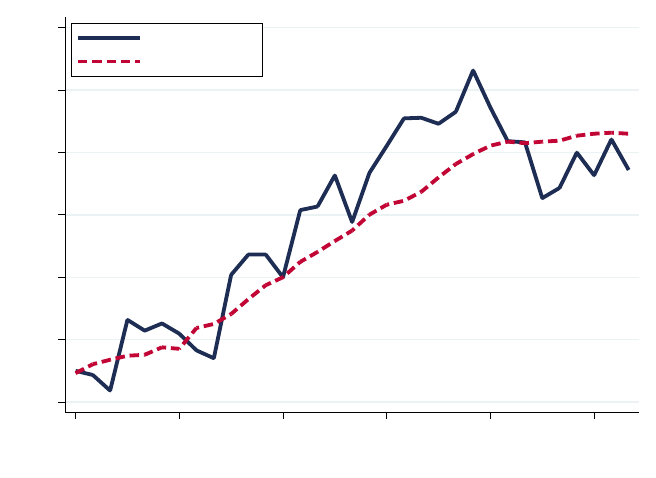

in the period leading up to and during the imposition of tariffs. Toward that end, Figure

1 displays manufacturing employment and production from January 2017 to August 2019,

with each data series converted to an index that equals 100 in January 2018, just before

the imposition of the first round of new tariffs. As indicated in the Figure, manufacturing

employment and output increased at a robust pace in 2017 and, indeed, through much of

2018. Since the end of 2018, however, manufacturing output has declined noticeably and

manufacturing employment growth has stalled. Given this inflection point, which came

after the imposition of substantial tariffs by the U.S. and its trading partners, it seems

reasonable to ask whether the tariffs implemented or planned in 2018 played some role in

this manufacturing slowdown. Given the patterns evident in Figure 1, it is now helpful to

provide additional detail on the timing of the implemented tariffs we study.

5

Figure 1: Measures of Manufacturing Activity: 2017m1 to 2019m8

98 99 100 101 102 103 104

Jan. 2018 = 100

2017 2018 2019

Jan Jul Jan Jul Jan Jul

IP

Employment

Sources: Federal Reserve Board (FRB) for industrial production; U.S. Department of Labor, Bureau of

Labor Statistics for employment.

2.2 Timing of U.S. and Retaliatory Tariffs

The escalation in tariffs beginning in 2018 can be classified under three separate actions,

which occurred on distinct timelines and were subject to distinct rounds of retaliatory tariffs.

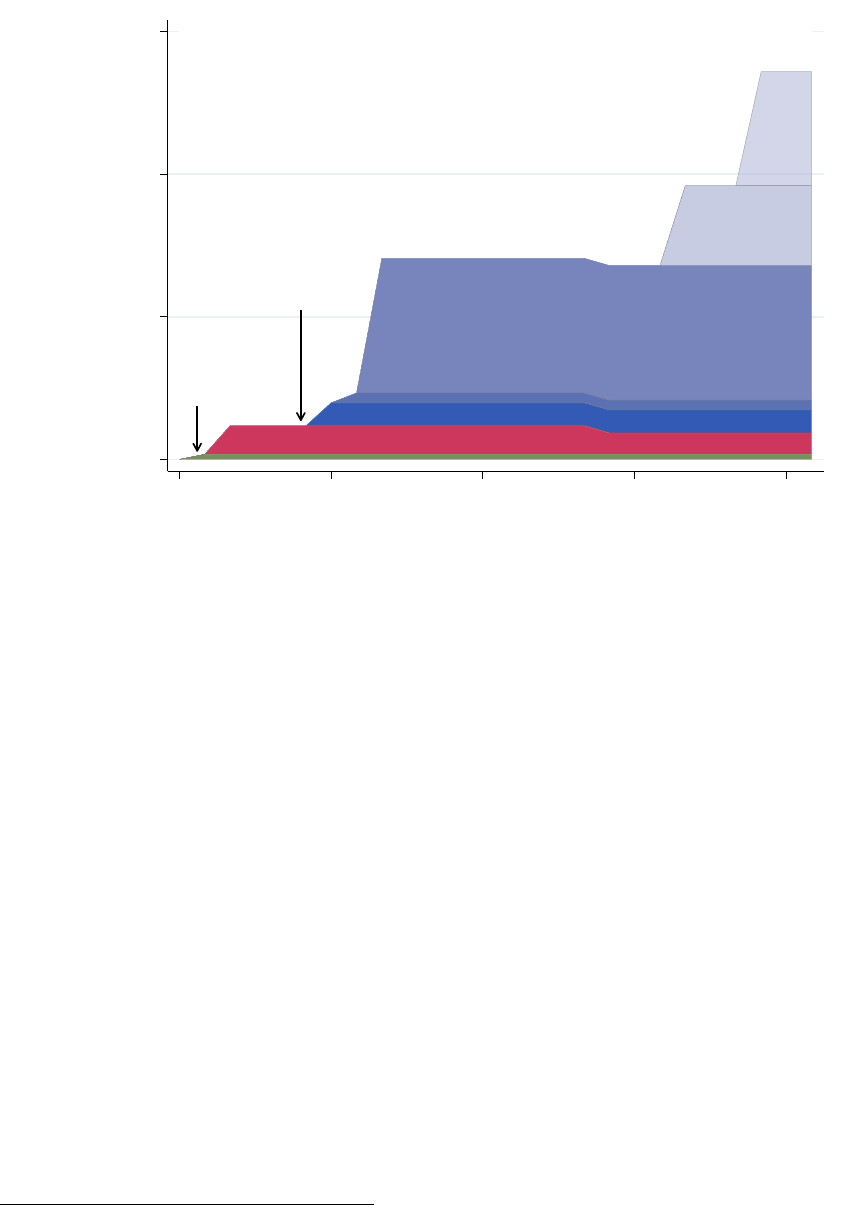

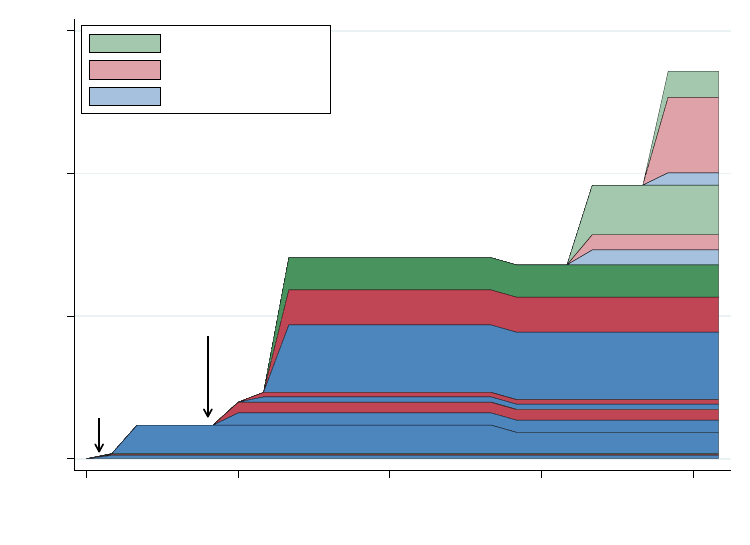

Figures 2 and 3 display the scope and timing of these trade actions.

The first tariff action was enacted in early February 2018 against large residential washing

machines and solar panels/modules. Applying the rarely used Section 201 of the Trade Act

of 1974, these tariffs affected all import partners based on a determination of “whether an

article is being imported in such increased quantities that it is a substantial cause of injury,

or threat thereof, to the U.S. industry producing an article like or directly competitive with

the imported article” (U.S. Code: Title 19, Code 2252). These tariffs are scheduled to last

for three years before automatically expiring. The value of 2017 U.S. imports affected by

these tariffs is shown by the green area in Figure 2.

The second major tariff action affected steel and aluminum imports beginning in March

2018. In only the third instance of its use by the United States, the U.S. administration

self-initiated an investigation under Section 232 of the Trade Expansion Act of 1962, which

determines whether an imported product is being imported “in certain quantities or under

such circumstances as to impair or threaten to impair U.S. national security” (U.S. Code:

Title 19, Code 1862). The announced tariff rates were applied at 25 percent on steel and

certain steel products and 10 percent on aluminum. The administration initially exempted

the imports of several countries, including Canada, Mexico, Korea, and the countries com-

6

prising the European Union; however, in June 2018 these exemptions were removed.

1

The

value of imports affected by these tariffs is shown by the red area in Figure 2.

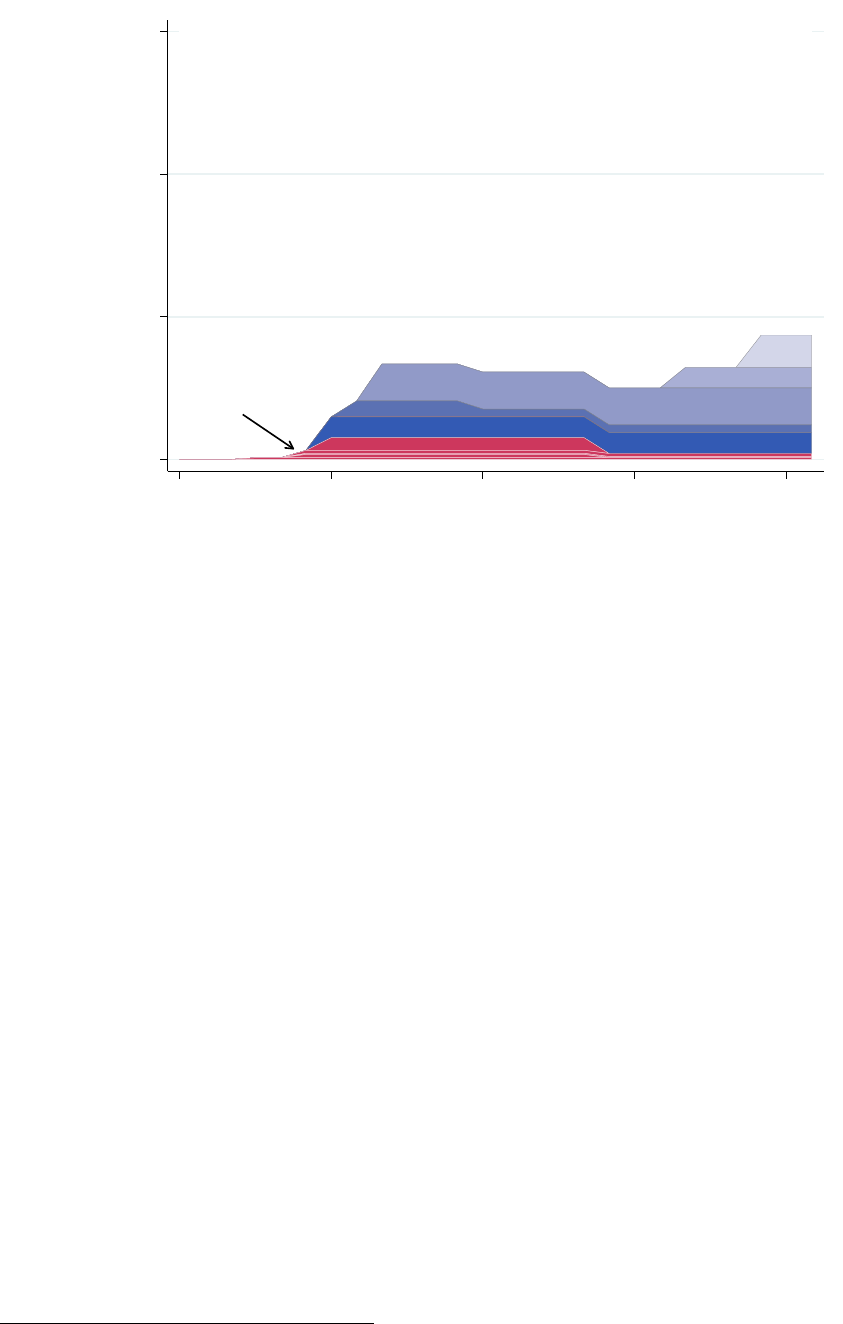

In response to this second action, China announced retaliatory tariffs on U.S. exports

in April of 2018, while the European Union, Canada, and Mexico followed with their own

retaliatory tariffs in June and July of 2018. These tariffs focused on aluminum waste, scrap,

pork and various agricultural products for the case of China, and steel, aluminum and other

agricultural goods for the cases of the E.U., Canada, and Mexico. The value of 2017 U.S.

exports subject to these retaliatory tariffs is shown by the red portion of Figure 3. The

equal scales of the axes in Figures 3 and 2 makes clear that the magnitude of retaliation on

U.S. exports has been significantly lower than the level of tariffs applied by the U.S. on its

imports.

The third and most significant tariff action imposed tariffs on U.S. imports from China

based on Section 301 of the Trade Act of 1974. This provision provides enforcement mecha-

nisms against a wide range of trade practices deemed to be unjustifiable, unreasonable, dis-

criminatory, or that violate trade agreements. The initial section 301 investigation against

Chinese trade practices focused on intellectual property and technology transfer. The re-

sults of the investigation were released in March of 2018, and tariffs on Chinese goods were

announced in April. These tariffs were actually applied in several phases as both the United

States and China retaliated against import tariffs imposed on one another. Phase 1 of U.S.

tariffs occurred in July 2018, targeting $34 billion of Chinese imports, with additional Phase

2 tariffs on $16 billion following in August. Each of these initial phases were set at a rate of

25 percent. The largest set of tariffs, which covered nearly $200 billion of Chinese imports,

went into effect in late September 2018 at a rate of 10 percent. These initial phases of the

section 301 tariffs can be seen as the blue areas of Figure 2.

Each of these phases of U.S. tariffs against Chinese imports was accompanied by Chinese

retaliatory tariffs on U.S. exports. Retaliation on Phases 1 and 2 covered equivalent dollar

values of U.S. exports at identical rates, while the Phase 3 covered a smaller amount — $60

billion of U.S. exports — at rates ranging from 5-10 percent. These values are shown in the

blue areas of Figure 3.

There was an extended lull in the exchanges of U.S.-China tariffs between October 2018

and April 2019 as negotiations between the two sides took place. In May of 2019, citing a re-

treat from Chinese commitments in previous rounds of the negotiations, the U.S. announced

that the Phase 3 tariffs would be increased to 25 percent beginning May 10th. China re-

taliated by raising tariff rates on a little over half of its Phase 3 retaliatory tariffs. Further

U.S. tariffs were announced in August 2019, but fall outside our period of analysis: a Phase

4 of U.S. tariffs against roughly $110 billion in Chinese imports to take effect in September

1

The Republic of Korea managed to secure a permanent exemption after agreeing to stringent import

quotas to the U.S. market.

7

Figure 2: Timeline of New U.S. Import Tariffs: 2018-2019

Solar Panels,

Wash. Mach.

Sec.201: $7B

Steel, Aluminum

Sec. 232: $40B

Chinese Imports

Sec. 301: $506B

0 200 400 600

Billions of USD (Based on 2017 Imports)

2018m1 2018m7 2019m1 2019m7 2020m1

Sources: USITC for 2017 import values. See Table A1 for details on the set of relevant products and trade

values.

Notes: Our analysis below covers only the 2018 rounds of tariffs.

2019, and a Phase 5 of tariffs against roughly $160 billion in December 2019. China once

again retaliated with a plan for additional tariffs on U.S. exports to take effect with a similar

timing.

As we highlight below, the effect of these tariffs on the U.S. manufacturing sector depends

at least in part on how they impact global supply chains. U.S. manufacturers competing

with Chinese imports would fare quite differently than manufacturers that rely on Chinese

inputs in their U.S. production. For a rough guide for how these tariffs were split along this

dimension, we apply the United Nations Broad Economic Categories (BEC) classification

to these tariffs (see also Bown, Jung and Lu (2019b) for a similar breakdown).

2

As shown

in Appendix Figure B1, the early U.S. tariffs predominantly covered intermediate goods,

represented by the blue areas of the section 232 and initial section 301 phases of U.S. tariffs.

There were some reports that this focus on intermediate goods over consumer goods was a

purposeful effort on the part of the United States to shield U.S. consumers from any effects

of tariffs.

2

Of course, the BEC classification does not substitute for analysis using input-output tables, as one U.S.

industry’s final good output can be another industry’s intermediate input.

8

Figure 3: Timeline of Retaliatory Tariffs on U.S. Exports: 2018-2019

Mexico, Turkey, Russia

China, EU, Canada

& Aluminum Tariffs

Retaliation on Steel

Retaliation on

Sec. 301 Tariffs

China

0 200 400 600

Billions of USD (Based on 2017 Exports)

2018m1 2018m7 2019m1 2019m7 2020m1

Sources: USITC for 2017 export values. See Table A2 for details on the set of relevant products and trade

values.

2.3 Data and Measurement

This section describes the data sources and measurement for the empirical analysis presented

in Section 3. We use publicly available data on the sets of products covered by U.S. import

tariffs and foreign retaliatory tariffs. For U.S. tariffs, product lists are from the United States

Trade Representative and as published in the U.S. Federal Register. For retaliatory tariffs

by U.S. trade partners, data are drawn from the relevant government agencies including

the Canadian Department of Finance, the European Commission, as well as the World

Trade Organization. These lists of affected products have been helpfully collected by other

researchers who have made them available on their websites.

3

Table A1 provides a list of

links to all lists of affected products.

We map the Harmonized System (HS) codes covered by tariffs described above to the

North American Industry Classification System (NAICS) using the concordance developed

by Pierce and Schott (2012). For U.S. import tariffs, this requires a simple application of

the concordance. For tariffs imposed by U.S. trade partners, this process is complicated by

the fact that the import product codes published by foreign governments cannot be matched

to the Schedule B system used for U.S. exports below the six-digit HS level. Therefore, for

foreign retaliatory tariffs, we treat an entire six-digit HS code as being covered by tariffs if any

product with that six-digit HS prefix is covered by a tariff, following Blanchard, Bown and

3

See, for example, the website, maintained by the Crowell-Moring International Trade law firm and Bown

and Kolb (2019).

9

Chor (2019), Waugh (2019) and Bown, Jung and Lu (2019a). We find that this assumption

is justified because the value of U.S. exports that we classify as being covered by retaliatory

tariffs lines up well with those calculated by other researchers as well as those announced by

U.S. trade partners, as reported in Table A2.

Our measures of exposure to the various rounds of tariffs imposed by the U.S. and its

trading partners also require data on the value of overall imports, exports and shipments.

We collect data on the dollar value of U.S. imports and exports from the United States

International Trade Commission. For annual levels of industry shipments, we use the most

recent year of the Annual Survey of Manufactures (ASM), 2016. Data on the input usage

of each industry are drawn from the BEA’s input-output tables for 2012, the most recent

vintage available.

Lastly, we draw monthly values of the dependent variables for our analysis—industry

output, employment, and producer prices—from three sources. Our measures of monthly

industry output come from the Federal Reserve’s G.17 Release on Industrial Production

and Capacity Utilization. For monthly estimates of employment at the industry-level, we

utilize data from the Current Employment Statistics (CES) program of the Bureau of Labor

Statistics. Finally, we use the producer price index, also from the Bureau of Labor Statistics,

to measure monthly changes in prices across industries.

2.4 Level of Aggregation

We conduct the analysis at the level of four-digit NAICS industries, which is the most de-

tailed level at which comprehensive data for industrial production, producer prices, and

employment are available at a consistent level of aggregation, with several exceptions. First,

we separate aluminum manufacturing (NAICS 3313) into three sub-industries to reflect an

important distinction within the industry that is impossible to ignore given the set of tariffs

we study. Primary aluminum production (NAICS 331313) consists of establishments largely

making aluminum from raw materials like alumina and bauxite. The remaining components

of NAICS 3313 (NAICS 331314: Secondary Smelting and Alloying of Aluminum, NAICS

331315: Aluminum Sheet, Plate, and Foil Manufacturing, and NAICS 331318: Other Alu-

minum Rolling, Drawing, and Extruding) manufacture aluminum from scrap, dross, or other

existing aluminum. As is clear from this definition, primary aluminum manufacturers would

be protected by the U.S. tariffs on aluminum, while the same tariffs would apply to both the

output and inputs of the second group of producers. Therefore, we split NAICS 3313 into

primary aluminum production (NAICS 331313), secondary aluminum production (NAICS

331314), and the combination of NAICS 331315 and 331318, consistent with the industry

splits used in the BEA input-output tables.

Second, there are exceptions to the use of the four-digit NAICS classification due to data

limitations. In particular, there are some industries (NAICS 315: Apparel Manufacturing,

10

and NAICS 316: Leather and Allied Product Manufacturing) where declining domestic pro-

duction has made 4-digit NAICS detail increasingly uncommon in U.S. federal statistics. We

have therefore used the 3-digit classification for these two industries. Data on manufacturing

employment and producer prices also lack sufficient detail on the aluminum splits detailed

above, and so we use the aggregate NAICS 3313. After factoring in the necessary aggrega-

tions, our baseline samples contain 76 industries for employment, 84 industries for industrial

production, and 81 industries for producer prices.

2.5 Industry-Level Measures of Trade Policy Impact

This section describes the measures we construct to quantify the industry-level effects of the

trade policies enacted by the U.S. and its trading partners in 2018. Our focus in construct-

ing these measures is capturing the effect of realized changes in tariffs on forces likely to

impact outcomes in the manufacturing sector, including the amount of import competition

in the U.S. market, foreign demand for U.S. exports, and input costs. In particular, we

construct three industry-level measures capturing each of these channels of potential trade

policy impact. Uncertainty regarding trade policy may have led to additional effects; indeed,

uncertainty has been a prominent focus of industry anecdotes as well as academic research

(see, for example Caldara et al. (2019)).

New Tariff Import Share of Domestic Absorption

One of the most salient ways in which tariffs could affect an industry’s economic activity is by

restricting foreign competition. To measure the extent of this potential protection, we relate

the scale of imports affected by new tariffs to the level of domestic absorption. Formally,

let Ω

I

be the list of U.S. imported product-country pairs (pc) subject to new tariffs. The

variables imp

i

and exp

i

identify total industry i imports and exports, and Q

i

equals domestic

production. Then, the new tariff import share of domestic absorption is given by:

Import Protection

i

=

P

pc∈Ω

I

imp

ipc

Q

i

+ imp

i

− exp

i

. (1)

Throughout the remainder of the draft, we typically refer to this measure as an industry’s

degree of “import protection” from the 2018 tariffs.

4

In our baseline results, we calculate equation (1) for the cumulative set of tariffs from

2018 as a whole.

5

Table 1 lists the top ten industries from this cumulative measure of

4

Our measures of the channels of tariff effects are based on country-product-level trade flows, but do not

incorporate information on the ad valorem tariff rate assessed. In the case of U.S. tariffs, the overwhelming

majority of import value was covered by ad valorem rates that were either initially set at or eventually

reached 25 percent.

5

In Appendix B.3 we describe additional results in which we calculate separate measures of import

11

new import protection. Despite the focus on China-specific tariffs in media coverage of

recent trade actions, the global tariffs – Section 232 tariffs on steel and aluminum and the

Section 201 tariffs on washing machines and solar panels – play a prominent role in this

list of protected industries.

6

Other industries such as electric lighting equipment (NAICS

3351), household and institutional furniture and kitchen cabinets (NAICS 3371), and other

electrical equipment and component (NAICS 3359) are primarily affected by the U.S. tariffs

on Chinese imports.

Table 1: Top Ten Industries by New Import Protection

New Tariff

Import Share

Rank NAICS Industry Description of Absorption

1 331313 Primary Aluminum Production 67%

2 3351 Electric Lighting Equipment 30%

3 3371 Household and Institutional Furniture

and Kitchen Cabinet

24%

4 3344 Semiconductor and Other Electronic

Component

21%

5 3311 Iron and Steel Mills and Ferroalloy Mfg 21%

6 33131B Aluminum Sheet/Plate/Foil and

Rolling/Drawing/Extruding

19%

7 3352 Household Appliance Manufacturing 18%

8 3359 Other Electrical Equipment & Component 16%

9 3160 Leather and Allied Product 15%

10 3332 Industrial Machinery 14%

Sources: Authors’ calculations based on equation (1) in the text.

Notes: This measures corresponds to the cumulative effect of all new tariffs

from January through September 2018.

New Tariff Export Share of Output

While U.S. tariffs may reduce competition for some industries in the domestic market, U.S.

trading partners responded to these tariffs by imposing retaliatory tariffs. These retaliatory

tariffs may harm U.S. manufacturers by decreasing their competitiveness in foreign markets.

We measure this potential effect as the share of U.S. output that has been impacted by

new retaliatory tariffs. Defining Ω

E

to be the list of U.S. exported product-country pairs

(pc) subject to retaliatory tariffs, we calculate the new tariff export share of output – which

we refer to as an industry’s exposure to “foreign retaliation” – as the following:

protection for each individual wave of tariffs.

6

Solar panels and modules are included in NAICS industry 334413; NAICS industry 3344 is listed as

number 4 in Table 1 though this industry comprises a wide range of chips, microprocessors, and other

electrical components.

12

Foreign Retaliation

i

=

P

pc∈Ω

E

exp

ipc

Q

i

. (2)

The ten industries most affected by new foreign retaliatory tariffs (for 2018 as a whole)

are shown in Table 2. As is clear from the table, even the most affected industries experience

increases in tariffs on less than 10 percent of their overall shipments.

7

Table 2: Top Ten Industries by New Tariff Export Share of Output

New Tariff

Export Share

Rank NAICS Industry Description of Output

1 3346 Manufacturing and Reproducing

Magnetic & Optical Media

8.6%

2 3160 Leather and Allied Product 7.7%

3 33131B Aluminum Sheet/Plate/Foil &

Rolling/Drawing/Extruding

7.7%

4 3311 Iron and Steel Mills and Ferroalloy Mfg 6.9%

5 3361 Motor Vehicle Manufacturing 4.9%

6 3352 Household Appliance 4.7%

7 3211 Sawmills and Wood Preservation 4.5%

8 3343 Audio and Video Equipment 4.3%

9 3253 Pesticide, Fertilizer, and Other

Agricultural Chemical

4.1%

10 3341 Computer and Peripheral Equipment 3.9%

Sources: Authors’ calculations based on equation (2) in the text.

Notes: This measures corresponds to the cumulative effect of all new tariffs

from January through September 2018.

New Tariff Share of Costs

The final channel we study traces the impact of U.S. tariffs on input costs via supply chain

linkages with foreign countries. The principal data on an industry’s sources of inputs used in

U.S. production are the input-output tables produced by the Bureau of Economic Analysis.

At the core of these tables are the “make” and “use” tables. The “use” table provides a

matrix use

ij

–the dollar value of commodity j used in industry i production, and similarly

the “make” table provides a matrix make

ij

–the dollar value of commodity j produced in

industry i production. It is helpful to first consider the overall share of an industry’s costs

coming from foreign sources. Define SC

ij

as the share of input costs of commodity j in

industry i:

S

ij

=

use

ij

M

i

+ Comp

i

, (3)

7

This measure of retaliatory tariffs includes retaliatory tariffs by China on U.S. exports of motor vehicles

(NAICS 3361), which were imposed in July of 2018, but then suspended in January 1, 2019.

13

where the variable M

i

equals total intermediate uses of industry i, and Comp

i

equals

compensation of employees of industry i. Then, define IS

j

as the import share of domestic

supply of commodity j:

IS

j

=

imp

j

Q

j

+ imp

j

, (4)

where here the variables imp

j

and Q

j

, are imports and output of commodity j, respec-

tively. By multiplying the terms from equations (3) and (4) we arrive at the (implied) import

share of costs in industry i from commodity j. Without additional detail on the sources of

inputs across countries, here we must use the “proportionality assumption”: that the dis-

tribution of the uses of imported commodities in an industry is proportional to domestic

commodity usage. Summing across commodities j yields the total import share of costs for

industry i. This implied import share of costs is given by:

ISC

i

=

X

j

ISC

ij

=

X

j

use

ij

M

i

+ Comp

i

| {z }

product share

of costs

imp

j

Q

j

+ imp

j

| {z }

product import

share

(5)

We use data from the BEA’s 2012 input-output tables, the most recent year available,

updated with 2016 information on values of imports and shipments. To incorporate the

more recent data, we separate our measure of input usage into two components. The first

component, Equation (3) uses only data from the 2012 detailed I-O tables and measures the

share of total costs of each commodity j for an industry i. The second component, Equation

(4), uses the more recent data on output and imports. It is worth pointing out that we are

only able to update equation (4) for manufactured goods, as annual output measures for

non-goods are unavailable. For non-goods commodities, we will use the 2012 values that

come from the IO-tables.

Finally, we construct our measure of an industry’s share of costs subject to new tariffs

to be the share of equation (5) that is covered by new U.S. import tariffs. We refer to this

measure below as the degree of “rising input costs” for a given industry, and calculate it as

follows:

14

Rising Input Costs

i

=

X

j

NT SC

ij

=

X

j

use

ij

M

i

+ Comp

i

P

pc∈Ω

I

imp

jpc

Q

j

+ imp

j

, (6)

where as before the term Ω

I

denotes the list of U.S. imported product-country pairs (pc)

subject to new tariffs.

Table 3 lists the top domestic industries most affected by increased costs from recent

import tariffs, where once again we show the cumulative effects from all new 2018 tariffs.

As is apparent in the table, all of these industries are heavily dependent on various met-

als for domestic production. In some cases, such as the most affected industry, aluminum

sheet/plate/foil (NAICS 33131B), our measures indicate that any benefits of increased im-

port protection are offset by increases in costs.

8

Table 3: Top Ten Industries by New Tariff Import Share of Costs

New Tariff

Share

Rank NAICS Industry Description of Costs

1 33131B Aluminum Sheet/Plate/Foil &

Rolling/Drawing/Extruding

17.6

2 3312 Steel Product Mfg from Purchased Steel 8.4

3 3324 Boiler, Tank, and Shipping Container 8.3

4 3321 Forging and Stamping 7.4

5 331313 Primary Aluminum Production 7.2

6 331314 Secondary Smelting and Alloying of Aluminum 7.1

7 3323 Architectural and Structural Metals 5.3

8 3369 Other Transportation Equipment 5.0

9 3339 Other General Purpose Machinery 4.5

10 3352 Household Appliance 4.4

Sources: Authors’ calculations based on equation (6) in the text.

Notes: This measures corresponds to the cumulative effect of all new tariffs

from January through September 2018.

3 Short-Run Impacts of Tariffs on Manufacturing

This section presents the differences-in-differences empirical strategy we use to estimate the

relationship between recent tariffs and outcomes in the manufacturing sector and presents

our baseline results.

8

This is a result of a significant degree of input requirements “on the diagonal” of the use tables published

by the BEA.

15

3.1 Empirical Strategy

The distribution of our measures of tariff impacts across industries, shown in part in Tables 1,

2, and 3 demonstrates the need for a systematic approach to decompose the impacts of tariffs

on the manufacturing sector. Any bivariate relationship between an outcome measure and

one of the channels identified above could end up conflating multiple, potentially offsetting

effects on an industry. Hence, we will control for all channels of exposure to tariffs in our

baseline specification, allowing us to calculate estimates of the effect of each channel holding

the others constant, and determining which tariff channel dominates.

In addition, rather than designating a set period of time over which to analyze the effects

of tariffs on the outcome variables, we adopt a flexible setup that allows the effects of each

of the channels to vary over time. In particular, we interact the industry-level measures

for each of the tariff channels with a full set of month dummies. This allows us determine

the exact timing of any estimated tariff effects in high-frequency data, while also providing

information on the presence of any differential pre-existing trends in outcome variables across

industries.

Finally, recognizing that international trade will have industry-level effects even in the

absence of changes in trade policy, we include additional controls that account for a baseline

level of export and import exposure for each industry.

9

These controls should account for

general exposure to international conditions such as changes in the value of the dollar and

foreign GDP growth. In addition, these controls may also serve as a coarse proxy for exposure

to trade policy uncertainty.

Our estimating equation is given by:

y

it

= α +

X

t

γ

t

1(M

t

= t)(Import Protection

i

) +

X

t

θ

t

1(M

t

= t)(Input Cost

i

) ... (7)

+

X

t

λ

t

1(M

t

= t)(Foreign Retaliation

i

) + +

X

t

ω

t

1(M

t

= t)(Import Share

i

) ...

+

X

t

ϕ

t

1(M

t

= t)(Export Share

i

) + δ

i

+ δ

t

+ ε

it

where 1(M

t

= t) indicates a monthly categorical variable, and the outcome of interest,

y

it

, is either log employment, log output, or the log of the producer price index of industry

i in time t.

One concern inherent in this type of differences-in-differences analysis is the issue of

differing trends across industries prior to the implementation of new tariffs. We utilize two

approaches to account for pre-trends. First, we replace the measure y

it

with the equivalent

measure after removing an industry-specific trend in 2017 (denoted ey

it

), the last full year

9

Our export exposure measure is simply the export share of output (from 2016), and the import share of

domestic absorption (also from 2016).

16

before the implementation of new tariffs. In a second approach, we estimate equation (7)

and then follow Finkelstein (2007) by differencing out the pre-trend path for each coefficient,

thereby arriving at a point estimate of the particular channel for the period of our study.

Specifically, for a given coefficient (say, the γ

t

coefficient above) we calculate the following:

∆y

γ

it

= (

γ

Jun-Aug19

− γ

Mar18-May18

) − (γ

Mar18-May18

− γ

Feb17-Apr17

) (8)

where we utilize the average of March-May, 2018, as the approximate period (t = 0) of the

cumulative 2018 tariffs, with the end period being the average of the last three months of

our sample (June-August, 2019) and the pre-period being the average of three months from

an equivalent number of months before (February-April, 2017).

3.2 Results

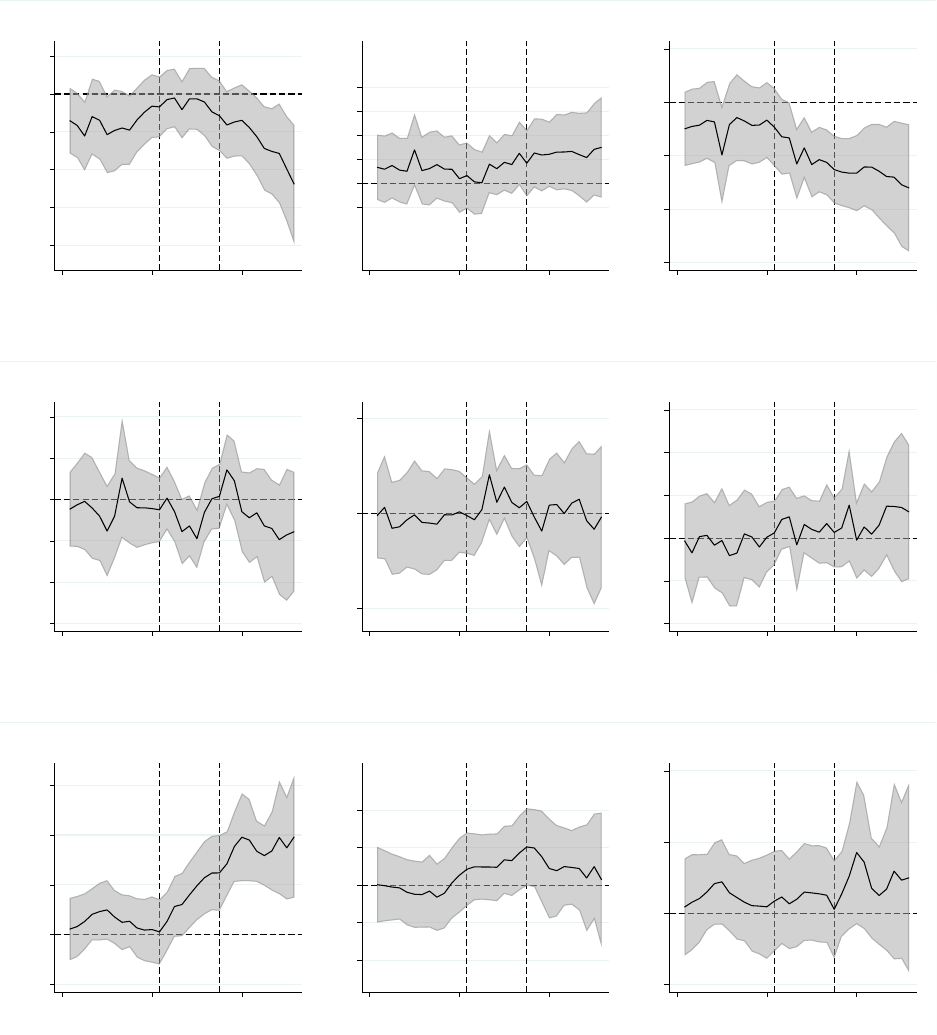

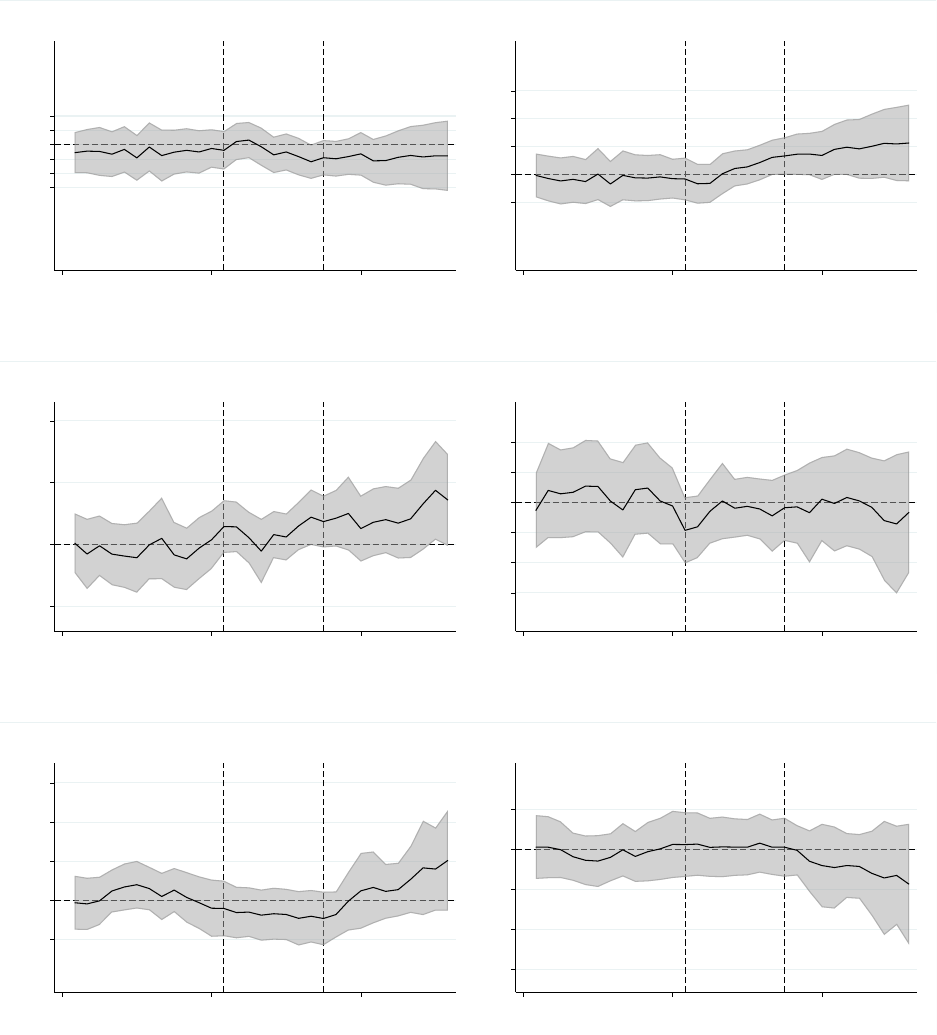

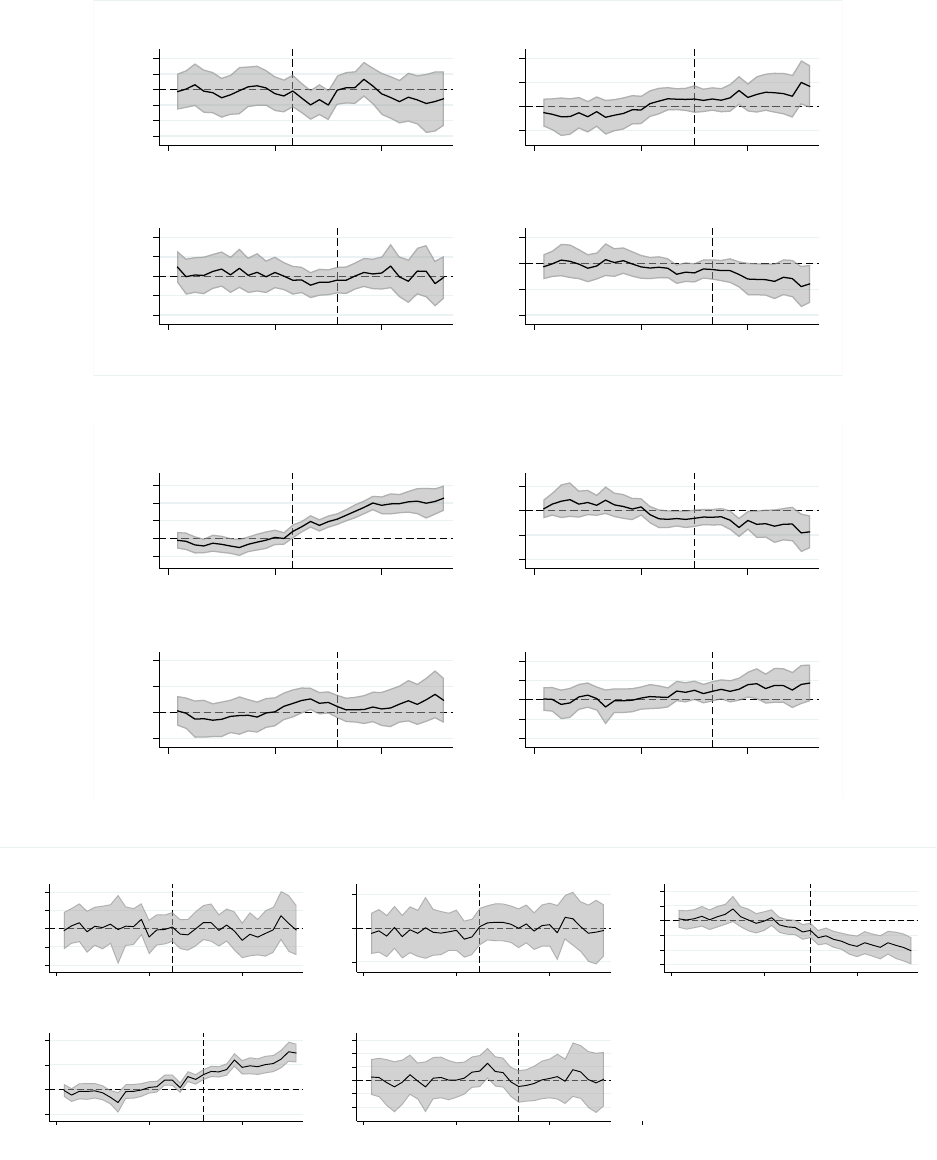

Figure 4 provides a visual representation of the results of equation (7) when using the

industry-detrended (ey

it

) outcomes of interest. Specifically, the three panels of the figure

display the 90 percent confidence intervals of the coefficient estimates for the interactions of

the tariff channel measures with the month dummies. The dashed vertical lines indicate the

timing of the first (February) and last (September) trade actions imposed by the U.S. and

its trading partners in 2018.

Panel A displays estimated effects for detrended employment. The left column of panel

A shows a negative and statistically significant relationship between the rising input cost

effect of tariffs and manufacturing employment. An interesting feature of this relationship

is that it materializes with a lag following the application of tariffs affecting U.S. imported

intermediates, suggesting that the effects of this channel take some time to manifest itself

in manufacturing employment. This result, therefore, provides additional context for the

aggregate trends shown in Figure 1, in which manufacturing activity did not slow noticeably

until the end of 2018. The middle column of panel A indicates a modest positive effect on

employment associated with import protection, but these estimates are somewhat imprecise.

Finally, the right column of panel A exhibits a negative effect of foreign retaliatory tariffs on

U.S. manufacturing employment that is apparent immediately after retaliatory tariffs begin

to be imposed. For all three sets of estimates shown in panel A of Figure 4, coefficient

estimates during the period prior to the implementation of tariffs are reasonably flat, though

not always centered exactly around zero.

The first column of Table 4 provides alternative estimates of the relationship between the

tariff channels and employment based on the de-trending approach from Finkelstein (2007)

described above. These estimates are consistent with those reported in Figure 4, and also

17

Figure 4: Effects of Cumulative Tariffs (Detrended)

(a) Employment

-.8 -.6 -.4 -.2 0 .2

90% CI

2017m1 2018m1 2019m1 2020m1

Rising Input Costs

-.05 0 .05 .1 .15 .2

90% CI

2017m1 2018m1 2019m1 2020m1

Import Protection

-1.5 -1 -.5 0 .5

90% CI

2017m1 2018m1 2019m1 2020m1

Foreign Retaliation

(b) Industrial Production (Output)

-1.5 -1 -.5 0 .5 1

90% CI

2017m1 2018m1 2019m1 2020m1

Rising Input Costs

-.5 0 .5

90% CI

2017m1 2018m1 2019m1 2020m1

Import Protection

-2 -1 0 1 2 3

90% CI

2017m1 2018m1 2019m1 2020m1

Foreign Retaliation

(c) Producer Price Index

-1 0 1 2 3

90% CI

2017m1 2018m1 2019m1 2020m1

Rising Input Costs

-.2 -.1 0 .1 .2

90% CI

2017m1 2018m1 2019m1 2020m1

Import Protection

-1 0 1 2

90% CI

2017m1 2018m1 2019m1 2020m1

Foreign Retaliation

Sources: Federal Reserve Board (FRB), U.S. Department of Labor, Bureau of Labor Statistics; authors’

calculations.

Notes: Each panel represents separate regressions, with each row of plots corresponding to the first three

components of equation (7), after removing an industry-specific trend in the dependent variable. The shaded

areas represent 90 percent confidence intervals, and the two dashed lines represent February 2018 and

September 2018, the first and last wave of new 2018 tariffs.

provide a more straightforward way of characterizing their economic significance. We find

that shifting an industry from the 25th percentile to the 75th percentile in terms of exposure

to each of the three channels of tariffs is associated with a reduction in manufacturing

18

employment of 1.4 percent, with the positive contribution from the import protection effect

of tariffs (0.3 percent) more than offset by the negative effects associated with rising input

costs (-1.1 percent) and retaliatory tariffs (-0.7 percent).

10

Panel B of Figure 4 presents the coefficient estimates pertaining to the relationship be-

tween tariffs and industrial production. Here, we see little evidence of significant impacts

from the 2018 tariffs, on net, though there is a brief period of a negative relationship with the

input cost channel in mid-2018 and a noticeable shift down in estimates toward the end of

our sample. The estimates pertaining to the other channels – import protection and foreign

retaliation – do not exhibit statistically significant patterns. Point estimates in column 2 of

Table 4 similarly lack statistical significance.

Finally, panel C of Figure 4 indicates that these new tariffs had significant effects on

producer prices, primarily through the pass-through of rising input costs (the left column).

There is also suggestive evidence that producer prices rose modestly through the import

protection channel (the middle column); however, the estimates lack precision. Although one

might expect negative effects on producer prices impacted by foreign retaliatory tariffs, we

see no evidence for this in our analysis (the right column). In terms of economic significance,

the estimates in column 3 of Table 4 indicate that an interquartile shift in exposure to rising

input costs is associated with a 4.1 percent increase in factory-gate prices.

Table 4: Point Estimates of Cumulative Effect by Channel:

Industrial Producer

Variable Employment Production Prices

Import Protection 0.080* -0.042 -0.053

(0.049) (0.165) (0.069)

Rising Input Costs -0.463*** -0.357 1.780***

(0.122) (0.330) (0.486)

Foreign Retaliation -0.506** 0.180 0.341

(0.249) (0.657) (0.538)

Industry Fixed Effects yes yes yes

Number of Industries 76 84 81

Observations 2,440 2,688 2,586

Sources: Federal Reserve Board (FRB), U.S. Department of Labor, Bureau of

Labor Statistics; authors’ calculations.

Notes: See equations (7) and (8) in the text. Robust standard errors in paren-

theses. ∗ p < 0.10, ∗∗ p < 0.05, ∗ ∗ ∗ p < 0.01.

10

An alternative way of calculating the economic significance of these estimates is to consider the effect of

shifting the average industry—in terms of exposure to the three channels—to an alternative scenario with

zero tariff exposure. This change in exposure to tariffs is also associated with a 1.4 percent relative reduction

in employment. We caution, however, that this estimate does not account for additional general equilibrium

effects that might be associated with the recent tariffs, which might be the result of either changes to applied

tariffs or uncertainty regarding future tariffs.

19

3.3 Discussion

The results presented in Figure 4 and Table 4 pertain to the set of tariffs enacted in 2018,

with estimated effects through August 2019. As additional data become available, it may

be possible to estimate effects of the Phase 4 tariffs against Chinese imports enacted in

September 2019. Our results suggest that the effects of this later round of tariffs will be

highly dependent on the composition of affected products. As shown in Appendix Figure

B1, the September 2019 U.S. tariffs focused to a much greater extent on consumer goods

rather than the intermediate inputs that were heavily targeted in the 2018 tariff actions.

Therefore, the input cost channel could play a smaller role in the effects of the 2019 tariffs

on the manufacturing sector.

We also note that the longer-run effects of these tariffs could be qualitatively different

than the short-run effects that we estimate here. On the one hand, there may be more

substantial expansion of U.S. manufacturing activity in the longer-term as firms fully adjust

their supply chains to avoid U.S. import tariffs, highlighting a potential longer lag structure

for the import protection channel. That said, there is suggestive evidence that the United

States is not typically the immediate destination for production relocation from China due

to increased tariffs. In the washing machine case studied in Flaaen, Horta¸csu and Tintelnot

(2019), firms first moved production to other East Asian countries (Thailand and Vietnam)

following China-specific antidumping duties imposed in mid-2017. After the later Section

201 tariffs against worldwide imports of washing machines (discussed above), these same

firms did indeed shift some sizable production to the United States, though this occurred

with substantial costs to consumers via rising prices.

4 Conclusion

This paper examines the effect of the tariff increases imposed by the United States and its

trading partners in 2018 on outcomes in the U.S. manufacturing sector. We calculate mea-

sures of each industry’s exposure to tariff changes via three channels: the import protection

that comes when an industry’s output is subject to U.S. tariffs, the increase in production

costs resulting from tariffs on imported inputs, and the reduction in foreign competitiveness

due to retaliatory tariffs in U.S. export markets. We then estimate the relationship between

these measures of exposure to tariffs and manufacturing employment, output, and producer

prices.

We find that the 2018 tariffs are associated with relative reductions in manufacturing

employment and relative increases in producer prices. For manufacturing employment, a

small boost from the import protection effect of tariffs is more than offset by larger drags

from the effects of rising input costs and retaliatory tariffs. For producer prices, the effect

of tariffs is mediated solely through rising input costs.

20

These results have implications for evaluating the effects of recent U.S. trade policy.

While one may view the negative welfare effects of tariffs found by other researchers to be an

acceptable cost for a more robust manufacturing sector, our results suggest that the tariffs

have not boosted manufacturing employment or output, even as they increased producer

prices. While the longer-term effects of the tariffs may differ from those that we estimate

here, the results indicate that the tariffs, thus far, have not led to increased activity in the

U.S. manufacturing sector.

In addition, our results suggest that the traditional use of trade policy as a tool for

the protection and promotion of domestic manufacturing is complicated by the presence of

globally interconnnected supply chains. While the potential for both tit-for-tat retaliation

on import protection and input-output effects on the domestic economy have long been rec-

ognized by trade economists, empirical evidence documenting these channels in the context

of an advanced economy has been limited. We find the impact from the traditional import

protection channel is completely offset in the short-run by reduced competitiveness from

retaliation and higher costs in downstream industries.

21

References

Amiti, Mary, Stephen J. Redding, and David Weinstein. 2019. “The Impact of the

2018 Trade War on U.S. Price and Welfare.” Journal of Economic Perspectives, 33(4): 187–

210.

Balassa, Bela. 1965. “Tariff Protection in Industrial Countries.” Journal of Political Econ-

omy, 73(6): 573–94.

Blanchard, Emily J., Chad P. Bown, and Davin Chor. 2019. “Did Trump’s Trade

War Impact the 2018 Election?” National Bureau of Economic Research Working Paper

26434.

Bown, Chad P., and Melina Kolb. 2019. “Trump’s Trade War Timeline: An Up-to-Date

Guide.” Peterson Institute for International Economics.

Bown, Chad P., Euijin Jung, and Zhiyao Lu. 2019a. “China’s Retaliation to Trump’s

Tariffs.” Peterson Institute for International Economics.

Bown, Chad P., Euijin Jung, and Zhiyao Lu. 2019b. “Trump, China, and Tariffs: From

Soybeans to Semiconductors.” Peterson Institute for International Economics.

Caldara, Dario, Matteo Iacoviello, Patrick Molligo, Andrea Prestipino, and An-

drea Raffo. 2019. “The Economic Effects of Trade Policy Uncertainty.” Journal of Mon-

etary Economics.

Cavallo, Alberto, Gita Gopinath, Brent Neiman, and Jenny Tang. 2019. “Tariff

Passthrough at the Border and at the Store: Evidence from U.S. Trade Policy.” Becker-

Friedman Institute Working Paper 2019-124.

Corden, W.M. 1966. “The Structure of a Tariff System and the Effective Protective Rate.”

Journal of Political Economy, 74(3): 221–237.

Fajgelbaum, Pablo D., Pinelopi K. Goldberg, Patrick J. Kennedy, and Amit K.

Khandelwal. 2019. “The Return to Protectionism.” National Bureau of Economic Re-

search Working Paper 25638.

Finkelstein, Amy. 2007. “The Aggregate Effects of Health Insurance: Evidence from the

Introduction of Medicare.” Quarterly Journal of Economics, 122(1): 1–37.

Flaaen, Aaron, Ali Horta¸csu, and Felix Tintelnot. 2019. “The Production Relocation

and Price Effects of U.S. Trade Policy: The Case of Washing Machines.” National Bureau

of Economic Research Working Paper 25767.

22

Handley, Kyle, Fariha Kamal, and Ryan Monarch. 2019. “Rising Import Tariffs,

Falling Export Growth: When Modern Supply Chains Meet Old-Style Protectionism.”

Working Paper.

Huang, Yi, Chen Lin, Sibo Liu, and Heiwei Tang. 2019. “Trade Networks and Firm

Value: Evidence from the U.S.-China Trade War.” Centre for Economic Policy Research

Working Paper DP14173.

Johnson, Harry G. 1953. “Optimum Tariffs and Retaliation.” The Review of Economic

Studies, 21(2): 142–53.

Kaldor, N. 1940. “A Note on Tariffs and the Terms of Trade.” Economica, 7(28): 377–80.

Pierce, Justin, and Peter Schott. 2012. “A Concordance Between U.S. Harmonized

System Codes and SIC/NAICS Product Classes and Industries.” Journal of Economic

and Social Measurement, 37(1-2): 61–96.

Reyes-Heroles, Ricardo, Sharon Traiberman, and Eva Van Leemput. 2019.

“Emerging Markets and the New Geography of Trade: The Effects of Rising Trade Barri-

ers.” Working Paper Working Paper.

Waugh, Michael E. 2019. “The Consumption Response to Trade Shocks: Evidence from

the US-China Trade War.” National Bureau of Economic Research Working Paper 26353.

23

A Expanded Detail on Implemented Tariffs

Tables A1 and A2 provide additional information regarding the data on products covered by

tariffs. Specifically, the tables report the value of trade–based on 2017 annual data from the

U.S. Census Bureau–that we calculate was subject to new tariffs, along with comparisons to

values of trade publicly announced by governments and those calculated by other researchers.

In addition, we provide links to sources of the lists of HS codes covered by new tariffs.

Table A1: New U.S. Import Tariffs by Trade Action and Wave

2017 Reported

Reference Import by Other Source

for Affected Volume Government Estimates for Other

Import Tariff Products Billions of U.S. Dollars Estimates

Sec. 201: Solar Panels 7 8.5

Sec. 201: Washing Machines 1.85 1.8

Sec. 232: Steel Link 27.7 10.2 29 Source

Sec. 232: Aluminum Link 17.4 7.7 17 Source

Sec. 301 Part 1 Link 32.3 34

Sec. 301 Part 2 Link 13.7 16

Sec. 301 Part 1+2 46.0 50 45.7 Source

Section 301 Part 3 Link 189 200 177 Source

Table A2: New Retaliatory Tariffs on U.S. Exports by Trade Action and Wave

2017 Reported

Reference Export by Other Source

for Affected Volume Government Estimates for Other

Retaliatory Tariff Products Billions of U.S. Dollars Estimates

China on US – Apr. 2018 Link 2.44 2.4 2.39 Source

EU on US – Jun. 2018 Link 4.23 3.2 3.24 Source

Canada on US – Jul. 2018 Link 17.8 12.8 12.76 Source

China on US – Jul. 2018 Link 29.2 34

China on US – Aug. 2018 Link 21.9 16

China on US – Jul.+Aug. 51.1 50 49.8 Source

China on US – Sep. 2018 Link 52 60 53.4 Source

Mexico on US – Jun. 2018 Link 4.51 3.8

India on US – Jan. 2019 Link 0.89 1.3 1.3 Source

Turkey on US – Jun. 2018 Link 1.56 1.8

Russia on US – Aug. 2018 Link 0.27 0.43

China on US – Sep. 2019 Link 112

China on US – Dec. 2019 Link 160

24

B Additional Results

Figure B1 breaks down Figure 2 in the main text based on major classifications on the types

of goods subject to new U.S. import tariffs. As indicated in the figure, the tariffs imposed

by the U.S. in 2018 were targeted mostly against intermediate goods (shown in blue) and

capital goods (red), which are inputs to production for U.S.-located manufacturers. Later

rounds of tariffs imposed in 2019, which fall outside of our period of analysis and are shown

by light shading, were focused relatively more on consumer goods.

Figure B1: Composition of New U.S. Import Tariffs: 2018-2019

Solar Panels,

Wash. Mach.

Sec.201: $7B

Steel, Aluminum

Sec. 232: $40B

Chinese Imports

Sec. 301: $506B

0 200 400 600

Billions of USD (Based on 2017 Imports)

2018m1 2018m7 2019m1 2019m7 2020m1

Consumer Goods

Capital Goods

Intermediate Goods

Source: U.S. International Trade Commission for 2017 Import Values. See Table A1 for details on the set of

relevant products and trade values. Classification comes from the Broad Economic Categories (BEC) from

the United Nations. Further details can be found here. Lightly shaded areas are used for tariffs imposed in

late 2019, which fall outside the main period of analysis for this paper.

We also report coefficient estimates for the control variables used in equation (7). These

variables—industry export share of output and industry import share of domestic absorption—

are intended to capture any features of industry exposure to things like exchange rate move-

ments or overall foreign growth; these effects may also capture some of the potential impact

from increased uncertainty on international markets more generally. Figure B2 reports these

results pertaining to employment, industrial production, and PPIs.

25

Figure B2: Coefficient Estimates from General International Conditions

(a) Employment

-.06-.04-.020.02.04

90% CI

2017m1 2018m1 2019m1 2020m1

Import Share of Consumption

-.05 0 .05 .1 .15

90% CI

2017m1 2018m1 2019m1 2020m1

Export Share of Shipments

(b) Industrial Production (Output)

-.2 0 .2 .4

90% CI

2017m1 2018m1 2019m1 2020m1

Import Share of Consumption

-.3 -.2 -.1 0 .1 .2

90% CI

2017m1 2018m1 2019m1 2020m1

Export Share of Shipments

(c) Producer Price Index

-.1 0 .1 .2 .3

90% CI

2017m1 2018m1 2019m1 2020m1

Import Share of Consumption

-.3 -.2 -.1 0 .1

90% CI

2017m1 2018m1 2019m1 2020m1

Export Share of Shipments

Sources: Federal Reserve Board (FRB), U.S. Department of Labor, Bureau of Labor Statistics; authors’

calculations.

Notes: Each panel represents results from separate regressions, where we plot the coefficient estimates of

ω

t

and ϕ

t

from the detrended version of equation (7). The shaded areas represent 90 percent confidence

intervals, and the two dashed lines represent February 2018 and September 2018, the first and last wave of

new 2018 tariffs.

B.1 Alternative Specifications

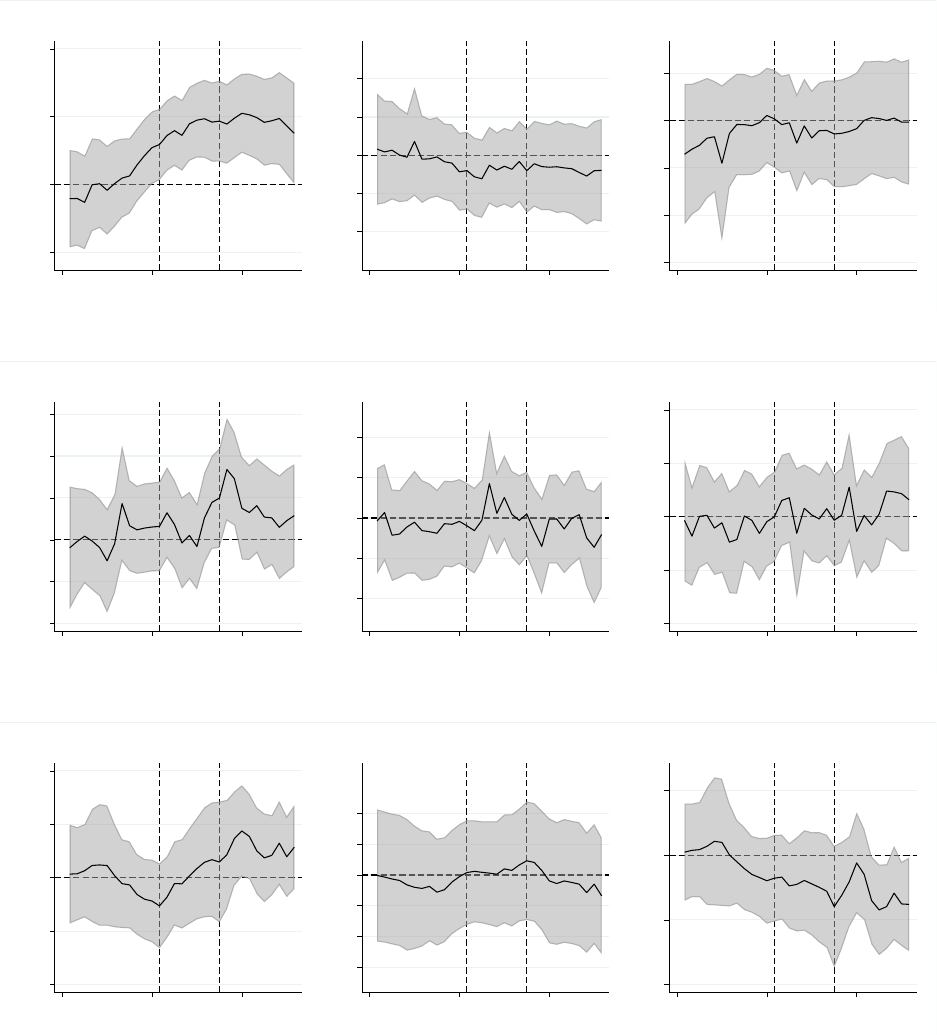

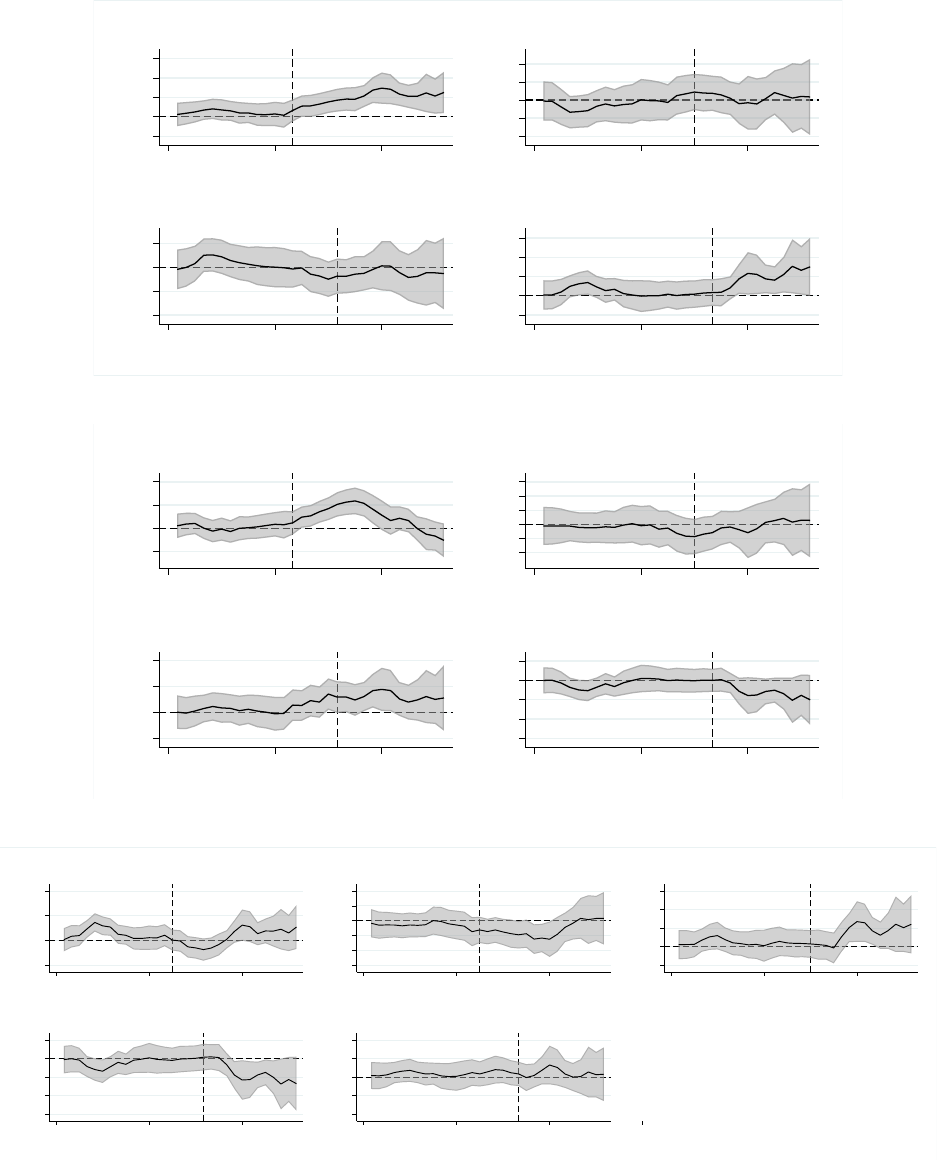

Figure B3 presents the results from estimating equation (7) without first removing an

industry-specific trend from each dependent variable. As indicated in the figure, there is

26

evidence that some industries were on different pre-trends in terms of the outcome variables

prior to the imposition of tariffs. For example, the estimates for employment, shown in Panel

a of Figure B3 appear to be on upward trends with respect to rising input costs and foreign

retaliation and a downward trend for import protection.

As discussed in the main text, we control for these differing pre-trends by either detrend-

ing the dependent variable based on its 2017 linear trend or subtracting out the pre-trend

following the approach in Finkelstein (2007). Our approach, therefore, treats these time

trends as resulting from independent random shocks that affect outcomes in each industry

over the short term, rather than long-term trends associated with particular industry char-

acteristics. This assumption seems reasonable given our use of high-frequency data focusing

on a relatively short period of time. It is also supported by our finding, shown in Figure

B3 that the pre-trends often move in different directions for different tariff channels, even

though measures of each of the tariff channel exposure variables are positively correlated

with one another.

B.2 Univariate Results

Figure B4 presents results of regressions of the three outcome variables on individual tariff

channel measures, one at a time, as opposed to including the three channels together in the

same regression. Thus, Figure B4 shows the results of nine separate regressions, rather than

three separate regressions as in Figure 4 in the main text.

There are some similarities between these “univariate” regression results and the main

results shown in Figure 4. Figure B4 still finds negative relationships between employment

and both the rising input cost and foreign retaliation channels. There are also important

differences, however. While the middle column of Panel C in Figure B4 finds a positive

relationship between the effects of import protection and producer prices, the equivalent

panel in Figure 4 reveals that this result is not present once the measure for rising input

costs is included in the regression.

B.3 Results by Tariff Wave

The main results presented in Figure 4 calculate exposure to three tariff channels based

on cumulative values of affected trade, covering all tariffs imposed over the course of 2018.

Figures B5, B6, and B7, on the other hand, show the results of regressions that include

separate measures for each of the individual waves of tariffs. Therefore, Figures B5, B6,

and B7 each show the results of a single regression. The vertical lines in each of the figures

represent the time that each individual tariff wave took effect.

These figures yield several findings on the effects of each individual tariff wave. First,

27

Figure B3: Effects of Cumulative Tariffs (Non-Detrended)

(a) Employment

-.5 0 .5 1

90% CI

2017m1 2018m1 2019m1 2020m1

Rising Input Costs

-.2 -.1 0 .1 .2

90% CI

2017m1 2018m1 2019m1 2020m1

Import Protection

-1.5 -1 -.5 0 .5

90% CI

2017m1 2018m1 2019m1 2020m1

Foreign Retaliation

(b) Industrial Production (Output)

-1 -.5 0 .5 1 1.5

90% CI

2017m1 2018m1 2019m1 2020m1

Rising Input Costs

-.4 -.2 0 .2 .4

90% CI

2017m1 2018m1 2019m1 2020m1

Import Protection

-2 -1 0 1 2

90% CI

2017m1 2018m1 2019m1 2020m1

Foreign Retaliation

(c) Producer Price Index

-2 -1 0 1 2

90% CI

2017m1 2018m1 2019m1 2020m1

Rising Input Costs

-.3 -.2 -.1 0 .1 .2

90% CI

2017m1 2018m1 2019m1 2020m1

Import Protection

-2 -1 0 1

90% CI

2017m1 2018m1 2019m1 2020m1

Foreign Retaliation

Sources: Federal Reserve Board (FRB), U.S. Department of Labor, Bureau of Labor Statistics; authors’

calculations.

Notes: Each panel represents separate regressions, with each column of the panel corresponding to the first

three components of equation (7). The shaded areas represent 90 percent confidence intervals, and the two

dashed lines represent February 2018 and September 2018, the first and last wave of new 2018 tariffs.

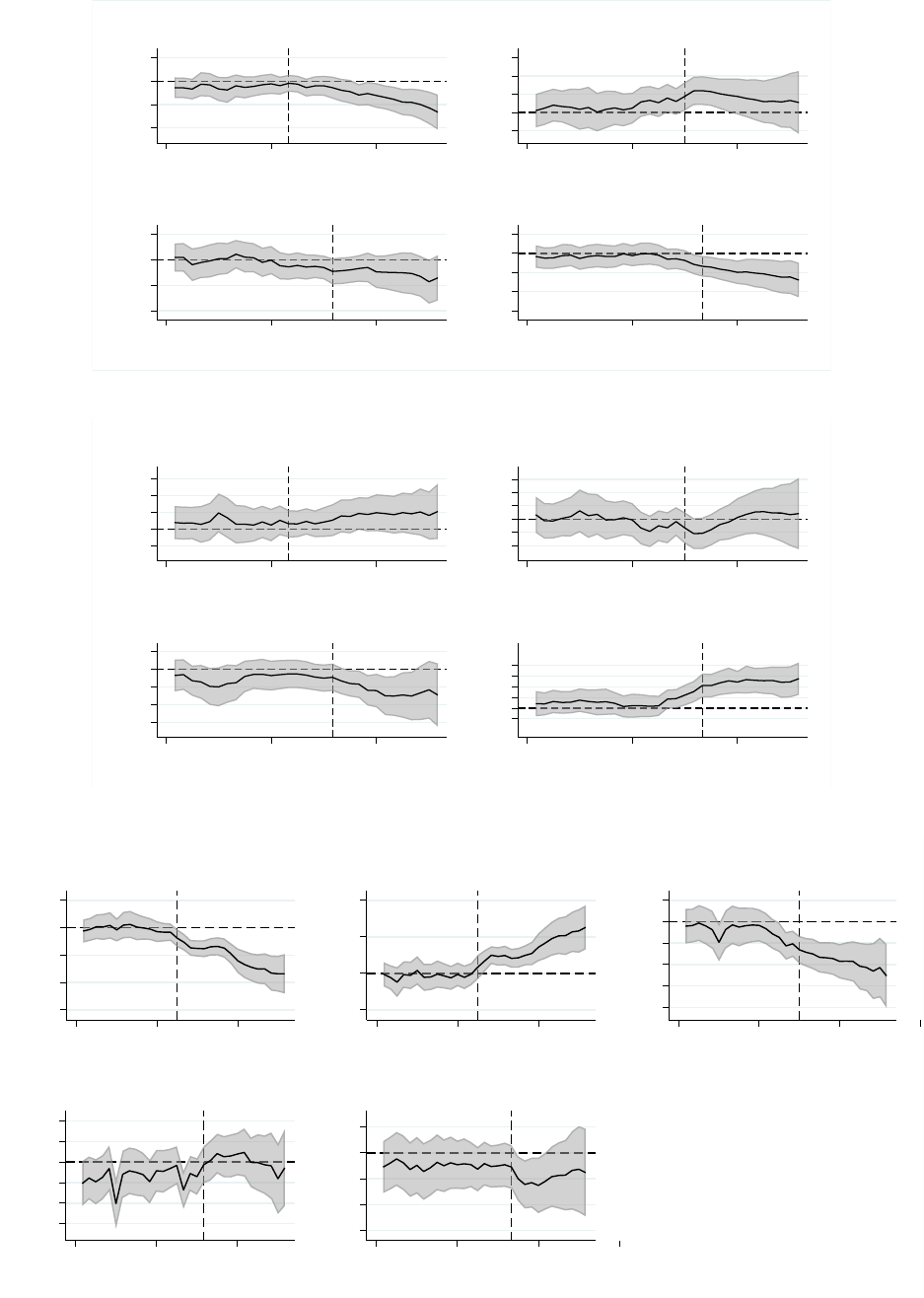

we typically find the most pronounced relationships with outcome variables coming from

the March (steel and aluminum) and September (largest China 301 wave) waves of U.S.

tariffs. This is apparent, for example, in the effects of the rising input cost tariff waves on

employment (Panel a of Figure B5) and producer prices (Panel a of Figure B7). Second, we

28

Figure B4: Univariate Effects of Cumulative Tariffs (Detrended)

(a) Employment

-.8 -.6 -.4 -.2 0 .2

90% CI

2017m1 2018m1 2019m1 2020m1

Rising Input Costs

-.1 -.05 0 .05 .1

90% CI

2017m1 2018m1 2019m1 2020m1

Import Protection

-1.5 -1 -.5 0 .5

90% CI

2017m1 2018m1 2019m1 2020m1

Foreign Retaliation

(b) Industrial Production (Output)

-1 -.5 0 .5 1

90% CI

2017m1 2018m1 2019m1 2020m1

Rising Input Costs

-.4 -.2 0 .2 .4

90% CI

2017m1 2018m1 2019m1 2020m1

Import Protection

-2 -1 0 1 2 3

90% CI

2017m1 2018m1 2019m1 2020m1

Foreign Retaliation

(c) Producer Price Index

-1 0 1 2 3 4

90% CI

2017m1 2018m1 2019m1 2020m1

Rising Input Costs

-.2 0 .2 .4 .6 .8

90% CI

2017m1 2018m1 2019m1 2020m1

Import Protection

-1 0 1 2 3

90% CI

2017m1 2018m1 2019m1 2020m1

Foreign Retaliation

Sources: Federal Reserve Board (FRB), U.S. Department of Labor, Bureau of Labor Statistics; authors’

calculations.

Notes: Each chart represents separate regressions, with only the particular channel present. The shaded areas

represent 90 percent confidence intervals, and the two dashed lines represent February 2018 and September

2018, the first and last wave of new 2018 tariffs.

find that producer prices respond quickly to tariffs. Panel a of Figure B7 shows producer

prices rising immediately in response to the March and September rounds of tariffs.

29

Figure B5: Employment Effects by Tariff Wave (Detrended)

(a) Rising Input Costs

-1 -.5 0 .5

90% CI

2017m1 2018m1 2019m1 2020m1

Rising Input Costs (Mar.)

-5 0 5 1015

90% CI

2017m1 2018m1 2019m1 2020m1

Rising Input Costs (Jul.)

-20 -10 0 10

90% CI

2017m1 2018m1 2019m1 2020m1

Rising Input Costs (Aug.)

-6 -4 -2 0 2

90% CI

2017m1 2018m1 2019m1 2020m1

Rising Input Costs (Sep.)

(b) Import Protection

-.2 0 .2 .4 .6

90% CI

2017m1 2018m1 2019m1 2020m1

Import Protection (Mar.)

-1-.50 .5 11.5

90% CI

2017m1 2018m1 2019m1 2020m1

Import Protection (Jul.)

-3 -2 -1 0 1

90% CI

2017m1 2018m1 2019m1 2020m1

Import Protection (Aug.)

-.10.1.2.3.4

90% CI

2017m1 2018m1 2019m1 2020m1

Import Protection (Sep.)

(c) Foreign Retaliation

-60-40-20 0 20

90% CI

2017m1 2018m1 2019m1 2020m1

Foreign Retaliation (Apr.)

-5 0 5 10

90% CI

2017m1 2018m1 2019m1 2020m1

Foreign Retaliation (Jun.)

-4 -3 -2 -1 0 1

90% CI

2017m1 2018m1 2019m1 2020m1

Foreign Retaliation (Jul.)

-3 -2 -1 0 1 2

90% CI

2017m1 2018m1 2019m1 2020m1

Foreign Retaliation (Aug.)

-1.5 -1 -.5 0 .5

90% CI

2017m1 2018m1 2019m1 2020m1

Foreign Retaliation (Sep.)

Sources: U.S. Department of Labor, Bureau of Labor Statistics; authors’ calculations.

Notes: The shaded areas represent 90 percent confidence intervals.

30

Figure B6: I.P. Effects by Tariff Wave (Detrended)

(a) Rising Input Costs

-1.5-1-.50 .5 1

90% CI

2017m1 2018m1 2019m1 2020m1

Rising Input Costs (Mar.)

-20 0 20 40

90% CI

2017m1 2018m1 2019m1 2020m1

Rising Input Costs (Jul.)

-40-20 0 2040

90% CI

2017m1 2018m1 2019m1 2020m1

Rising Input Costs (Aug.)

-20 -10 0 10

90% CI

2017m1 2018m1 2019m1 2020m1

Rising Input Costs (Sep.)

(b) Import Protection

-.5 0 .5 1 1.5

90% CI

2017m1 2018m1 2019m1 2020m1

Import Protection (Mar.)

-10 -5 0 5

90% CI

2017m1 2018m1 2019m1 2020m1

Import Protection (Jul.)

-5 0 5 10

90% CI

2017m1 2018m1 2019m1 2020m1

Import Protection (Aug.)

-1 -.5 0 .5 1

90% CI

2017m1 2018m1 2019m1 2020m1

Import Protection (Sep.)

(c) Foreign Retaliation

-40-20 0 20 40

90% CI

2017m1 2018m1 2019m1 2020m1

Foreign Retaliation (Apr.)

-5 0 5

90% CI

2017m1 2018m1 2019m1 2020m1

Foreign Retaliation (Jun.)

-6 -4 -2 0 2 4

90% CI

2017m1 2018m1 2019m1 2020m1

Foreign Retaliation (Jul.)

-10 0 10 20

90% CI

2017m1 2018m1 2019m1 2020m1

Foreign Retaliation (Aug.)

-2 -1 0 1 2 3

90% CI

2017m1 2018m1 2019m1 2020m1

Foreign Retaliation (Sep.)

Sources: Federal Reserve Board; authors’ calculations.

Notes: The shaded areas represent 90 percent confidence intervals.

31

Figure B7: P.P.I. Effects by Tariff Wave (Detrended)

(a) Rising Input Costs

-1 0 1 2 3

90% CI

2017m1 2018m1 2019m1 2020m1

Rising Input Costs (Mar.)

-10-5 0 5 10

90% CI

2017m1 2018m1 2019m1 2020m1

Rising Input Costs (Jul.)

-20-10 0 10

90% CI

2017m1 2018m1 2019m1 2020m1

Rising Input Costs (Aug.)

-5 0 5 1015

90% CI

2017m1 2018m1 2019m1 2020m1

Rising Input Costs (Sep.)

(b) Import Protection

-1 0 1 2

90% CI

2017m1 2018m1 2019m1 2020m1

Import Protection (Mar.)

-2-10 1 2 3

90% CI

2017m1 2018m1 2019m1 2020m1

Import Protection (Jul.)

-2 0 2 4

90% CI

2017m1 2018m1 2019m1 2020m1

Import Protection (Aug.)

-1.5-1 -.5 0 .5

90% CI

2017m1 2018m1 2019m1 2020m1

Import Protection (Sep.)

(c) Foreign Retaliation

-50 0 50 100

90% CI

2017m1 2018m1 2019m1 2020m1

Foreign Retaliation (Apr.)

-6 -4 -2 0 2 4

90% CI

2017m1 2018m1 2019m1 2020m1

Foreign Retaliation (Jun.)

-2 0 2 4 6

90% CI

2017m1 2018m1 2019m1 2020m1

Foreign Retaliation (Jul.)

-15-10 -5 0 5

90% CI

2017m1 2018m1 2019m1 2020m1

Foreign Retaliation (Aug.)

-4 -2 0 2 4

90% CI

2017m1 2018m1 2019m1 2020m1

Foreign Retaliation (Sep.)

Sources: U.S. Department of Labor, Bureau of Labor Statistics ; authors’ calculations.

Notes: The shaded areas represent 90 percent confidence intervals.

32