REPORT OF THE

ELECTRONICS INSURANCE NOTICES AND

DOCUMENTS WORKING GROUP

Pursuant to S.C.R. No. 159, S.D. 1 (2013)

REQUESTING THE INSURANCE COMMISSIONER TO CONVENE A

WORKING GROUP TO EXPLORE THE USE OF ELECTRONIC

TRANSMISSION OF INSURANCE NOTICES AND DOCUMENTS

Prepared by the

INSURANCE DIVISION

DEPARTMENT OF COMMERCE AND CONSUMER AFFAIRS

STATE OF HAWAII

December 2013

ii

TABLE OF CONTENTS

Introduction……………………………………………………………………………. 1

Discussion…………………………………………………………………………….. .2

I. Model Law……………………………………………………………….. 2

A. Electronic Delivery of Insurance Documents………………… 3

B. Electronic Posting………………………………………………. 4

II. Use of Electronic Insurance Notices and Documents in Other

States…………………………………………………………………….. 5

III. Electronic Posting in Other States……………………………………. 5

IV. Industry Interests……………………………………………………….. 6

V. Consumer Interests and Concerns…………………………………… 6

VI. Uniform Electronic Transactions Act………………………………..... 8

Findings and Recommendations…………………………………………………..10

Appendices

A. Senate Concurrent Resolution No. 159, S.D. 1, Twenty-seventh

Legislature, 2013…………………………………………………...................14

B. Model Merged Insurance Transaction Modernization Electronic

Delivery or Posting……………………………………………………………..16

C. Property Casualty Insurers Association of America e-posting/

e-delivery - Laws & Regulations Reference Chart………………………….21

ELECTRONIC INSURANCE NOTICES AND DOCUMENTS

WORKING GROUP REPORT

INTRODUCTION

Senate Concurrent Resolution No. 159, S.D. 1 (2013) (“SCR 159”) requested the

Insurance Commissioner to do the following:

(1) Convene a working group to explore the use of electronic transmission of

insurance notices and documents; and

(2) Develop alternatives for insurance notices and documents that balance the

convenience of electronic notices and documents with consumer protection.

A copy of the resolution is attached as Appendix A.

SCR 159 specified that the Working Group be composed of the Insurance

Commissioner and representatives from the following: Commission to Promote Uniform

Legislation (“Hawaii Commission”); Property Casualty Insurers Association of America

(“PCI”); Hawaii Insurers Council (“HIC”); and State Farm Insurance Company (“State

Farm”).

The Working Group consisted of the following: Gordon Ito, Insurance

Commissioner; Alex Hageli, PCI; Isaac Kosasa, HIC; Lori C. Lum, Watanabe Ing LLC

representing PCI; Robert R. Nash, State Farm; Alison Powers, HIC; Mark Sektnan, PCI;

and Bob Toyofuku, Hawaii Commission.

Additional participants in the Working Group were: Martha Im, Insurance

Division; Robert Joslin, Hawaii Public Adjusters; David Leifer, American Council of Life

Insurers (“ACLI”); Ann Le Lievre, Insurance Division; Joann Waiters, ACLI; and Tiffany

Yajima, Ashford & Wriston, LLLP.

1

SCR 159 requested that the Legislative Reference Bureau submit a final report of

the Working Group’s findings and recommendations, including any proposed legislation,

to the Legislature no later than 20 days prior to the convening of the Regular Session of

2014.

The Working Group met over the course of August 2013 through November

2013. Minutes from each meeting, with accompanying exhibits discussed during the

meetings, are posted on the Department of Commerce and Consumer Affairs,

Insurance Division website at: http://hawaii.gov/dcca/ins/.

DISCUSSION

I. Model Law

The Working Group reviewed and discussed a model law drafted by the

insurance industry, the Model Merged Insurance Transaction Modernization Electronic

Delivery or Posting (“Model Law”), which allows for both electronic delivery of insurance

documents and notices, as well as for electronic posting of property and casualty

insurance documents that contain no personally identifiable information

1

. Although the

Model Law has not been adopted by a majority of the states, it has been adopted, in

whole or in part, by some states within the past two (2) years with the support of the

insurance industry. See Appendix B.

The Model Law has two (2) components. The first part allows for electronic

delivery of all insurance notices and documents, provided the consumer affirmatively

consents, or opts-in, to receiving specific notices or documents electronically. The

1

The first iteration of part 1 of the Model Law began circulating in approximately 2009, while part 2 of the

Model Law began circulating in approximately 2011. In late 2012, the two (2) parts were joined to form

the Model Law, the most recent iteration of which is dated March 2013.

2

second part of the Model Law allows for electronic posting on a website of standard

policy forms and endorsements that contain no personally identifiable information,

provided that the consumer does not specifically request, or opts-out, to receiving those

documents in paper form.

A. Electronic Delivery of Insurance Documents

Part 1 of the Model Law, entitled “Electronic Notices and Documents”, allows for

delivery of insurance documents to a recipient’s electronic mail address or posting of

the same on an electronic network or site accessible via the internet, together with

separate notice of the posting to a recipient’s electronic mail address, provided the

recipient affirmatively consents, or opts-in, to receive the documents by electronic

means. Part 1 is intended to apply to all insurance notices and documents, including

those that contain personally identifiable information.

In addition, the recipient must be provided a statement regarding the right to

receive a paper copy of the documents. The statement must include language

regarding the right to withdraw such consent, whether the consent applies to a single

transaction or categories of documents, the means to obtain a paper copy and any

associated fees for paper copies, and the procedure to withdraw consent. There must

also be information provided regarding hardware and software requirements, and any

updates to such, to access electronic documents. Other provisions in part 1 of the

Model Law address the validity of the transaction if consents or acknowledgment of

receipt of notices or documents are not verified, effect of prior transactions in the event

consent to electronic delivery is revoked, electronic storage of oral consents, and

3

acknowledgment of the federal Electronic Signatures in Global and National Commerce

Act (“E-SIGN”), Public Law 106-229, codified at 15 USC § 7001 et seq.

B. Electronic Posting

Part 2 of the Model Law, entitled “Posting of Policies on the Internet”, allows for

electronic posting of property and casualty insurance notices and documents on a

website, usually the insurers’ website, for retrieval by the policyholder. Documents that

would be posted electronically are restricted to those that do not contain personally

identifiable information, such as the standard policy form and standard endorsement.

The insurer would post these documents on their website unless the policy holder

specifically declines to receive an electronic copy, or opts-out, and will then receive a

paper copy.

Certain conditions must be in place for electronic posting to occur, including that

the policy and endorsements: 1) must be accessible for as long as the policy is in force;

2) are archived for five (5) years after expiration; and 3) are posted in a manner that

allows the insured to retrieve and print using software widely available on the internet

and free to use. Further, the insurer is to provide certain information with the

declarations page and any renewals, including the exact policy and endorsement forms

purchased, the method by which the insured may obtain without charge a paper copy of

the policy, and the internet address where the policy and endorsements are posted.

Lastly, the insurer must provide notice in the format preferred by the policy holder, of

any changes to the forms or endorsements, the right to obtain a paper copy of

documents, and the internet address where the forms are posted.

4

II. Use of Electronic Insurance Notices and Documents in Other States

Generally speaking, an insurance document may be delivered electronically

unless: (1) it is expressly prohibited, as enumerated in Hawaii’s Uniform Electronic

Transactions Act (“UETA”), Hawaii Revised Statutes (“HRS”) §489E-3(b)(3)(C); or (2) a

law requires a specific document to be delivered via first class mail. The Working

Group gathered information about use of electronic insurance notices and documents in

other states. Eleven (11) states

2

have enacted insurance code provisions that allow for

electronic delivery of policies and endorsements and an additional three (3) states

3

have issued bulletins which have interpreted electronic mail to equate with physical mail

under the respective states’ insurance code sections. See Appendix C.

III. Electronic Posting in Other States

Currently, twelve (12) states allow for electronic posting, or e-posting, of

insurance documents.

4

Of the twelve (12) states, eight (8) states

5

restrict e-posting to

property and casualty policies or endorsements, three (3) states

6

are silent as to the

lines of insurance qualifying for e-posting, and one (1) state

7

restricts e-posting to

automobile policies.

2

Delaware, Florida (for commercial lines policy only, must opt-out), Idaho, Kansas, Maryland, Minnesota,

Missouri, North Carolina, Pennsylvania, Texas, and Virginia.

3

Arkansas, Kentucky, and Tennessee.

4

Alaska, Arizona, Florida, Illinois, Kansas, Michigan, Minnesota, Missouri, Oklahoma, Pennsylvania,

Texas, and Virginia.

5

Alaska, Arizona, Florida, Minnesota, Missouri, Oklahoma, Texas (also includes automobile policies for

e-posting), and Virginia.

6

Illinois, Kansas, and Pennsylvania.

7

Michigan.

5

IV. Industry Interests

The industry supports parts 1 and 2 of the Model Law. Insurers are in favor of

allowing electronic delivery of all documents, including those that contain personally

identifiable information, if the consumer affirmatively opts-in to receive such notices and

documents electronically. In addition, insurers support e-posting of standard policies

and endorsements that contain no personally identifiable information where policy

holders must opt-out to receive a paper copy of those documents. Other than the

exemptions under E-SIGN regarding electronic notices of cancellations for life insurance

benefits (except for annuities) and health insurance and benefits, industry

representatives were in favor of electronic notices and documents for all lines of

insurance.

Industry representatives stated that consumers are increasingly requesting

electronic documents, especially younger consumers who are technology savvy and

prefer electronic transactions. Electronic documents allow for cost savings for the

insurer for printing and mailing, which are then passed on to the consumer, as well as

environmental savings in fossil fuel and paper waste. The electronic format allows for

documents to be readily available and accessible from the internet, and in a searchable

format.

V. Consumer Interests and Concerns

While there were no named representatives in the Working Group representing

formal consumer advocate organizations or interests, comments shared during Working

Group meetings did not, in general, indicate strong opposition to part 1 of the Model

Law, allowing electronic notices and documents to be transmitted electronically when

6

the consumer opts-in to receive those documents electronically. However, the Hawaii

Commission strongly opposed any electronic cancellation, termination, lapse, or

material alteration of a contract of insurance, insurance benefits, life settlement or

viatical settlement agreements, or service contract. Additionally, the Hawaii

Commission and public comments indicated concerns regarding the language in part 2

of the Model Law that allows insurers to post standard policies and endorsements on

the internet unless the consumer opts-out to receive those documents in paper form. In

particular, the concern was that many consumers would find it confusing to opt-in for

one set of documents, and opt-out for another category of documents.

Hawaii’s consumers include the elderly and many immigrants for whom English

is a second language; either or both groups may not be technology savvy. In addition,

rural areas in Hawaii have limited cell phone or internet access. Having standard

policies and endorsements automatically posted on the internet may hamper

consumers’ access to electronically posted documents. Consumers may not

understand that the standard policy form is available on the internet and that they would

need to opt-out to request a paper copy. Other concerns included consumers who

would not understand that the declarations page was not the policy, which would be a

separate document available through the insurer’s website. There was also concern

that changes to standard policy forms and endorsements may be transmitted

electronically but not received due to an inaccurate email address or filtered out as

spam, resulting in consumers being unaware of such changes even if the consumer

opted-in to receive e-documents.

7

Additionally, fees for paper copies of notices and documents were discussed.

One concern voiced regarding part 1 of the Model Law addressed discounts for

consumers who opt-in to receive electronic notices and documents, then later change

their mind and request paper copies. Any charges for paper copies should be equitable

in relation to the discount for opting-in for electronic documents. For part 2 of the Model

Law, while some industry representatives in the Working Group stated they would not

impose any fees for consumers who opt-out to receive a paper copy of standard policy

forms and endorsements, there are some insurers who do charge for paper copies of

the standard policy forms and endorsements. Working Group industry representatives

also stated they may later reassess if a fee would be imposed for continuing to receive

paper copies of standard policies and endorsements.

Finally, the Working Group was cognizant that electronic delivery of notices and

documents must be compliant with the Americans with Disabilities Act and other state

disability laws.

VI. Uniform Electronic Transactions Act

The UETA was developed in 1999 by the National Conference of Commissioners

on Uniform State Laws to enable use of electronic records and signatures relating to a

transaction between two (2) or more individuals in the conduct of business, commercial,

or governmental affairs. UETA was meant to allow for electronic records and electronic

signatures to have the same legally binding effect as paper records and manual

signatures, provided that the two (2) parties agree to those terms.

8

Forty-seven (47) states, including Hawaii, have adopted UETA. The three (3)

states

8

which have not adopted UETA have enacted statutes that essentially allow for

use of electronic transactions. Hawaii’s UETA statute, codified at HRS Chapter 489E,

allows for and recognizes electronic records and signatures. However, there is a

specific exclusion for certain types of insurance documents. HRS § 489E-3(b)(3)(C)

states in part as follows:

(b) This chapter does not apply to a transaction to the extent it is

governed by: . . .

(3) A law or rule governing notice of: . . .

(C) Cancellation, termination, lapse, or material alteration of

a contract of insurance, insurance benefits, life settlement or

viatical settlement agreement, or service contract.

If the Legislature allows for electronic delivery of notices of cancellation, termination,

lapse, or material alteration of a contract of insurance, insurance benefits, life settlement

or viatical settlement agreement, or service contract, then HRS § 489E-3(b)(3)(C) may

need to be amended, as well as a substantial number of provisions requiring written

notice in the Insurance Code. A partial listing of the affected provisions in the Insurance

Code is as follows:

Article 3A, Chapter 431

Notices related to the privacy of personal financial information

Article 10, Chapter 431

Disclosure of healthcare coverage

Application for insurance coverage

Execution of policies

Delivery of policies

Notice of cancellation or non-renewal

Assignment of polices

8

Illinois, New York, and Washington are the three (3) states which have not adopted UETA.

9

Article 10A, Chapter 431 Health Insurance

Cancellation non-renewal reinstatement of coverage

Notice of right to return the policy – free examination of policy

Article 10C, Chapter 431 Motor vehicle Insurance

Notice of replacement of insurance by a subsidiary or affiliate of insurer

Notice of cancellation or non-renewal

Disclosure of personal injury protection limits and payments

Article 10D, Chapter 431 Life Insurance and Annuities

Disclosure requirements of insurers and producers

Disclosure and reporting when replacing life insurance with a new policy

Article 10H, Chapter 431 Long Term Care Insurance

Disclosure of right to return policy free look at policy

Report of long term care benefits

Notice of unintentional lapse

Notice of lapse or termination for non-payment of premium

Standard format and outline of coverage

Chapter 431C, Life Settlements

Disclosures to Owners

If the Legislature allows electronic notices for cancellation, termination, lapse, or

material alteration of a contract of insurance, insurance benefits, life settlement or

viatical settlement agreement, or service contract notices, where the Insurance Code is

silent as of these types of documents, HRS § 489E-3 requires clarifying language to

specifically allow for this.

FINDINGS AND RECOMMENDATIONS

After much discussion and deliberation, the Working Group makes the following

findings and recommendations:

1. All Working Group representatives agree that a growing number of

consumers prefer communicating with insurers electronically rather than

10

through traditional means, including receiving documents, notices, and

policy forms.

2. There was no unanimous agreement as to recommendations on electronic

transmission of insurance notices and documents:

a. Industry Working Group representatives agree insurers that wish to

do so should be permitted, but not required, to offer their

policyholders the option to receive all insurance notices and

documents electronically. In addition, industry Working Group

representatives agree that insurers should be permitted, but not

required, to post standard forms and policies that contain no

personally identifiable information on insurers’ websites for

purposes of satisfying their legal obligation to deliver such

documents to their policyholders.

b. While the Hawaii Commission to Promote Uniform Legislation

(“Hawaii Commission”) recognizes the benefits of electronic

transmission of insurance notices and documents, the Hawaii

Commission supports insureds affirmatively consenting to receive

electronically certain insurance notices and documents, including

those that do not contain personally identifiable information.

However, the Hawaii Commission specifically opposes any

electronic notices and documents that are in direct contravention to

Hawaii’s UETA, HRS §489E-3(b)(3)(C), which specifically prohibits

electronic delivery of notices of cancellation, termination, lapse, or

11

material alteration of a contract of insurance, insurance benefits, life

settlement or viatical settlement agreement, or service contract.

c. The Insurance Commissioner recognizes the benefits of electronic

transmission of insurance notices and documents and supports

allowing consumers to choose to receive insurance notices and

documents. However, the Insurance Commissioner is opposed to

the automatic e-posting of documents and requiring the consumer

to opt-out or affirmatively choose to receive certain documents in

paper format. Additionally, the Insurance Commissioner is

concerned with any fees insurers may impose for paper copies of

documents.

3. There was no unanimous agreement on proposed legislation:

a. Industry representatives agree to adoption of both parts 1 and 2 of

the Model Merged Insurance Transaction Modernization Electronic

Delivery or Posting (“Model Law”).

b. The Hawaii Commission opposes any legislation allowing for

electronic delivery of notices of cancellation, termination, lapse, or

material alteration of a contract of insurance, insurance benefits, life

settlement or viatical settlement agreement, or service contract, in

direct contravention to Hawaii’s UETA, HRS §489E-3(b)(3)(C).

c. The Hawaii Commission and the Insurance Commissioner oppose

any proposed legislation allowing for automatic electronic posting of

12

13

documents or notices that would then require the consumer to

affirmatively request, or opt-in to receive, paper copies of the same.

4. The Legislature should consider language in the Model Law and

determine if industry and consumer interests may be accommodated by

allowing electronic transmission of insurance notices and documents.

5. The Legislature may need to consider whether rulemaking is necessary

before implementation of any statute allowing for electronic transmission

of insurance notices and documents, to provide appropriate guidance to

insurers and consumers.

APPENDIX A

THE SENATE

TWENTY-SEVENTH LEGISLATURE, 2013

STATE OF HAWAII

S.C.R. NO.

SENATE CONCURRENT

RESOLUTION

159

S.0.1

REQUESTING

THE

INSURANCE

COMMISSIONER

TO

CONVENE

A

WORKING

GROUP

TO

EXPLORE

THE

USE

OF

ELECTRONIC TRANSMISSION

OF

INSURANCE

NOTICES

AND

DOCUMENTS.

1

WHEREAS,

Hawaii

has

adopted

the

model

Uniform

Electronic

2

Transactions

Act,

codified

as

chapter

489E,

Hawaii

Revised

3

Statutes;

and

4

5

WHEREAS,

chapter

489E,

Hawaii

Revised

Statutes,

excludes

6

insurance

documents

and

notices

from

its

purview;

and

7

8

WHEREAS,

insurance

notices

and

documents

are

currently

9

required

to

be

in

writing;

and

10

11

WHEREAS,

although

consumers

have

indicated

a

preference

to

12

obtain

notices

and

documents

by

electronic

means,

there

are

13

certain

questions

as

to

the

appropriate

use

and

application

of

14

electronic

notices

and

documents;

and

15

16

WHEREAS,

the

insurance

industry,

like

other

industries,

is

17

engaged

in

more

online

and

internet-based

sales

and

18

notifications;

and

19

20

WHEREAS,

because

the

insurance

mark.etplace

is

in

the

21

process

of

this

change,

the

State

is

interested

in

exploring

the

22

appropriate

balance

between

consumer

convenience

and

consumer

23

protection;

and

24

2S

WHEREAS,

potential

issues

related

to

the

use

of

electronic

26

transmission

of

insurance

notices

and

documents

should

be

27

explored;

now,

therefore,

28

29

BE

IT

RESOLVED

by

the

Senate

of

the

Twenty-seventh

30

Legislature

of

the

State

of

Hawaii,

Regular

Session

of

2013,

the

31

House

of

Representatives

concurring,

that

the

Insurance

32

Commissioner

is

requested

to

convene

a

working

group

to

explore

2013-2101

SCR159 SD1

SMA.

doc

IIIIIII

~IIIIIIIIIIIIII~IIII~IIIIIII~IIIIII~~II!IIIIIIIII~~II

~IIIIIIIIIII~IIIIIIIIIIIII!IIIIIIIIIII~IIIIIIIII

14

Page 2

S.C.R. NO.

1

the

use

of

electronic

transmission

of

insurance

notices

and

2

documents;

and

3

159

S.D. 1

4

BE

IT

FURTHER

RESOLVED

that

the

working

group

be

composed

5

of

the

Insurance

Commissioner

and

representatives

from

the

6

Commission

to

Promote

Uniform

Legislation,

Property

Casualty

7

Insurers

Association

of

America,

Hawaii

Insurers

Council,

and

8

State

Farm

Insurance

Company;

and

9

lOBE

IT

FURTHER

RESOLVED

that

the

working

group

is

also

11

requested

to

develop

alternatives

for

insurance

notices

and

12

documents

that

balance

the

convenience

of

electronic

notices

and

13

documents

with

consumer

protection;

and

14

15

BE

IT

FURTHER

RESOLVED

that

the

representatives

on

the

16

working

group

not

be

considered

state

employees

based

solely

17

upon

their

participation

in

the

working

group;

and

18

19

BE

IT

FURTHER

RESOLVED

that

the

working

group

is

requested

20

to

submit

a

final

report

of

the

working

group's

findings

and

21

recommendations,

including

any

proposed

legislation,

to

the

22

Legislature

no

later

than

twenty

days

prior

to

the

convening

of

23·

the

Regular

Session

of

2014;

and

24

25

BE

IT

FURTHER

RESOLVED

that

certified

copies

of

this

26

Concurrent

Resolution

be

transmitted

to

the

Insurance

27

Commissioner,

Commission

to

Promote

Uniform

Legislation,

28

Property

Casualty

Insurers

Association

of

America,

Hawaii

29

Insurers

Council,

and

State

Farm

Insurance

Company.

30

2013-2101

SCR159 SD1

SMA.doc

IIIIIIIII~III~II~I~III~IIIII~I~IIII~IIIIIIIIIIIIIIIIIIII~IIIIII~IIIII~III1I111~~IIIIIIIIIII~1I1111

15

Mar. 25, 2013 version

MODEL MERGED INSURANCE TRANSACTION MODERNIZATION

ELECTRONIC DELIVERY OR POSTING

AN ACT TO ALLOW THE TRANSMISSION OF ELECTRONIC NOTICES OR

DOCUMENTS RELATED TO INSURANCE AND INSURANCE POLICIES UNDER

CERTAIN CIRCUMSTANCES AND POSTING OF PROPERTY AND CASUALTY

INSURANCE POLICIES AND ENDORSEMENTS WHERE CERTAIN CONDITIONS ARE

MET.

BE IT ENACTED:

Amend XXXXX of the XXXX Code by adding a new section thereto as follows:

§XXXX Electronic Notices and Documents.

1) In this section, the following words shall have the following meanings:

A.“Delivered by electronic means” includes:

1. Delivery to an electronic mail address at which a party has

consented to receive notices or documents; or

2. Posting on an electronic network or site accessible via the internet,

mobile application, computer, mobile device, tablet, or any other

electronic device, together with separate notice of the posting

which shall be provided by electronic mail to the address at which

the party has consented to receive notice or by any other delivery

method that has been consented to by the party.

B. “Party” means any recipient of any notice or document required as part of

an insurance transaction, including but not limited to an applicant, an

insured, a policyholder, or an annuity contract holder.

2) Subject to subsection (4) of this section, any notice to a party or any other

document required under applicable law in an insurance transaction or that is to

serve as evidence of insurance coverage may be delivered, stored, and presented

by electronic means so long as it meets the requirements of the Uniform

Electronic Transactions Act [CITATION].

3) Delivery of a notice or document in accordance with this section shall be

considered equivalent to any delivery method required under applicable law,

including delivery by first class mail; first class mail, postage prepaid; certified

mail; certificate of mail; or certificate of mailing.

16

APPENDIX B

4) A notice or document may be delivered by electronic means by an insurer to a

party under this section if:

A.The party has affirmatively consented to that method of delivery and has

not withdrawn the consent;

B.The party, before giving consent, is provided with a clear and conspicuous

statement informing the party of:

1. Any right or option of the party to have the notice or document

provided or made available in paper or another non-electronic

form.

2. The right of the party to withdraw consent to have a notice or

document delivered by electronic means and any fees, conditions,

or consequences imposed in the event consent is withdrawn;

3. Whether the party’s consent applies:

a. Only to the particular transaction as to which the notice or

document must be given; or

b. To identified categories of notices or documents that may

be delivered by electronic means during the course of the

parties’ relationship;

4. (1) The means, after consent is given, by which a party may

obtain a paper copy of a notice or document delivered by

electronic means; and (2) The fee, if any, for the paper copy; and

5. The procedure a party must follow to withdraw consent to have a

notice or document delivered by electronic means and to update

information needed to contact the party electronically;

C. The party:

1. Before giving consent, is provided with a statement of the

hardware and software requirements for access to and retention of

a notice or document delivered by electronic means; and

2. Consents electronically, or confirms consent electronically, in a

manner that reasonably demonstrates that the party can access

information in the electronic form that will be used for notices or

documents delivered by electronic means as to which the party has

given consent; and

D. After consent of the party is given, the insurer, in the event a change in

the hardware or software requirements needed to access or retain a notice

17

1. Provides the party with a statement of:

a. The revised hardware and software requirements for access

to and retention of a notice or document delivered by

electronic means;

b. The right of the party to withdraw consent without the

imposition of any fee, condition, or consequence that was

not disclosed under (B)(2) of this subsection; and

2. Complies with paragraph (B) of this subsection.

5) This section does not affect requirements related to content or timing of any

notice or document required under applicable law.

6) If a provision of this title or applicable law requiring a notice or document to be

provided to a party expressly requires verification or acknowledgment of receipt

of the notice or document, the notice or document may be delivered by electronic

means only if the method used provides for verification or acknowledgment of

receipt.

7) The legal effectiveness, validity, or enforceability of any contract or policy of

insurance executed by a party may not be denied solely because of the failure to

obtain electronic consent or confirmation of consent of the party in accordance

with subparagraph (4)(C)(2) of this section.

8) (1) A withdrawal of consent by a party does not affect the legal effectiveness,

validity, or enforceability of a notice or document delivered by electronic means

to the party before the withdrawal of consent is effective. (2) A withdrawal of

consent by a party is effective within a reasonable period of time after receipt of

the withdrawal by the insurer. (3) Failure by an insurer to comply with subsection

(4)(D) of this section may be treated, at the election of the party, as a withdrawal

of consent for purposes of this section.

9) This section does not apply to a notice or document delivered by an insurer in an

electronic form before the effective date of this act to a party who, before that

date, has consented to receive notice or document in an electronic form otherwise

allowed by law.

10) If the consent of a party to receive certain notices or documents in an electronic

form is on file with an insurer before the effective date of this act, and pursuant to

this section, an insurer intends to deliver additional notices or documents to such

party in an electronic form, then prior to delivering such additional notices or

documents electronically, the insurer shall notify the party of:

18

A. The notices or documents that may be delivered by electronic means

under this section that were not previously delivered electronically; and

B. The party’s right to withdraw consent to have notices or documents

delivered by electronic means.

11) (1) Except as otherwise provided by law, if an oral communication or a recording

of an oral communication from a party can be reliably stored and reproduced by

an insurer, the oral communication or recording may qualify as a notice or

document delivered by electronic means for purposes of this section. (2) If a

provision of this title or applicable law requires a signature or notice or document

to be notarized, acknowledged, verified, or made under oath, the requirement is

satisfied if the electronic signature of the person authorized to perform those acts,

together with all other information required to be included by the provision, is

attached to or logically associated with the signature, notice or document.

12) This section may not be construed to modify, limit, or supersede the provisions of

the federal Electronic Signatures in Global and National Commerce Act, Public

Law 106-229, as amended.

Amend XXXXX of the XXXX Code by adding a new section thereto as follows:

§ XXXX Posting of Policies on the Internet.

Notwithstanding any other provisions of §XXXX Electronic Notices and Documents,

standard property and casualty insurance policies and endorsements that do not contain

personally identifiable information may be mailed, delivered, or posted on the insurer’s

Web site. If the insurer elects to post insurance policies and endorsements on its Web

site in lieu of mailing or delivering them to the insured, it must comply with all of the

following conditions:

1) The policy and endorsements must be accessible and remain that way for as long

as the policy is in force;

2) After the expiration of the policy, the insurer must archive its expired policies and

endorsements for a period of five years, and make them available upon request;

19

20

3) The policies and endorsements must be posted in a manner that enables the

insured to print and save the policy and endorsements using programs or

applications that are widely available on the Internet and free to use;

4) The insurer provides the following information in, or simultaneous with each

declarations page provided at the time of issuance of the initial policy and any

renewals of that policy:

A. a description of the exact policy and endorsement forms purchased by the

insured;

B. a method by which the insured may obtain, upon request and without

charge, a paper copy of their policy; and

C. the internet address where their policy and endorsements are posted,

and;

5) The insurer provides notice, in the format preferred by the insured, of any changes

to the forms or endorsements, the insured’s right to obtain, upon request and

without charge, a paper copy of such forms or endorsements, and the internet

address where such forms or endorsements are posted.

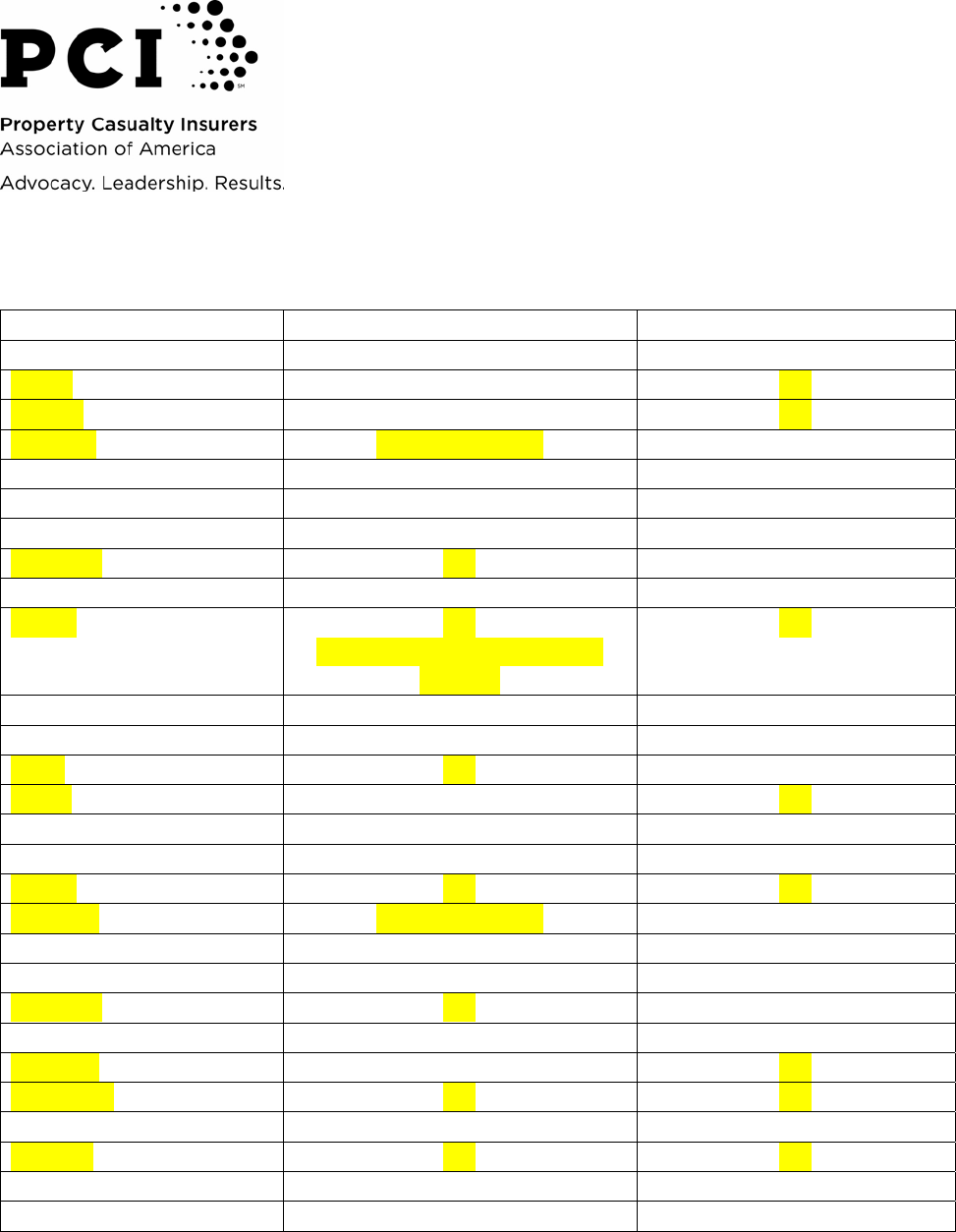

e‐Delivery/e‐Posting–Laws&Regulations*

STATE E‐DELIVERY E‐POSTING

Alabama No No

Alaska No Yes

Arizona No Yes

Arkansas Yes(DOIbulletin) No

California No No

Colorado No No

Connecticut No No

Delaware Yes No

D.C. No No

Florida Yes

(commercialonly;policyonly;

opt‐out)

Yes

Georgia No No

Hawaii No No

Idaho Yes No

Illinois No Yes

Indiana No No

Iowa No No

Kansas Yes Yes

Kentucky Yes(DOIbulletin) No

Louisiana No No

Maine No No

Maryland Yes No

Massachusetts No No

Michigan No Yes

Minnesota Yes Yes

Mississippi No No

Missouri Yes Yes

Montana No No

Nebraska No No

*Thelawsandregulationsincludedwithinthischarthavebeenenactedandpromulgatedspecificallyinregardsto

insurance.ThischartdoesnotincludecitationtogenerallyapplicableelectroniccommercestatutessuchasE‐SIGNand

UETA.

21

APPENDIX C

22

Nevada No No

NewHampshire No No

NewJersey No No

NewMexico No No

NewYork No No

NorthCarolina Yes No

NorthDakota No No

Ohio No No

Oklahoma No Yes

Oregon No No

Pennsylvania Yes Yes

RhodeIsland No No

SouthCarolina No No

SouthDakota No No

Tennessee Yes(DOIbulletin) No

Texas Yes Yes

Utah No No

Vermont No No

Virginia Yes Yes

Washington No No

WestVirginia No No

Wisconsin No No

Wyoming No No

Totalstatesw/e‐Delivery: 14outof51

Totalstatesw/e‐Posting:12outof51

e‐Deliveryrefersbroadlytotheelectronicdeliveryofanyandallinsurancedocuments(includingpolicy,

notices,bills)topolicyholderswhocons ent(i.e.,opt‐in)toreceivesuchmaterialselectronically.

e‐Posting,orPostingPoliciestotheIn

t

ernet,referstothepostingofpolicyformsandendorsementsthatdo

notcontainpersonallyidentifiableinformationtotheInternetandsendingalinktothematerialsviae‐mail

tothepolicyholderinlieuofmailingpapercopiestothepolicyholder.Provisionofthesematerialsviathis

methodismade

withouttheconsentofthepolicyholder,andthosepolicyholderswishingtoreceivepaper

copiesmustrequestsuchfromtheirinsurer(i.e.,opt‐out).E‐Postingiseasilyconfusedwithe‐Delivery;

however,therearedistinctdifferences.E‐Deliveryreferstotheelectronicdeliveryofseveraltypesof

documentsandrequiresthepoli

cyholder’sconsent;e‐Postingislimitedtopolicyformsandendorsement

thatcontainnopersonallyidentifiableinformationanddoesnotrequiretheconsentofthepolicyholder.