Userid: CPM Schema: instrx Leadpct: 100% Pt. size: 9

Draft Ok to Print

AH XSL/XML

Fileid: … ons/i1120s/2023/a/xml/cycle05/source (Init. & Date) _______

Page 1 of 55 10:19 - 17-Jan-2024

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

2023

Instructions for Form 1120-S

U.S. Income Tax Return for an S Corporation

Department of the Treasury

Internal Revenue Service

Section references are to the Internal Revenue Code unless

otherwise noted.

Contents Page

What’s New ............................... 1

Photographs of Missing Children ................ 2

The Taxpayer Advocate Service ................. 2

Direct Deposit of Refund ...................... 2

How To Get Forms and Publications .............. 2

General Instructions ......................... 2

Purpose of Form ......................... 2

How To Make the Election .................. 2

Who Must File .......................... 2

Termination of Election .................... 2

Electronic Filing ......................... 3

When To File ........................... 3

Where To File ........................... 4

Who Must Sign .......................... 3

Paid Preparer Authorization ................. 3

Assembling the Return .................... 4

Tax Payments ........................... 4

Electronic Deposit Requirement .............. 4

Estimated Tax Payments ................... 5

Interest and Penalties ..................... 5

Accounting Methods ...................... 6

Accounting Period ....................... 6

Rounding Off to Whole Dollars ............... 6

Recordkeeping .......................... 6

Amended Return ........................ 6

Other Forms and Statements That May Be

Required ............................ 7

At-Risk Limitations ....................... 8

Passive Activity Limitations ................. 8

Net Investment Income Tax Reporting

Requirements ........................ 13

Specific Instructions ........................ 13

Income .............................. 14

Deductions ........................... 16

Tax and Payments ...................... 21

Schedule B. Other Information .............. 22

Schedules K and K-1 (General Instructions) .... 24

Specific Instructions (Schedule K-1 Only) ...... 25

Part I. Information About the Corporation ...... 25

Part II. Information About the Shareholder ...... 25

Specific Instructions (Schedules K and K-1,

Part III) ............................. 26

Schedule L. Balance Sheets per Books ....... 47

Schedule M-1. Reconciliation of Income

(Loss) per Books With Income (Loss) per

Return ............................. 48

Contents Page

Schedule M-2. Analysis of AAA, PTEP,

Accumulated E&P, and OAA ............. 48

Principal Business Activity Codes .............. 52

Index ................................... 55

Future Developments

For the latest information about developments related to Form

1120-S and its instructions, such as legislation enacted after

they were published, go to

IRS.gov/Form1120S.

What’s New

Electronically filed returns. The electronic filing threshold for

corporate returns required to be filed on or after January 1, 2024,

has decreased to 10 or more returns. See Electronic Filing, later.

Increase in penalty for failure to file. For tax returns required

to be filed in 2024, the minimum penalty for failure to file a return

that is more than 60 days late has increased to the smaller of the

tax due or $485. See

Late filing of return, later.

Deduction for certain energy efficient commercial building

property. For tax years beginning in 2023, corporations filing

Form 1120-S and claiming the energy efficient commercial

buildings deduction should report the deduction on line 19. See

the instructions for line 19.

Expiration of 100% business meal expense deduction. The

temporary 100% business meal expense deduction for food and

beverages provided by a restaurant does not apply to amounts

paid or incurred after 2022.

Elective payment election. Applicable entities and electing

taxpayers can elect to treat certain credits as elective payments.

See the instructions for line 24d and the Instructions for Form

3800.

Digital assets. Digital assets are required to be reported. See

new

question 16 on Schedule B, later.

Schedules K and K-1 reporting codes. Separate reporting

codes are assigned to items grouped under code H for Other

income (loss), code S for Other deductions, code P for Other

credits, and code AD for Other information in prior years. See the

List of Codes in the Shareholder's Instructions for Schedule K-1

(Form 1120-S).

The following new reporting credit codes are added to

line 13g.

•

Code A. Zero-emission nuclear power production credit.

•

Code B. Production from advanced nuclear power facilities

credit.

•

Code AG. Credit for military spouse participation.

•

Code AX. Carbon oxide sequestration credit recapture.

•

Code AY. New clean vehicle credit.

•

Code BC. Eligible credits from transferor(s) under section

6418.

Reminder

Election by a small business corporation. Don't file Form

1120-S unless the corporation has filed or is attaching Form

Jan 17, 2024

Cat. No. 11515K

Page 2 of 55 Fileid: … ons/i1120s/2023/a/xml/cycle05/source 10:19 - 17-Jan-2024

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

2553, Election by a Small Business Corporation. For details, see

the Instructions for Form 2553.

Photographs of

Missing Children

The Internal Revenue Service is a proud partner with the

National Center for Missing & Exploited Children® (NCMEC).

Photographs of missing children selected by the Center may

appear in instructions on pages that would otherwise be blank.

You can help bring these children home by looking at the

photographs and calling 1-800-THE-LOST (1-800-843-5678) if

you recognize a child.

The Taxpayer Advocate Service

The Taxpayer Advocate Service (TAS) is an independent

organization within the IRS that helps taxpayers and protects

taxpayer rights. TAS strives to ensure that every taxpayer is

treated fairly and knows and understands their rights under the

Taxpayer Bill of Rights.

As a taxpayer, the corporation has rights that the IRS must

abide by in its dealings with the corporation. TAS can help the

corporation if:

•

A problem is causing financial difficulty for the business;

•

The business is facing an immediate threat of adverse action;

or

•

The corporation has tried repeatedly to contact the IRS but no

one has responded, or the IRS hasn't responded by the date

promised.

TAS has offices in every state, the District of Columbia, and

Puerto Rico. Local advocates' numbers are in their local

directories and at

TaxpayerAdvocate.IRS.gov. The corporation

can also call TAS at 877-777-4778.

TAS also works to resolve large-scale or systemic problems

that affect many taxpayers. If the corporation knows of one of

these broad issues, please report it to TAS through the Systemic

Advocacy Management System at

IRS.gov/SAMS.

For more information, go to IRS.gov/Advocate.

Direct Deposit of Refund

To request a direct deposit of the corporation's income tax refund

into an account at a U.S. bank or other financial institution, attach

Form 8050, Direct Deposit of Corporate Tax Refund. See the

instructions for line 28.

How To Get Forms and Publications

Internet. You can access the IRS website 24 hours a day, 7

days a week, at IRS.gov to:

•

Download forms, instructions, and publications;

•

Order IRS products online;

•

Research your tax questions online;

•

Search publications online by topic or keyword;

•

View Internal Revenue Bulletins (IRBs) published in recent

years; and

•

Sign up to receive local and national tax news by email.

Tax forms and publications. The corporation can view, print,

or download all of the forms and publications it may need on

IRS.gov/FormsPubs. Otherwise, the corporation can go to

IRS.gov/OrderForms to place an order and have forms mailed to

it.

General Instructions

Purpose of Form

Use Form 1120-S to report the income, gains, losses,

deductions, credits, and other information of a domestic

corporation or other entity for any tax year covered by an election

to be an S corporation.

How To Make the Election

For details about the election, see Form 2553, Election by a

Small Business Corporation, and the Instructions for Form 2553.

Who Must File

A corporation or other entity must file Form 1120-S if (a) it

elected to be an S corporation by filing Form 2553, (b) the IRS

accepted the election, and (c) the election remains in effect.

After filing Form 2553, you should have received confirmation

that Form 2553 was accepted. If you didn't receive notification of

acceptance or nonacceptance of the election within 2 months of

filing Form 2553 (5 months if you checked box Q1 to ask for a

letter ruling), please follow up by calling 800-829-4933. Don't file

Form 1120-S for any tax year before the year the election takes

effect.

Relief for late elections. If you haven't filed Form 2553, or

didn't file Form 2553 on time, you may be entitled to relief for a

late-filed election to be an S corporation. See the Instructions for

Form 2553 for details.

Termination of Election

Once the election is made, it stays in effect until it is terminated.

If the election is terminated, the corporation (or a successor

corporation) can make another election on Form 2553 only with

IRS consent for any tax year before the fifth tax year after the first

tax year in which the termination took effect. See Regulations

section 1.1362-5 for details.

An election terminates automatically in any of the following

cases.

1. The corporation is no longer a small business corporation

as defined in section 1361(b). This kind of termination of an

election is effective as of the day the corporation no longer

meets the definition of a small business corporation. Attach to

Form 1120-S for the final year of the S corporation a statement

notifying the IRS of the termination and the date it occurred.

2. For each of 3 consecutive tax years, the corporation (a)

has accumulated earnings and profits (AE&P), and (b) derives

more than 25% of its gross receipts from passive investment

income as defined in section 1362(d)(3)(C). The election

terminates on the first day of the 1st tax year beginning after the

3rd consecutive tax year. The corporation must pay a tax for

each year it has excess net passive income. See the line 23a

instructions for details on how to figure the tax.

3. The election is revoked. An election can be revoked only

with the consent of shareholders who, at the time the revocation

is made, hold more than 50% of the number of issued and

outstanding shares of stock (including nonvoting stock). The

revocation can specify an effective revocation date that is on or

after the day the revocation is filed. If no date is specified, the

revocation is effective at the start of the tax year if the revocation

is made on or before the 15th day of the 3rd month of that tax

year. If no date is specified and the revocation is made after the

15th day of the 3rd month of the tax year, the revocation is

effective at the start of the next tax year.

To revoke the election, the corporation must file a statement

with the appropriate service center listed under Where To File in

the Instructions for Form 2553. In the statement, the corporation

must notify the IRS that it is revoking its election to be an S

corporation. The statement must be signed by each shareholder

who consents to the revocation and contain the information

required by Regulations section 1.1362-6(a)(3).

A revocation can be rescinded before it takes effect. See

Regulations section 1.1362-6(a)(4) for details.

2

Instructions for Form 1120-S (2023)

Page 3 of 55 Fileid: … ons/i1120s/2023/a/xml/cycle05/source 10:19 - 17-Jan-2024

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

For rules on allocating income and deductions between an S

corporation's short year and a C corporation's short year and

other special rules that apply when an election is terminated, see

section 1362(e) and Regulations section 1.1362-3.

If an election was terminated under (1) or (2) above and the

corporation believes the termination was inadvertent, the

corporation can ask for permission from the IRS to continue to

be treated as an S corporation. See Regulations section

1.1362-4 for the specific requirements that must be met to

qualify for inadvertent termination relief.

Electronic Filing

S corporations can generally electronically file (e-file) Form

1120-S, related forms, schedules, statements, and attachments;

Form 7004 (automatic extension of time to file); and Forms 940,

941, and 944 (employment tax returns). Form 1099 and other

information returns can also be electronically filed. The option to

e-file doesn't, however, apply to certain returns.

For returns filed on or after January 1, 2024, S corporations

that file 10 or more returns are required to e-file Form 1120-S.

See Regulations section 301.6037-2. However, these

corporations can request a waiver of the electronic filing

requirements.

For more information on e-filing, see E-file for Business and

Self Employed Taxpayers on IRS.gov.

Exclusions From Electronic Filing Requirement

Waivers. The IRS may waive the electronic filing rules if the S

corporation demonstrates that a hardship would result if it were

required to file its return electronically. A corporation interested in

requesting a waiver of the mandatory electronic filing

requirement must file a written request, and request one in the

manner prescribed by the IRS. All written requests for waivers

should be mailed to:

Internal Revenue Service

Ogden Submission Processing Center

Attn: Form 1120 e-file Waiver Request

Mail Stop 1057

Ogden, UT 84201

If using a delivery service, requests for waivers should be

mailed to:

Internal Revenue Service

Ogden Submission Processing Center

Attn: Form 1120 e-file Waiver Request

Mail Stop 1057

1973 N. Rulon White Blvd.

Ogden, UT 84404

Waiver requests can also be faxed to 877-477-0575. Contact

the e-Help Desk at 866-255-0654 for questions regarding the

waiver procedures or process.

Exemptions. The IRS may provide exemptions from the

requirements to electronically file. If using the technology

required to electronically file conflicts with religious beliefs, the

corporation is exempt from the requirement. Clearly indicate the

exemption on the corporation’s return. Write “Religious

Exemption” at the top of the Form 1120-S. File the return at the

applicable IRS address. See

Where To File, later. For more

information, see Notice 2024-18.

When To File

Generally, an S corporation must file Form 1120-S by the 15th

day of the 3rd month after the end of its tax year. For calendar

year corporations, the due date is March 15, 2024. A corporation

that has dissolved must generally file by the 15th day of the 3rd

month after the date it dissolved.

If the due date falls on a Saturday, Sunday, or legal holiday,

the corporation can file on the next day that isn’t a Saturday,

Sunday, or legal holiday.

If the S corporation election was terminated during the tax

year and the corporation reverts to a C corporation, file Form

1120-S for the S corporation's short year by the due date

(including extensions) of the C corporation's short year return.

Private Delivery Services

Corporations can use certain private delivery services (PDS)

designated by the IRS to meet the “timely mailing as timely filing”

rule for tax returns. Go to IRS.gov/PDS for the current list of

designated services.

The PDS can tell you how to get written proof of the mailing

date.

For the IRS mailing address to use if you are using a PDS, go

to

IRS.gov/PDSStreetAddresses.

Private delivery services can't deliver items to P.O.

boxes. You must use the U.S. Postal Service to mail any

item to an IRS P.O. box address.

Extension of Time To File

File Form 7004, Application for Automatic Extension of Time To

File Certain Business Income Tax, Information, and Other

Returns, to ask for an extension of time to file. Generally, the

corporation must file Form 7004 by the regular due date of the

return. See the Instructions for Form 7004.

Who Must Sign

The return must be signed and dated by:

•

The president, vice president, treasurer, assistant treasurer,

chief accounting officer; or

•

Any other corporate officer (such as tax officer) authorized to

sign.

If a return is filed on behalf of a corporation by a receiver,

trustee, or assignee, the fiduciary must sign the return instead of

the corporate officer. Returns and forms signed by a receiver or

trustee in bankruptcy on behalf of a corporation must be

accompanied by a copy of the order or instructions of the court

authorizing signing of the return or form.

If an employee of the corporation completes Form 1120-S,

the paid preparer space should remain blank. Anyone who

prepares Form 1120-S but doesn't charge the corporation

shouldn't complete that section. Generally, anyone who is paid to

prepare the return must sign it and fill in the “Paid Preparer Use

Only” area.

The paid preparer must complete the required preparer

information and:

•

Sign the return in the space provided for the preparer's

signature,

•

Include their Preparer Tax Identification Number (PTIN), and

•

Give a copy of the return to the taxpayer.

A paid preparer may sign original or amended returns by

rubber stamp, mechanical device, or computer software

program.

Paid Preparer Authorization

If the corporation wants to allow the IRS to discuss its 2023 tax

return with the paid preparer who signed it, check the “Yes” box

in the signature area of the return. This authorization applies only

to the individual whose signature appears in the “Paid Preparer

CAUTION

!

TIP

Instructions for Form 1120-S (2023)

3

Page 4 of 55 Fileid: … ons/i1120s/2023/a/xml/cycle05/source 10:19 - 17-Jan-2024

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Use Only” section of the return. It doesn't apply to the firm, if any,

shown in that section.

If the “Yes” box is checked, the corporation is authorizing the

IRS to call the paid preparer to answer any questions that may

arise during the processing of its return. The corporation is also

authorizing the paid preparer to:

•

Give the IRS any information that is missing from the return;

•

Call the IRS for information about the processing of the return

or the status of any related refund or payment(s); and

•

Respond to certain IRS notices about math errors, offsets,

and return preparation.

The corporation isn't authorizing the paid preparer to receive

any refund check, bind the corporation to anything (including any

additional tax liability), or otherwise represent the corporation

before the IRS.

The authorization will automatically end no later than the due

date (excluding extensions) for filing the corporation's 2024 tax

return. If the corporation wants to expand the paid preparer's

authorization or revoke the authorization before it ends, see Pub.

947, Practice Before the IRS and Power of Attorney.

Assembling the Return

To ensure that the corporation's tax return is correctly processed,

attach all schedules and other forms after page 5 of Form

1120-S in the following order.

1. Schedule N (Form 1120), Foreign Operations of U.S.

Corporations.

2. Schedule D (Form 1120-S), Capital Gains and Losses

and Built-in Gains.

3. Form 4797, Sales of Business Property.

4. Form 8949, Sales and Other Dispositions of Capital

Assets.

5. Form 8996, Qualified Opportunity Fund.

6. Form 8825, Rental Real Estate Income and Expenses of

a Partnership or an S Corporation.

7. Form 1125-A, Cost of Goods Sold.

8. Form 8050, Direct Deposit of Corporate Tax Refund.

9. Form 4136, Credit for Federal Tax Paid on Fuels.

10.

Form 8941, Credit for Small Employer Health Insurance

Premiums.

11.

Form 3800, General Business Credit.

12.

Form 8997, Initial and Annual Statement of Qualified

Opportunity Fund (QOF) Investments.

13.

Form 6252, Installment Sale Income.

14.

Schedule A (Form 8936), Clean Vehicle Credit Amount.

15.

Schedules K-1 (Form 1120-S), Shareholder's Share of

Income, Deductions, Credits, etc.

16.

Form 8938, Statement of Specified Foreign Financial

Assets.

17.

Additional schedules in alphabetical order, including

Schedule K-2 (Form 1120-S), Shareholders' Pro Rata Share

Items—International, and Schedules K-3 (Form 1120-S),

Shareholder's Share of Income, Deductions, Credits,

etc.—International.

18.

Additional forms in numerical order.

Complete every applicable entry space on Form 1120-S and

Schedule K-1. Don't enter “See Attached” or “Available Upon

Request” instead of completing the entry spaces. If more space

is needed on the forms or schedules, attach separate sheets

using the same size and format as the printed forms.

If there are supporting statements and attachments, arrange

them in the same order as the schedules or forms they support

and attach them last. Show the totals on the printed forms. Enter

the corporation's name and EIN on each supporting statement or

attachment.

Tax Payments

Generally, the corporation must pay any tax due in full no later

than the due date for filing its tax return (not including

extensions). See the

instructions for line 26. If the due date falls

on a Saturday, Sunday, or legal holiday, the payment is due on

the next day that isn't a Saturday, Sunday, or legal holiday.

Electronic Deposit Requirement

Corporations must use electronic funds transfers to make all

federal tax deposits (such as deposits of employment, excise,

and corporate income tax). Generally, electronic funds transfers

are made using the Electronic Federal Tax Payment System

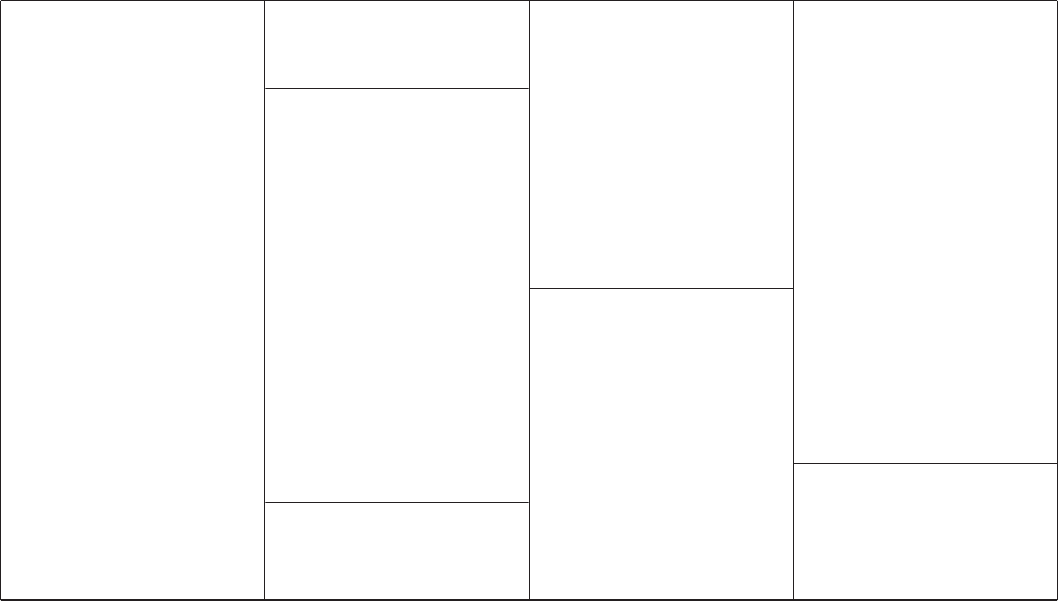

Where To File

File the corporation's return at the applicable IRS address listed below.

If the corporation's principal business,

office, or agency is located in:

And the total assets at the end of the tax

year (Form 1120-S, page 1, item F) are:

Use the following address:

Connecticut, Delaware, District of Columbia,

Georgia, Illinois, Indiana, Kentucky, Maine,

Maryland, Massachusetts, Michigan, New

Hampshire, New Jersey, New York, North

Carolina, Ohio, Pennsylvania, Rhode Island,

South Carolina, Tennessee, Vermont, Virginia,

West Virginia, Wisconsin

Less than $10 million and

Schedule M-3 isn't filed

Department of the Treasury

Internal Revenue Service Center

Kansas City, MO 64999-0013

$10 million or more, or

less than $10 million and

Schedule M-3 is filed

Department of the Treasury

Internal Revenue Service Center

Ogden, UT 84201-0013

Alabama, Alaska, Arizona, Arkansas, California,

Colorado, Florida, Hawaii, Idaho, Iowa, Kansas,

Louisiana, Minnesota, Mississippi, Missouri,

Montana, Nebraska, Nevada, New Mexico,

North Dakota, Oklahoma, Oregon, South

Dakota, Texas, Utah, Washington, Wyoming

Any amount

Department of the Treasury

Internal Revenue Service Center

Ogden, UT 84201-0013

A foreign country or U.S. territory Any amount

Internal Revenue Service Center

P.O. Box 409101

Ogden, UT 84409

4

Instructions for Form 1120-S (2023)

Page 5 of 55 Fileid: … ons/i1120s/2023/a/xml/cycle05/source 10:19 - 17-Jan-2024

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

(EFTPS). However, if the corporation doesn't want to use

EFTPS, it can arrange for its tax professional, financial

institution, payroll service, or other trusted third party to make

deposits on its behalf. Also, it may arrange for its financial

institution to submit a same-day wire payment (discussed below)

on its behalf. EFTPS is a free service provided by the

Department of the Treasury. Services provided by a tax

professional, financial institution, payroll service, or other third

party may have a fee.

To get more information about EFTPS or to enroll in EFTPS,

visit

www.EFTPS.gov or call 800-555-4477. To contact EFTPS

using the Telecommunications Relay Services (TRS), for people

who are deaf, hard of hearing, or have a speech disability, dial

711 and provide the TRS assistant the 800-555-4477 number

above or 800-733-4829.

Depositing on time. For any deposit made by EFTPS to be on

time, the corporation must submit the deposit by 8 p.m. Eastern

time the day before the date the deposit is due. If the corporation

uses a third party to make deposits on its behalf, they may have

different cutoff times.

Same-day wire payment option. If the corporation fails to

submit a deposit transaction on EFTPS by 8 p.m. Eastern time

the day before the date a deposit is due, it can still make its

deposit on time by using the Federal Tax Collection Service

(FTCS). To use the same-day wire payment method, the

corporation will need to make arrangements with its financial

institution ahead of time regarding availability, deadlines, and

costs. Financial institutions may charge a fee for payment made

this way. To learn more about the information the corporation will

need to provide to its financial institution to make a same-day

wire payment, go to

IRS.gov/SameDayWire.

Estimated Tax Payments

Generally, the corporation must make installment payments of

estimated tax for the following taxes if the total of these taxes is

$500 or more: (a) the tax on built-in gains, (b) the excess net

passive income tax, and (c) the investment credit recapture tax,

each discussed later.

The amount of estimated tax required to be paid annually is

the smaller of (a) the total of the above taxes shown on the return

for the tax year (or if no return is filed, the total of these taxes for

the year), or (b) the sum of (i) the investment credit recapture tax

and the built-in gains tax shown on the return for the tax year (or

if no return is filed, the total of these taxes for the tax year), and

(ii) any excess net passive income tax shown on the

corporation's return for the preceding tax year. If the preceding

tax year was less than 12 months, the estimated tax must be

determined under (a).

The estimated tax is generally payable in four equal

installments. However, the corporation may be able to lower the

amount of one or more installments by using the annualized

income installment method or adjusted seasonal installment

method under section 6655(e).

For a calendar year corporation, the payments are due for

2024 by April 15, June 15, September 15, and December 15. For

a fiscal year corporation, they are due by the 15th day of the 4th,

6th, 9th, and 12th months of the year. If any date falls on a

Saturday, Sunday, or legal holiday, the installment is due on the

next day that isn't a Saturday, Sunday, or legal holiday.

The corporation must make the payments using electronic

funds transfers as described earlier.

For information on penalties that may apply if the corporation

fails to make required payments, see the Instructions for Form

2220.

Interest and Penalties

If the corporation receives a notice about penalties after

it files its return, send the IRS an explanation and we will

determine if the corporation meets reasonable-cause

criteria.

Don't attach an explanation when the corporation's

return is filed.

Interest. Interest is charged on taxes paid late even if an

extension of time to file is granted. Interest is also charged on

penalties imposed for failure to file, negligence, fraud, substantial

valuation misstatements, substantial understatements of tax,

and reportable transaction understatements from the due date

(including extensions) to the date of payment. The interest

charge is figured at a rate determined under section 6621.

Late filing of return. A penalty may be assessed if the return is

filed after the due date (including extensions) or the return

doesn't show all the information required, unless each failure is

due to reasonable cause. See

Caution, earlier. For returns on

which no tax is due, the penalty is $235 for each month or part of

a month (up to 12 months) the return is late or doesn't include

the required information, multiplied by the total number of

persons who were shareholders in the corporation during any

part of the corporation's tax year for which the return is due. If tax

is due, the penalty is the amount stated above plus 5% of the

unpaid tax for each month or part of a month the return is late, up

to a maximum of 25% of the unpaid tax. The minimum penalty

for a tax return required to be filed in 2024 that is more than 60

days late is the smaller of the tax due or $485.

Late payment of tax. A corporation that doesn't pay the tax

when due may generally be penalized

1

/2 of 1% of the unpaid tax

for each month or part of a month the tax isn't paid, up to a

maximum of 25% of the unpaid tax. The penalty won't be

imposed if the corporation can show that the failure to pay on

time was due to reasonable cause. See

Caution, earlier.

Failure to furnish information timely. For each failure to

furnish Schedule K-1 (and Schedule K-3, if applicable) to a

shareholder when due and each failure to include on

Schedule K-1 (and Schedule K-3, if applicable) all the

information required to be shown (or the inclusion of incorrect

information), a $310 penalty may be imposed with respect to

each Schedule K-1 (and Schedule K-3, if applicable) for which a

failure occurs. If the requirement to report correct information is

intentionally disregarded, each $310 penalty is increased to

$630 or, if greater, 10% of the aggregate amount of items

required to be reported. See sections 6722 and 6724 for more

information.

The penalty won't be imposed if the corporation can show

that not furnishing information timely was due to reasonable

cause. See Caution, earlier.

Trust fund recovery penalty. This penalty may apply if certain

excise, income, social security, and Medicare taxes that must be

collected or withheld aren't collected or withheld, or these taxes

aren't paid. These taxes are generally reported on:

•

Form 720, Quarterly Federal Excise Tax Return;

•

Form 941, Employer's QUARTERLY Federal Tax Return;

•

Form 943, Employer's Annual Federal Tax Return for

Agricultural Employees;

•

Form 944, Employer's ANNUAL Federal Tax Return; or

•

Form 945, Annual Return of Withheld Federal Income Tax.

The trust fund recovery penalty may be imposed on all

persons who are determined by the IRS to have been

responsible for collecting, accounting for, or paying over these

taxes, and who acted willfully in not doing so. The penalty is

equal to the full amount of the unpaid trust fund tax. See the

Instructions for Form 720, Pub. 15 (Circular E), Employer's Tax

Guide, or Pub. 51 (Circular A), Agricultural Employer's Tax

CAUTION

!

Instructions for Form 1120-S (2023)

5

Page 6 of 55 Fileid: … ons/i1120s/2023/a/xml/cycle05/source 10:19 - 17-Jan-2024

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Guide, for details, including the definition of “responsible

persons.”

Other penalties. Other penalties can be imposed for

negligence, substantial understatement of tax, reportable

transaction understatements, and fraud. See sections 6662,

6662A, and 6663.

Accounting Methods

Figure income using the method of accounting regularly used in

keeping the corporation's books and records. The method used

must clearly reflect income. Permissible methods include cash,

accrual, or any other method authorized by the Internal Revenue

Code.

The following rules apply.

•

Generally, an S corporation can't use the cash method of

accounting if it’s a tax shelter (as defined in section 448(d)(3)).

See section 448 for details.

•

A corporation must use an accrual method for sales and

purchases of inventory items unless it is a small business

taxpayer (defined later). See the Form 1125-A instructions. If you

are a small business taxpayer, you can adopt or change your

accounting method to account for inventories (i) in the same

manner as materials and supplies that are non-incidental, or (ii)

to conform to the taxpayer’s treatment of inventories in an

applicable financial statement (as defined in section 451(b)(3))

or, if the taxpayer doesn’t have an applicable financial statement,

the method of accounting used in the taxpayer’s books and

records prepared in accordance with the taxpayer’s accounting

procedures. Generally, IRS consent is required for changes in

accounting methods. See Rev. Proc. 2018-40 for the procedures

by which a small business taxpayer may obtain automatic

consent to change its method of accounting to reflect the

statutory changes made in this area. Also, see

Change in

accounting method, later.

•

Special rules apply to long-term contracts. See section 460.

•

Generally, dealers in securities must use the mark-to-market

accounting method. Dealers in commodities and traders in

securities and commodities can elect to use the mark-to-market

accounting method. See section 475.

Small business taxpayer. A small business taxpayer is a

taxpayer that (a) has average annual gross receipts of $29

million or less for the 3 prior tax years, and (b) isn’t a tax shelter

(as defined in section 448(d)(3)).

Change in accounting method. Generally, the corporation

must get IRS consent to change either an overall method of

accounting or the accounting treatment of any material item for

income tax purposes. To obtain consent, the corporation must

generally file Form 3115, Application for Change in Accounting

Method, during the tax year for which the change is requested.

See the Instructions for Form 3115 and Pub. 538, Accounting

Periods and Methods, for more information and exceptions. See

also the Instructions for Form 3115 for procedures that may

apply for obtaining automatic consent to change certain

methods of accounting, non-automatic change procedures, and

reduced Form 3115 filing requirements.

Accounting Period

A corporation must figure its income on the basis of a tax year. A

tax year is the annual accounting period a corporation uses to

keep its records and report its income and expenses.

An S corporation must use one of the following tax years.

•

A tax year ending December 31.

•

A natural business year.

•

An ownership tax year.

•

A tax year elected under section 444.

•

A 52-53-week tax year that ends with reference to a year

listed above.

•

Any other tax year (including a 52-53-week tax year) for which

the corporation establishes a business purpose.

A new S corporation must use Form 2553 to elect a tax year.

To later change the corporation's tax year, see Form 1128,

Application To Adopt, Change, or Retain a Tax Year, and its

instructions (unless the corporation is making an election under

section 444, discussed next).

Electing a tax year under section 444. Under the provisions

of section 444, an S corporation can elect to have a tax year

other than a required year, but only if the deferral period of the

tax year isn't longer than the shorter of 3 months or the deferral

period of the tax year being changed. This election is made by

filing Form 8716, Election To Have a Tax Year Other Than a

Required Tax Year.

An S corporation may not make or continue an election under

section 444 if it is a member of a tiered structure, other than a

tiered structure that consists entirely of partnerships and S

corporations that have the same tax year. For the S corporation

to have a section 444 election in effect, it must make the

payments required by section 7519. See Form 8752, Required

Payment or Refund Under Section 7519.

A section 444 election ends if an S corporation:

•

Changes its accounting period to a calendar year or some

other permitted year,

•

Is penalized for willfully failing to comply with the requirements

of section 7519, or

•

Terminates its S election (unless it immediately becomes a

personal service corporation).

If the termination results in a short tax year, enter at the top of

the first page of Form 1120-S for the short tax year, “SECTION

444 ELECTION TERMINATED.”

Rounding Off to Whole Dollars

The corporation may enter decimal points and cents when

completing its return. However, the corporation should round off

cents to whole dollars on its return, forms, and schedules to

make completing its return easier. The corporation must either

round off all amounts on its return to whole dollars, or use cents

for all amounts. To round, drop amounts under 50 cents and

increase amounts from 50 to 99 cents to the next dollar. For

example, $8.40 rounds to $8 and $8.50 rounds to $9.

If two or more amounts must be added to figure the amount to

enter on a line, include cents when adding the amounts and

round off only the total.

Recordkeeping

Keep the corporation's records for as long as they may be

needed for the administration of any provision of the Internal

Revenue Code. Usually, records that support an item of income,

deduction, or credit on the return must be kept for 3 years from

the date each shareholder's return is due or filed, whichever is

later. Keep records that verify the corporation's basis in property

for as long as they are needed to figure the basis of the original

or replacement property.

The corporation should keep copies of all filed returns. They

help in preparing future and amended returns.

Amended Return

To correct a previously filed Form 1120-S, file an amended Form

1120-S and check box H(4) on page 1. Attach a statement that

identifies the line number of each amended item, the corrected

amount or treatment of the item, and an explanation of the

reasons for each change.

If the income, deductions, credits, or other information

provided to any shareholder on Schedule K-1 or K-3 is incorrect,

file an amended Schedule K-1 or K-3 (Form 1120-S) for that

6

Instructions for Form 1120-S (2023)

Page 7 of 55 Fileid: … ons/i1120s/2023/a/xml/cycle05/source 10:19 - 17-Jan-2024

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

shareholder with the amended Form 1120-S. Also give a copy of

the amended Schedule K-1 or K-3 to that shareholder. Check

the “Amended K-1” or “Amended K-3” box at the top of the

Schedule K-1 or K-3 to indicate that it is an amended

Schedule K-1 or K-3.

A change to the corporation's federal return may affect its

state return. This includes changes made as the result of an IRS

examination. For more information, contact the state tax agency

for the state(s) in which the corporation's return was filed.

Other Forms and Statements That

May Be Required

Reportable transaction disclosure statement. Disclose

information for each reportable transaction in which the

corporation participated. Form 8886, Reportable Transaction

Disclosure Statement, must be filed for each tax year the

corporation participated in the transaction. The corporation may

have to pay a penalty if it is required to file Form 8886 and

doesn't do so. The following are reportable transactions.

1. Any listed transaction, which is a transaction that is the

same as or substantially similar to one of the types of

transactions that the IRS has determined to be a tax avoidance

transaction and identified by notice, regulation, or other

published guidance as a listed transaction.

2. Any transaction offered under conditions of confidentiality

for which the corporation (or a related party) paid an advisor a

fee of at least $50,000.

3. Certain transactions for which the corporation (or a

related party) has contractual protection against disallowance of

the tax benefits.

4. Certain transactions resulting in a loss of at least $2

million in any single year or $4 million in any combination of

years.

5. Any transaction identified by the IRS by notice, regulation,

or other published guidance as a “transaction of interest.”

For more information, see Regulations section 1.6011-4. Also

see the Instructions for Form 8886.

Penalties. The corporation may have to pay a penalty if it is

required to disclose a reportable transaction under section 6011

and fails to properly complete and file Form 8886. Penalties may

also apply under section 6707A if the corporation fails to file

Form 8886 with its corporate return, fails to provide a copy of

Form 8886 to the Office of Tax Shelter Analysis (OTSA), or files a

form that fails to include all the information required (or includes

incorrect information). Other penalties, such as an

accuracy-related penalty under section 6662A, may also apply.

See the Instructions for Form 8886 for details on these and other

penalties.

Reportable transactions by material advisors. Material

advisors to any reportable transaction must disclose certain

information about the reportable transaction by filing Form 8918,

Material Advisor Disclosure Statement, with the IRS. For details,

see the Instructions for Form 8918.

Transfers to a corporation controlled by the transferor.

Every significant transferor (as defined in Regulations section

1.351-3(d)) that receives stock of a corporation in exchange for

property in a nonrecognition event must include the statement

required by Regulations section 1.351-3(a) on or with the

transferor's tax return for the tax year of the exchange. The

transferee corporation must include the statement required by

Regulations section 1.351-3(b) on or with its return for the tax

year of the exchange, unless all the required information is

included in any statement(s) provided by a significant transferor

that is attached to the same return for the same section 351

exchange.

Election to reduce basis under section 362(e)(2)(C).

If

property is transferred to a corporation subject to section 362(e)

(2), the transferor and the acquiring corporation may elect, under

section 362(e)(2)(C), to reduce the transferor's basis in the stock

received instead of reducing the acquiring corporation's basis in

the property transferred. Once made, the election is irrevocable.

For more information, see section 362(e)(2) and Regulations

section 1.362-4. If an election is made, a statement must be filed

in accordance with Regulations section 1.362-4(d)(3).

Regulations section 1.1411-10(g) (section 1411 election

with respect to CFCs and QEFs). A corporation that directly

or indirectly owns stock of a controlled foreign corporation (CFC)

(within the meaning of section 953(c)(1)(B) or section 957(a)) or

a passive foreign investment company (within the meaning of

section 1297(a)) that the corporation treats as a qualified

electing fund (QEF) under section 1293 may make the election

provided in Regulations section 1.1411-10(g). The election must

be made no later than the first tax year beginning after 2013

during which the corporation (i) includes an amount in gross

income for chapter 1 purposes under section 951(a) or section

1293(a) for the CFC or QEF, and (ii) has a direct or indirect

owner that is subject to tax under section 1411 or would have

been if the election were made. This election must be made on

an entity-by-entity basis, and applies only to the particular CFCs

and QEFs for which an election is made. In general, for purposes

of section 1411, if an election is in effect for a CFC or QEF, the

amounts included in income under section 951 and section 1293

derived from the CFC or QEF are included in net investment

income, and distributions described in section 959(d) or section

1293(c) are excluded from net investment income. Additionally, if

the corporation elected to be treated as owning stock of a foreign

corporation within the meaning of section 958(a) under

Proposed Regulations section 1.958-1(e)(2), and an election

under Regulations section 1.1411-10(g) is in effect for a CFC,

the amount of global intangible low-taxed income included in

income under section 951A is included in net investment income

to the extent that it is allocated to the CFC under section 951A(f)

(2). An election that is made under Regulations section

1.1411-10(g) can't be revoked. For more information regarding

this election, see Regulations section 1.1411-10(g).

The election must be made in a statement that is filed with the

corporation's original or amended return for the tax year in which

the election is made. An election can be made on an amended

return only if the tax year for which the election is made, and all

tax years affected by the election, aren't closed by the period of

limitations on assessments under section 6501. The statement

must include:

•

The name and EIN of the corporation making the election;

•

A declaration that all of its shareholders consent to each

election made in the statement;

•

A declaration that the corporation elects under Regulations

section 1.1411-10(g) to apply the rules in Regulations section

1.1411-10(g) to the CFCs and QEFs identified in the statement;

and

•

The following information for each CFC and QEF for which an

election is made (i) the name of the CFC or QEF; and (ii) either

the EIN of the CFC or QEF, or, if the CFC or QEF doesn't have an

EIN, the reference ID number of the CFC or QEF.

In addition, for each CFC or QEF held by the corporation for

which an election under Regulations section 1.1411-10(g) has

already been made by the corporation, the statement should

include (i) the name of the CFC or QEF; and (ii) either the EIN of

the CFC or QEF, or, if the CFC or QEF doesn't have an EIN, the

reference ID number of the CFC or QEF.

Annual information reporting by specified domestic enti-

ties under section 6038D. Certain domestic corporations that

are formed or availed of to hold specified foreign financial assets

(“specified domestic entities”) must file Form 8938, Statement of

Instructions for Form 1120-S (2023)

7

Page 8 of 55 Fileid: … ons/i1120s/2023/a/xml/cycle05/source 10:19 - 17-Jan-2024

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Specified Foreign Financial Assets. Form 8938 must be filed

each year the value of the corporation's specified foreign

financial assets meets or exceeds the reporting threshold. For

more information on domestic corporations that are specified

domestic entities and the types of foreign financial assets that

must be reported, see the Instructions for Form 8938, generally,

and in particular,

Who Must File, Specified Domestic Entity,

Types of Reporting Thresholds, Specified Foreign Financial

Assets, Interests in Specified Foreign Financial Assets, Assets

Not Required To Be Reported, and Exceptions to Reporting.

In addition, a domestic corporation required to file Form 8938

with its Form 1120-S for the tax year should check “Yes” to

Schedule N (Form 1120), question 8, and also include that

schedule with its Form 1120-S.

Certification as a qualified opportunity fund. If the

corporation is organized to invest in qualified opportunity zone

property, it must attach Form 8996 to Form 1120-S to self-certify

as a QOF. In addition, the corporation files Form 8996 annually

to report that the QOF meets the investment standard of section

1400Z-2 or to figure the penalty if it fails to meet the investment

standard. The corporation must also complete line 15 of

Schedule B. For more information, see the Instructions for Form

8996.

Qualified opportunity fund investment. If the corporation

deferred a capital gain in a qualified opportunity fund (QOF), the

corporation must file its return with Schedule D (Form 1120-S),

Form 8949, and Form 8997 attached. The corporation will need

to file Form 8997 annually until it disposes of the investment. See

the instructions for Form 8997 for details.

Form 8975, Country-by-Country Report. Certain U.S.

persons that are the ultimate parent entity of a U.S. multinational

enterprise group with annual revenue for the preceding reporting

period of $850 million or more are required to file Form 8975. For

more information, see the Instructions for Form 8975.

Other forms and statements. See Pub. 542, Corporations, for

a list of other forms and statements a corporation may need to

file in addition to the forms and statements discussed throughout

these instructions.

At-Risk Limitations

In general, section 465 limits the amount of deductible net losses

shareholders can claim from certain activities. The at-risk

limitations don't apply to the corporation, but instead apply to

each shareholder's share of net losses attributable to each

activity. Because the treatment of each shareholder's share of

corporate net losses depends on the nature of the activity that

generated it, the corporation must report the items of income,

loss, and deduction separately for each activity. See Pub. 925,

Passive Activity and At-Risk Rules, for additional information.

Activities Covered by the At-Risk Rules

If the S corporation is involved in one of the following activities as

a trade or business or for the production of income, the

shareholder may be subject to the at-risk rules.

1. Holding, producing, or distributing motion picture films or

video tapes.

2. Farming.

3. Leasing section 1245 property, including personal

property and certain other tangible property that is depreciable

or amortizable.

4. Exploring for, or exploiting, oil and gas.

5. Exploring for, or exploiting, geothermal deposits (for wells

started after September 1978).

6. Any other activity not included in (1) through (5) that is

carried on as a trade or business or for the production of income.

Aggregation of Activities

Activities described in (6) under Activities Covered by the At-Risk

Rules, earlier, that constitute a trade or business are treated as

one activity if:

•

You actively participate in the management of the trade or

business, or

•

The trade or business is carried on by a partnership or S

corporation and 65% or more of its losses for the tax year are

allocable to persons who actively participate in the management

of the trade or business.

Similar rules apply to activities described in (1) through (5) of

that earlier discussion. For more information, see Pub. 925. If

you aggregate your activities under these rules for section 465

purposes, check the appropriate box in item J.

At-Risk Activity Reporting Requirements

If the corporate items of income, loss, or deduction reported on

Schedule K-1 are from more than one activity covered by the

at-risk rules, the corporation must report information separately

for each activity.

The following information must be provided on an attachment

to Schedule K-1 for each activity.

•

A statement that the information is a breakdown of the items

of income, loss, or deduction by at-risk activity.

•

The identity of the at-risk activity; the items of income, loss, or

deduction for the activity; other items of income, loss, or

deduction; and any other information that relates to the activity

(that is, distributions, shareholder loans, etc.).

Passive Activity Limitations

In general, section 469 limits the amount of losses, deductions,

and credits that shareholders can claim from “passive activities.”

The passive activity limitations don't apply to the corporation.

Instead, they apply to each shareholder's share of any income or

loss and credit attributable to a passive activity. Because the

treatment of each shareholder's share of corporate income or

loss and credit depends on the nature of the activity that

generated it, the corporation must report income or loss and

credits separately for each activity.

The following instructions and the instructions for Schedules

K and K-1, later, explain the applicable passive activity limitation

rules and specify the type of information the corporation must

provide to its shareholders for each activity. If the corporation

had more than one activity, it must report information for each

activity on an attachment to Schedules K and K-1.

Generally, passive activities include (a) activities that involve

the conduct of a trade or business if the shareholder doesn't

materially participate in the activity, and (b) all rental activities

(defined later) regardless of the shareholder's participation. For

exceptions, see

Activities That Are Not Passive Activities, later.

The level of each shareholder's participation in an activity must

be determined by the shareholder.

The passive activity rules provide that losses and credits from

passive activities can generally be applied only against income

and tax (respectively) from passive activities. Thus, passive

losses can't be applied against income from salaries, wages,

professional fees, or a business in which the shareholder

materially participates or against “portfolio income” (defined

later). Passive credits can't be applied against the tax related to

any of these types of income.

Special rules require that net income from certain activities

that would otherwise be treated as passive income must be

recharacterized as nonpassive income for purposes of the

passive activity limitations. See Recharacterization of Passive

Income, later.

8

Instructions for Form 1120-S (2023)

Page 9 of 55 Fileid: … ons/i1120s/2023/a/xml/cycle05/source 10:19 - 17-Jan-2024

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

To allow each shareholder to correctly apply the passive

activity limitations, the corporation must report income or loss

and credits separately by activity for each of the following.

•

Trade or business activities.

•

Rental real estate activities.

•

Rental activities other than rental real estate.

•

Portfolio income.

Activities That Are Not Passive Activities

The following aren't passive activities.

1. Trade or business activities in which the shareholder

materially participated for the tax year.

2. Any rental real estate activity in which the shareholder

materially participated if the shareholder met both of the

following conditions for the tax year.

a. More than half of the personal services the shareholder

performed in trades or businesses were performed in real

property trades or businesses in which the shareholder

materially participated.

b. The shareholder performed more than 750 hours of

services in real property trades or businesses in which the

shareholder materially participated.

For purposes of this rule, each interest in rental real estate is

a separate activity unless the shareholder elects to treat all

interests in rental real estate as one activity.

If the shareholder is married filing jointly, either the

shareholder or the shareholder’s spouse must separately meet

both of the above conditions, without taking into account

services performed by the other spouse.

A real property trade or business is any real property

development, redevelopment, construction, reconstruction,

acquisition, conversion, rental, operation, management, leasing,

or brokerage trade or business. Services the shareholder

performed as an employee aren't treated as performed in a real

property trade or business unless the shareholder owned more

than 5% of the stock in the employer.

3. The rental of a dwelling unit used by a shareholder for

personal purposes during the year for more than the greater of

14 days or 10% of the number of days that the residence was

rented at fair rental value.

4. An activity of trading personal property for the account of

owners of interests in the activity. For purposes of this rule,

personal property means property that is actively traded, such as

stocks, bonds, and other securities. See Temporary Regulations

section 1.469-1T(e)(6).

The section 469(c)(3) exception for a working interest in

oil and gas properties doesn't apply to an S corporation

because state law generally limits the liability of

shareholders.

Trade or Business Activities

A trade or business activity is an activity (other than a rental

activity or an activity treated as incidental to an activity of holding

property for investment) that:

1. Involves the conduct of a trade or business (within the

meaning of section 162),

2. Is conducted in anticipation of starting a trade or

business, or

3. Involves research or experimental expenditures under

section 174.

If the shareholder doesn't materially participate in the activity,

a trade or business activity of the corporation is a passive activity

for the shareholder.

TIP

Each shareholder must determine if he or she materially

participated in an activity. As a result, while the corporation's

ordinary business income (loss) is reported on page 1 of Form

1120-S, the specific income and deductions from each separate

trade or business activity must be reported on attachments to

Form 1120-S. Similarly, while each shareholder's allocable share

of the corporation's ordinary business income (loss) is reported

in box 1 of Schedule K-1, each shareholder's allocable share of

the income and deductions from each trade or business activity

must be reported on statements attached to each Schedule K-1.

See

Passive Activity Reporting Requirements, later, for more

information.

Rental Activities

Generally, except as noted below, if the gross income from an

activity consists of amounts paid principally for the use of real or

personal tangible property held by the corporation, the activity is

a rental activity.

There are several exceptions to this general rule. Under these

exceptions, an activity involving the use of real or personal

tangible property isn't a rental activity if any of the following

apply.

•

The average period of customer use (defined later) for such

property is 7 days or less.

•

The average period of customer use for such property is 30

days or less and significant personal services (defined later) are

provided by or on behalf of the corporation.

•

Extraordinary personal services (defined later) are provided

by or on behalf of the corporation.

•

The rental of such property is treated as incidental to a

nonrental activity of the corporation under Regulations section

1.469-1(e)(3)(vi).

•

The corporation customarily makes the property available

during defined business hours for nonexclusive use by various

customers.

•

The corporation provides property for use in a nonrental

activity of a partnership in its capacity as an owner of an interest

in such partnership. Whether the corporation provides property

used in an activity of a partnership in the corporation's capacity

as an owner of an interest in the partnership is determined on

the basis of all the facts and circumstances.

In addition, a guaranteed payment described in section

707(c) is never income from a rental activity.

Average period of customer use. Figure the average period

of customer use for a class of property by dividing the total

number of days in all rental periods by the number of rentals

during the tax year. If the activity involves renting more than one

class of property, multiply the average period of customer use of

each class by the ratio of the gross rental income from that class

to the activity's total gross rental income. The activity's average

period of customer use equals the sum of these class-by-class

average periods weighted by gross income. See Regulations

section 1.469-1(e)(3)(iii).

Significant personal services. Personal services include only

services performed by individuals. To determine if personal

services are significant personal services, consider all the

relevant facts and circumstances. Relevant facts and

circumstances include:

•

How often the services are provided,

•

The type and amount of labor required to perform the

services, and

•

The value of the services in relation to the amount charged for

use of the property.

The following services aren't considered in determining

whether personal services are significant.

•

Services necessary to permit the lawful use of the rental

property.

Instructions for Form 1120-S (2023)

9

Page 10 of 55 Fileid: … ons/i1120s/2023/a/xml/cycle05/source 10:19 - 17-Jan-2024

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

•

Services performed in connection with improvements or

repairs to the rental property that extend the useful life of the

property substantially beyond the average rental period.

•

Services provided in connection with the use of any improved

real property that are similar to those commonly provided in

connection with long-term rentals of high-grade commercial or

residential property. Examples include cleaning and

maintenance of common areas, routine repairs, trash collection,

elevator service, and security at entrances.

Extraordinary personal services. Services provided in

connection with making rental property available for customer

use are extraordinary personal services only if the services are

performed by individuals and the customers' use of the rental

property is incidental to their receipt of the services.

For example, a patient's use of a hospital room is generally

incidental to the care received from the hospital's medical staff.

Similarly, a student's use of a dormitory room in a boarding

school is incidental to the personal services provided by the

school's teaching staff.

Rental activity incidental to a nonrental activity. An activity

isn't a rental activity if the rental of the property is incidental to a

nonrental activity, such as the activity of holding property for

investment, a trade or business activity, or the activity of dealing

in property.

Rental of property is incidental to an activity of holding

property for investment if both of the following apply.

•

The main purpose for holding the property is to realize a gain

from the appreciation of the property.

•

The gross rental income from such property for the tax year is

less than 2% of the smaller of the property's unadjusted basis or

its fair market value (FMV).

Rental of property is incidental to a trade or business activity

if all of the following apply.

•

The corporation owns an interest in the trade or business at all

times during the year.

•

The rental property was mainly used in the trade or business

activity during the tax year or during at least 2 of the 5 preceding

tax years.

•

The gross rental income from the property for the tax year is

less than 2% of the smaller of the property's unadjusted basis or

its FMV.

If the corporation sells or exchanges property that is also

rented during the tax year (in which the gain or loss is

recognized), the rental is treated as incidental to the activity of

dealing in property if, at the time of the sale or exchange, the

property was held primarily for sale to customers in the ordinary

course of the corporation's trade or business.

See Temporary Regulations section 1.469-1T(e)(3) and

Regulations section 1.469-1(e)(3) for more information on the

definition of rental activities for purposes of the passive activity

limitations.

Reporting of rental activities. In reporting the corporation's

income or losses and credits from rental activities, the

corporation must separately report rental real estate activities

and rental activities other than rental real estate activities.

Shareholders who actively participate in a rental real estate

activity may be able to deduct part or all of their rental real estate

losses (and the deduction equivalent of rental real estate credits)

against income (or tax) from nonpassive activities. Generally, the

combined amount of rental real estate losses and the deduction

equivalent of rental real estate credits from all sources (including

rental real estate activities not held through the corporation) that

may be claimed is limited to $25,000.

Report rental real estate activity income (loss) on Form 8825

and line 2 of Schedule K and box 2 of Schedule K-1, rather than

on page 1 of Form 1120-S. Report credits related to rental real

estate activities on lines 13c and 13d of Schedule K (box 13,

codes E and F, of Schedule K-1) and low-income housing credits

on lines 13a and 13b of Schedule K (box 13, codes C and D of

Schedule K-1).

Report income (loss) from rental activities other than rental

real estate on line 3 of Schedule K and credits related to rental

activities other than rental real estate on line 13e of Schedule K

and in box 13, code G, of Schedule K-1.

Portfolio Income

Generally, portfolio income includes all gross income, other than

income derived in the ordinary course of a trade or business,

that is attributable to interest; dividends; royalties; income from a

real estate investment trust, a regulated investment company, a

real estate mortgage investment conduit, a common trust fund, a

controlled foreign corporation, a qualified electing fund, or a

cooperative; income from the disposition of property that

produces income of a type defined as portfolio income; and

income from the disposition of property held for investment. See

Self-Charged Interest, later, for an exception.

Solely for purposes of the preceding paragraph, gross

income derived in the ordinary course of a trade or business

includes (and portfolio income, therefore, doesn't include) the

following types of income.

•

Interest income on loans and investments made in the

ordinary course of a trade or business of lending money.

•

Interest on accounts receivable arising from the performance

of services or the sale of property in the ordinary course of a

trade or business of performing such services or selling such

property, but only if credit is customarily offered to customers of

the business.

•

Income from investments made in the ordinary course of a

trade or business of furnishing insurance or annuity contracts or

reinsuring risks underwritten by insurance companies.

•

Income or gain derived in the ordinary course of an activity of

trading or dealing in any property if such activity constitutes a

trade or business (unless the dealer held the property for

investment at any time before such income or gain is

recognized).

•

Royalties derived by the taxpayer in the ordinary course of a

trade or business of licensing intangible property.

•

Amounts included in the gross income of a patron of a

cooperative by reason of any payment or allocation to the patron

based on patronage occurring with respect to a trade or

business of the patron.

•

Other income identified by the IRS as income derived by the

taxpayer in the ordinary course of a trade or business.

See Temporary Regulations section 1.469-2T(c)(3) for more

information on portfolio income.

Report portfolio income and related deductions on

Schedule K rather than on page 1 of Form 1120-S.

Self-Charged Interest

Certain self-charged interest income and deductions may be

treated as passive activity gross income and passive activity

deductions if the loan proceeds are used in a passive activity.

Generally, self-charged interest income and deductions result

from loans between the corporation and its shareholders.

Self-charged interest also occurs in loans between the

corporation and another S corporation or partnership if each

owner in the borrowing entity has the same proportional

ownership interest in the lending entity.

The self-charged interest rules don't apply to a shareholder's

interest in an S corporation if the S corporation makes an

election under Regulations section 1.469-7(g) to avoid the

application of these rules. To make the election, the S

corporation must attach to its original or amended Form 1120-S

10

Instructions for Form 1120-S (2023)

Page 11 of 55 Fileid: … ons/i1120s/2023/a/xml/cycle05/source 10:19 - 17-Jan-2024

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

a statement that includes the name, address, EIN of the S

corporation, and a declaration that the election is being made

under Regulations section 1.469-7(g). The election will apply to

the tax year for which it was made and all subsequent tax years.

Once made, the election can only be revoked with the consent of

the IRS.

For more details on the self-charged interest rules, see

Regulations section 1.469-7.

Grouping Activities

Generally, one or more trade or business or rental activities may

be treated as a single activity if the activities make up an

appropriate economic unit for measurement of gain or loss under

the passive activity rules. Whether activities make up an

appropriate economic unit depends on all the relevant facts and

circumstances. The factors given the greatest weight in

determining whether activities make up an appropriate economic

unit are:

•

Similarities and differences in types of trades or businesses,

•

The extent of common control,

•

The extent of common ownership,

•

Geographical location, and

•

Reliance between or among the activities.

Example. The corporation has a significant ownership

interest in a bakery and a movie theater in Baltimore and a

bakery and a movie theater in Philadelphia. Depending on the

relevant facts and circumstances, there may be more than one

reasonable method for grouping the corporation's activities. For

instance, the following groupings may or may not be permissible.

•

A single activity.

•

A movie theater activity and a bakery activity.

•

A Baltimore activity and a Philadelphia activity.

•

Four separate activities.

Once the corporation chooses a grouping under these rules,

it must continue using that grouping in later tax years unless

either:

•

The corporation determines that the original grouping was

clearly inappropriate, or

•

A material change in the facts and circumstances makes that

grouping clearly inappropriate.

The IRS may regroup the corporation's activities if the

corporation's grouping isn't an appropriate economic unit and

one of the primary purposes for the grouping (or failure to

regroup as required under Regulations section 1.469-4(e)) is to

avoid the passive activity limitations. If you group your activities

under these rules for section 469 purposes, check the

appropriate box in item J.

Limitation on grouping certain activities. The following

activities may not be grouped together.

1. A rental activity with a trade or business activity unless

the activities being grouped together make up an appropriate

economic unit and:

a. The rental activity is insubstantial relative to the trade or

business activity or vice versa; or

b. Each owner of the trade or business activity has the same

proportionate ownership interest in the rental activity. If so, the

portion of the rental activity involving the rental of property to be

used in the trade or business activity can be grouped with the

trade or business activity.

2. An activity involving the rental of real property with an

activity involving the rental of personal property (except personal

property provided in connection with the real property or vice

versa).

3. Any activity with another activity in a different type of

business and in which the corporation holds an interest as a

limited partner or as a limited entrepreneur (as defined in section

461(k)(4)) if that other activity is holding, producing, or

distributing motion picture films or videotapes; farming; leasing

section 1245 property; or exploring for or exploiting oil and gas

resources or geothermal deposits.

Activities conducted through partnerships. Once a