Applying IFRS for the real estate industry

PwC Contents

Introduction to applying IFRS for the real estate industry 1

1. Real estate value chain 2

1.1. Overview of the investment property industry 2

1.2. Real estate life cycle 2

1.3. Relevant accounting standards 3

2. Acquisition and construction of real estate 5

2.1. Overview 5

2.2. Definition and classification 5

2.3. Acquisition of investment properties: asset acquisition or business

combination 9

2.4. Asset acquisitions: Measurement at initial recognition 15

2.5. Accounting for forward contracts and options to acquire real estate 18

2.6. Special considerations: investment properties under construction 20

2.7. Accounting for rental guarantees 21

2.8. Development properties: accounting for the costs of construction 23

3. Subsequent measurement of investment property 27

3.1. Costs incurred after initial recognition 27

3.2. Replacement of parts of investment property and subsequent expenditure 28

3.3. Subsequent measurement: Cost model 29

3.4. Impairment 32

3.5. Subsequent measurement: Fair value model 36

3.6. Fair value measurement of investment property: IFRS 13 38

3.7. Change in use of assets: transfers into and out of investment property 45

4. Rental income: accounting by lessors 49

4.1. Overview of guidance 49

4.2. Definition of a lease 49

4.3. Rental income: Lessor accounting 50

4.4. Premiums for properties in a prime location 56

4.5. Surrender premiums 56

4.6. Assumption of potential tenant’s existing lease 57

4.7. Key money 58

4.8. Letting fees 58

4.9. Tenant deposits received 59

4.10. Revenue from managing real estate property 60

4.11. Lease modifications 64

4.12. Revenue recognition: Surrender premium/break costs 65

4.13. Tenant obligations to restore a property’s condition 65

5. Real estate structures and tax considerations 66

Contents

Applying IFRS for the real estate industry

PwC Contents

5.1. Consolidation 66

5.2. Joint arrangements 72

5.3. Taxation 76

6. Disposal of investment property 83

6.1. Classification as held for sale under IFRS 5 83

6.2. Sale of investment property 83

7. Other reporting issues 86

7.1. Functional and presentation currency 86

7.2. Cash flow statement 88

8. Disclosures 91

8.1. Segment disclosures 91

8.2. IFRS 13 disclosures 96

8.3. Disclosure of fair value for properties accounted for using the cost model 97

Applying IFRS for the real estate industry

PwC 1

What is the focus of this publication?

This publication considers the main accounting issues encountered by real estate entities and the practices

adopted in the industry under International Financial Reporting Standards (IFRS).

Who should use this publication?

This publication is intended for real estate entities that construct and manage real estate property. Activities

such as the construction of properties on behalf of third parties, and holding or developing properties

principally for sale or otherwise own use, are not considered in this publication.

This publication is intended for:

audit committees, executives and financial managers in the real estate industry;

investors and other users of real estate industry financial statements, so they can identify some of the

accounting practices adopted to reflect features unique to the industry; and

accounting bodies, standard-setting agencies and governments throughout the world that are interested in

accounting and reporting practices and responsible for establishing financial reporting requirements.

What is included?

This publication covers issues that we believe are of financial reporting interest due to their particular relevance

to real estate entities and/or historical varying international practice.

This publication has a number of sections designed to cover the main issues raised.

This publication is based on the experience gained from the worldwide leadership position of PwC in the

provision of services to the real estate industry. This leadership enables PwC’s Real Estate Industry Group to

make recommendations and lead discussions on international standards and practice.

We hope you find this publication helpful.

Introduction to applying IFRS

for the real estate industry

Applying IFRS for the real estate industry

PwC 2

1.1. Overview of the investment property industry

The investment property or real estate industry comprises entities that hold real estate (land and buildings) to

earn rentals and/or for capital appreciation.

Real estate properties are usually held through a variety of structures that include listed and privately held

corporations, investment funds, partnerships and trusts.

1.2. Real estate life cycle

The life cycle of real estate that is accounted for as investment property typically includes the following stages:

Acquisition and

construction of

real estate

Leasing or

subleasing of

real estate

Management

of real estate

Sale or

demolition of

real estate

1

2

3

4

Step 1: Acquisition and construction of real estate

Control of real estate can be obtained through:

direct acquisition of real estate;

construction of real estate; or

leasing of real estate, under either operating or finance leases.

Entities normally perform strategic planning before the acquisition, construction or leasing, to assess the

feasibility of the project.

Entities might incur costs attributable to the acquisition, construction or leasing of real estate, during this first

step of the cycle. Entities might also enter into financing arrangements to secure the liquidity required for the

acquisition and construction of real estate.

Step 2: Leasing or subleasing of real estate

Most real estate entities primarily hold real estate for own use or for the purpose of earning rentals.

For entities holding real estate for the purpose of earning rentals, lease agreements might contain a variety of

terms. The most common terms that will feature in all leases include matters such as the agreed lease term (and

any options to extend that term), as well as the agreed rental payments due. Additional items that might feature

include payments for maintenance services, insurance, property taxes and terms of lease incentives provided to

the tenant.

Step 3: Management of real estate

Real estate entities often provide management services to tenants who occupy the real estate that they hold, to

ensure that the property is in good condition and to preserve the value of the real estate. These services might be

performed by the real estate owners themselves, or they might be outsourced to other entities that are designed to

provide these services. Services might include maintenance of common areas, cleaning and security.

Step 4: Sale or demolition of real estate

Real estate entities might sell the real estate that they hold at the end of the life cycle to benefit from capital

appreciation. Alternatively, entities might proceed with demolition of the property, potentially with a view to

construction of a new property.

1. Real estate value chain

Applying IFRS for the real estate industry

PwC 3

1.3. Relevant accounting standards

Acquisition and construction of real estate that is accounted for as investment property is governed by the

requirements of IAS 40, ‘Investment property’, IAS 16, ‘Property, plant and equipment’, and IAS 23,

‘Borrowing costs’.

The requirements of IAS 17, ‘Leases’, apply when an entity leases out the real estate property or an entity does

not elect to classify its property interest under an operating lease as investment property. The requirements of

IAS 18, ‘Revenue’, apply for revenue generated by a real estate entity other than lease income.

This publication is based on accounting standards that are effective for periods beginning on or after

1 January 2017.

There are a number of new standards, interpretations or amendments to existing standards issued as of the

date of this publication that are not yet effective. Their impact is presented in separate sections under each

relevant area or otherwise referred to specifically in the guide. The standards, interpretations or amendments

are as follows:

IFRS 9, ‘Financial Instruments’, which replaces guidance of IAS 39 on classification and measurement of

financial instruments (‘IFRS 9’);

IFRS 15, ‘Revenue from contracts with customers’, which replaces the guidance in IAS 18, IAS 11, IFRIC 13,

IFRIC 15, IFRIC 18 and SIC 31 (‘IFRS 15’);

IFRS 16, ‘Leases’, which replaces IAS 17, IFRIC 4, SIC 15 and SIC 27 (‘IFRS 16’);

‘Transfers of investment property’ amendments to IAS 40, ‘Investment Property’;

IFRIC 22, ‘Foreign currency transactions and advance consideration’ (‘IFRIC 22’); and

IFRIC 23, ‘Uncertainty over income tax treatments’ (‘IFRIC 23’).

The following standards, effective as at the date of this publication, are referred to in the guide:

IFRS 3, ‘Business combinations’ (‘IFRS 3’);

IFRS 5, ‘Non-current assets held for sale and discontinued operations’ (‘IFRS 5’);

IFRS 7, ‘Financial instruments: disclosures’ (‘IFRS 7’);

IFRS 8, ‘Operating segments’ (‘IFRS 8’);

IFRS 10, ‘Consolidated financial statements’ (‘IFRS 10’);

IFRS 11, ‘Joint arrangements’ (‘IFRS 11’);

IFRS 13, ‘Fair value measurement’ (‘IFRS 13’);

IAS 1, ‘Presentation of financial statements’ (‘IAS 1’);

IAS 2, ‘Inventories’ (‘IAS 2’);

IAS 7, ‘Statement of cash flows’ (‘IAS 7’);

IAS 8, ‘Accounting policies, changes in accounting estimates and errors’ (‘IAS 8’);

IAS 11, ‘Construction contracts’ (‘IAS 11’);

IAS 12, ‘Income taxes’ (‘IAS 12’);

IAS 16, ‘Property, plant and equipment’ (‘IAS 16’);

IAS 17, ‘Leases’ (‘IAS 17’);

IAS 18, ‘Revenue’ (‘IAS 18’);

IAS 21, ‘The effects of changes in foreign exchange rates’ (‘IAS 21’);

IAS 23, ‘Borrowing costs’ (‘IAS 23’);

Applying IFRS for the real estate industry

PwC 4

IAS 27, ‘Separate financial statements’ (‘IAS 27’);

IAS 28, ‘Investments in associates and joint ventures’ (‘IAS 28’);

IAS 36, ‘Impairment of assets’ (‘IAS 36’);

IAS 37, ‘Provisions, contingent liabilities and contingent assets’ (‘IAS 37’);

IAS 38, ‘Intangible assets’ (‘IAS 38’);

IAS 39, ‘Financial instruments: recognition and measurement’ (‘IAS 39’);

IAS 40, ‘Investment property’ (‘IAS 40’);

IFRIC 4, ‘Determining whether an arrangement contains a lease’ (‘IFRIC 4’);

IFRIC 13, ‘Customer loyalty programmes’ (‘IFRIC 13’);

IFRIC 15, ‘Agreements for construction of real estate’ (‘IFRIC 15’);

IFRIC 18, ‘Transfers of assets to customers’ (‘IFRIC 18’);

SIC 27, ‘Evaluating the substance of transactions involving the legal form of a lease’ (‘SIC 27’); and

SIC 31, ‘Revenue – barter transactions involving advertising services’ (‘SIC 31’).

Applying IFRS for the real estate industry

PwC 5

2.1. Overview

Real estate entities obtain real estate either by acquiring, constructing or leasing property. Property used for the

purpose of earning rentals is classified as investment property under IAS 40.

2.2. Definition and classification

Principles

IAS 40 defines investment property as property that is held to earn rentals or capital appreciation or both.

[IAS 40 para 5]. The property might be land or a building (part of a building) or both.

Investment property does not include:

Property intended for sale in the ordinary course of business or for development and resale.

Owner-occupied property, including property held for such use or for redevelopment prior to such use.

Property occupied by employees.

Owner-occupied property awaiting disposal.

Property that is leased to another entity under a finance lease.

[IAS 40 para 9].

Owner-occupied property is property that is used in the production or supply of goods or services or for

administrative purposes. [IAS 40 para 5]. A factory or the corporate headquarters of an entity would qualify as

owner-occupied property. During the life cycle of a property, real estate entities might choose to redevelop

property for the purposes of onward sale. Property held for sale in the ordinary course of business is classified

as inventory rather than investment property. [IAS 40 para 9(a)]. Transfers between investment property and

both owner-occupied property and inventory are dealt with in section 3.7.

Classification as investment property is not always straightforward. Factors to consider, when determining the

classification of a property, include but are not limited to:

the extent of ancillary services provided (see section 2.2.2);

the extent of use of the property in running an underlying business;

whether the property has dual use (see section 2.2.6);

the strategic plans of the entity for the property; and

previous use of the property.

2. Acquisition and construction

of real estate

Applying IFRS for the real estate industry

PwC 6

Example – Property leased out to hotel management entity

Background

Entity A owns property which it leases out under an operating lease to a hotel management entity. Entity A

has no involvement in the running of the hotel or any decisions made; these decisions are all undertaken by

the hotel management entity.

Does the property meet the definition of ‘investment property’ for entity A?

Solution

Yes. Although the property is used as a hotel by the lessee, entity A uses the property to earn rentals, and so

the property meets the definition of ‘investment property’.

Where an entity decides to dispose of an investment property without development, it continues to treat the

property as an investment property. [IAS 40 para 58]. The property will continue to be classified as investment

property until it meets the criteria to be classified as a non-current asset held for sale in accordance with IFRS 5

(see section 6).

Ancillary services

Where an entity provides insignificant ancillary services, such as maintenance, to the third party occupants of

the property, this does not affect the classification of the property as an investment property. [IAS 40 para 11].

Where ancillary services provided are more than insignificant, the property is regarded as owner-occupied,

because it is being used to a significant extent for the supply of goods and services. For example, in a hotel,

significant ancillary services such as a restaurant, fitness facilities or spa are often provided. IAS 40 provides no

application guidance as to what ‘insignificant’ means. Accordingly, entities should consider both qualitative and

quantitative factors in determining whether services are insignificant.

Example – Serviced apartments

Background

An entity owns a number of apartments which it leases out to tenants under short-term leases. The entity is

also responsible for providing in-house cleaning services, and it undertakes to provide internet, telephone

and cable television to the tenants for an additional monthly fee. The additional fee charged for the services is

approximately 20% of the monthly rental.

Does the property meet the definition of ‘investment property’?

Solution

No. The entity provides ancillary services to the tenants other than the right to use the property. The value of

these services represents around 20% of the rental income. Therefore, these services cannot be viewed as

insignificant. The property is classified as property, plant and equipment in the financial statements of

the entity.

Properties under construction or development

Real estate that meets the definition of ‘investment property’ is accounted for in accordance with IAS 40, even

during the period when it is under construction. Further, an investment property under redevelopment for

continued future use as investment property also continues to be recognised as investment property.

Properties held to be leased out as investment property

Real estate entities might hold investment properties that are vacant for a period of time. Where these

properties are held to be leased out under an operating lease, they are classified as investment property.

Applying IFRS for the real estate industry

PwC 7

Properties with undetermined use

Land with undetermined use is accounted for as investment property. This is due to the fact that an entity’s

decision around how it might use that land (be it as an investment property, inventory or as owner-occupied

property) is, of itself, an investment decision. In turn, the most appropriate classification for such property is as

investment property. [IAS 40 para B67 (b) (ii)].

Properties with dual use

A property might be partially owner-occupied, with the rest being held for rental income or capital appreciation.

If each of these portions can be sold separately (or separately leased out under a finance lease), the entity

should account for the portions separately. [IAS 40 para 10]. That is, the portion that is owner-occupied is

accounted for under IAS 16, and the portion that is held for rental income or capital appreciation, or both, is

treated as investment property under IAS 40.

If the portions cannot be sold or leased out separately under a finance lease, the property is investment property

only if an insignificant portion is owner-occupied, in which case the entire property is accounted for as

investment property. If more than an insignificant portion is owner-occupied, the entire property is accounted

for as property, plant and equipment. There is no guidance under the standards as to what ‘insignificant’

means; accordingly, entities should consider both qualitative and quantitative factors in determining whether

the portion of the property is insignificant.

Example – Hotel resort with a casino

Background

Entity A owns a hotel resort which includes a casino, housed in a separate building.

The entity operates the hotel and other facilities on the hotel resort, with the exception of the casino, which

can be sold or leased out under a finance lease. The casino is leased to an independent operator. Entity A has

no further involvement in the casino. The casino operator will only operate the casino with the existence of

the hotel and other facilities.

Does the casino meet the definition of ‘investment property’?

Solution

Yes. Management should classify the casino as investment property. The casino can be sold separately or

leased out under a finance lease. The hotel and other facilities would be classified as property, plant and

equipment.

If the casino could not be sold or leased out separately on a finance lease, the whole property would be

treated as property, plant and equipment.

Group situations

Within a group of entities, one group entity might lease property to another group entity for its occupation and

use. In the consolidated financial statements, such property is not treated as investment property, because from

the group's point of view the property is owner-occupied. In the separate financial statements of the entity that

owns the property or holds it under a finance lease, the property will be treated as investment property if it

meets the definition. [IAS 40 para 15].

In contrast, property owned or held under a finance lease by a group entity and leased to an associate or a joint

venture should be accounted for as investment property in both the consolidated financial statements and any

separate financial statements prepared. Associates and joint ventures are not considered part of the group for

consolidation purposes.

Applying IFRS for the real estate industry

PwC 8

Properties held under operating leases

An entity might choose to treat a property interest that is held by a lessee under an operating lease as an

investment property if:

the rest of the definition of investment property is met (see section 2.2); and

the lessee uses the fair value model in IAS 40 (see section 3.5).

This choice is available on a property-by-property basis. The initial cost of a property interest held under an

operating lease and classified as an investment property is as prescribed for a finance lease (that is, an asset

should be recognised at the lower of the fair value of the property and the present value of the minimum lease

payments). [IAS 40 para 25].

Impact of IFRS 16

IFRS 16 brings almost all leases on the balance sheet of the lessee. The lessee recognises a right-of-use asset and

a corresponding liability at the lease commencement date. [IFRS 16 para 22].

As a result, under IFRS 16, property currently held under operating leases will be recognised on the balance

sheet. If this property meets the definition of investment property, it is initially recognised in accordance with

IFRS 16, and it is subsequently accounted for as investment property in accordance with IAS 40.

The right-of-use asset might subsequently be carried at cost or fair value, depending on the accounting policy of

the entity for investment properties.

Example – Recognition of property held under an operating lease as investment property

Background

An entity owns a hotel that it leases out (as lessor) under an operating lease to a hotel management group.

The hotel is situated on land leased by the government to the entity (as lessee) for a period of 99 years, with

no transfer of title to the entity at the end of the lease. The hotel building’s useful life is expected to be

approximately 40 years. There are no provisions in the lease to return the land with the building intact at the

end of the 99-year lease. At inception of the lease, the present value of the minimum lease payments is

significantly lower than the fair value of the land. On considering the lease classification guidance in IAS 17,

it has been determined that the land lease meets the definition of an ‘operating lease’.

Can the hotel be classified as investment property?

Solution

Building:

Yes. The building meets the definition of ‘investment property’ and should be accounted for under IAS 40.

Land:

The land meets the definition of ‘investment property’ and is recognised on the balance sheet as an

investment property only if the entity has chosen the fair value model for investment property. [IAS

40 para 6]. Otherwise, it is recognised and accounted for as operating lease under IAS 17.

Impact of IFRS 16

Under IFRS 16, the entity will need to recognise a right-of-use asset relating to the leased land.

The right-of-use asset relating to the leased land should be accounted for as investment property, given that

it meets the definition. The policy that the entity applies for subsequent measurement of investment property

will not affect the classification of the land as investment property.

Applying IFRS for the real estate industry

PwC 9

2.3. Acquisition of investment properties: asset acquisition or

business combination

Entities might acquire investment properties that meet the definition of an asset or investment properties,

together with processes and outputs that meet the definition of a business under IFRS 3.

It is also common in the real estate industry to structure property acquisitions and disposals in a tax-efficient

manner. This often involves the transfer of a company, frequently referred to as a ‘corporate wrapper’, which

holds one or more properties.

The accounting treatment for an acquisition depends on whether it is a business combination or an asset

acquisition.

A ‘business’ is defined as an “integrated set of activities and assets that is capable of being conducted and

managed for the purpose of providing a return in the form of dividends, lower costs or other economic

benefits directly to investors or other owners, members or participants”. [IFRS 3 App A].

The legal form of the acquisition is not a determining factor when assessing whether a transaction is a business

combination or an asset acquisition. For example, the acquisition of a single vacant investment property is not a

business combination simply because it is effected using a corporate wrapper. Similarly, a transaction is not an

asset acquisition simply because the acquiring entity purchases a series of assets rather than a company.

A transaction will qualify as a business combination only where the assets purchased constitute a business.

Significant judgement is required in the determination of whether the definition of a business is met.

A business is a group of assets that includes inputs, outputs and processes that are capable of being managed

together for providing a return to investors or other economic benefits. Not all of the elements need to be

present for the group of assets to be considered a business:

Outputs are not required for an integrated set to qualify as a business. [IFRS 3 para B10].

A business need not include all of the inputs or processes that the seller used in operating that business if

market participants are capable of acquiring the business and continuing to produce outputs (for example,

by integrating the business with their own inputs and processes). [IFRS 3 para B8].

Different properties might fall on a spectrum ranging from asset acquisition to business combination,

depending on the facts and circumstances involved in the transaction. At one end of the spectrum is the

acquisition of a vacant parcel of land; at the other end is the acquisition of a full service, fully operational

shopping mall.

The purchase of a vacant parcel of land is typically viewed as an asset acquisition, because the land itself is an

input, but there are no significant processes in place. The acquisition of the full service shopping mall is

typically viewed as a business combination, because the shopping mall has inputs (the building), processes (the

strategic management, employees and procedures currently operating) and outputs (store rentals).

All other acquisitions fall somewhere in between these two on the spectrum. There is no bright line that

indicates whether the acquisition is that of a business or an asset. Each acquisition will be unique, and the facts

and circumstances of each will have to be examined, with significant judgement being required.

Each property type has its own considerations as to how it is operated and managed. In general, the more

actively managed a property is, the more likely it is to be considered a business.

Applying IFRS for the real estate industry

PwC 10

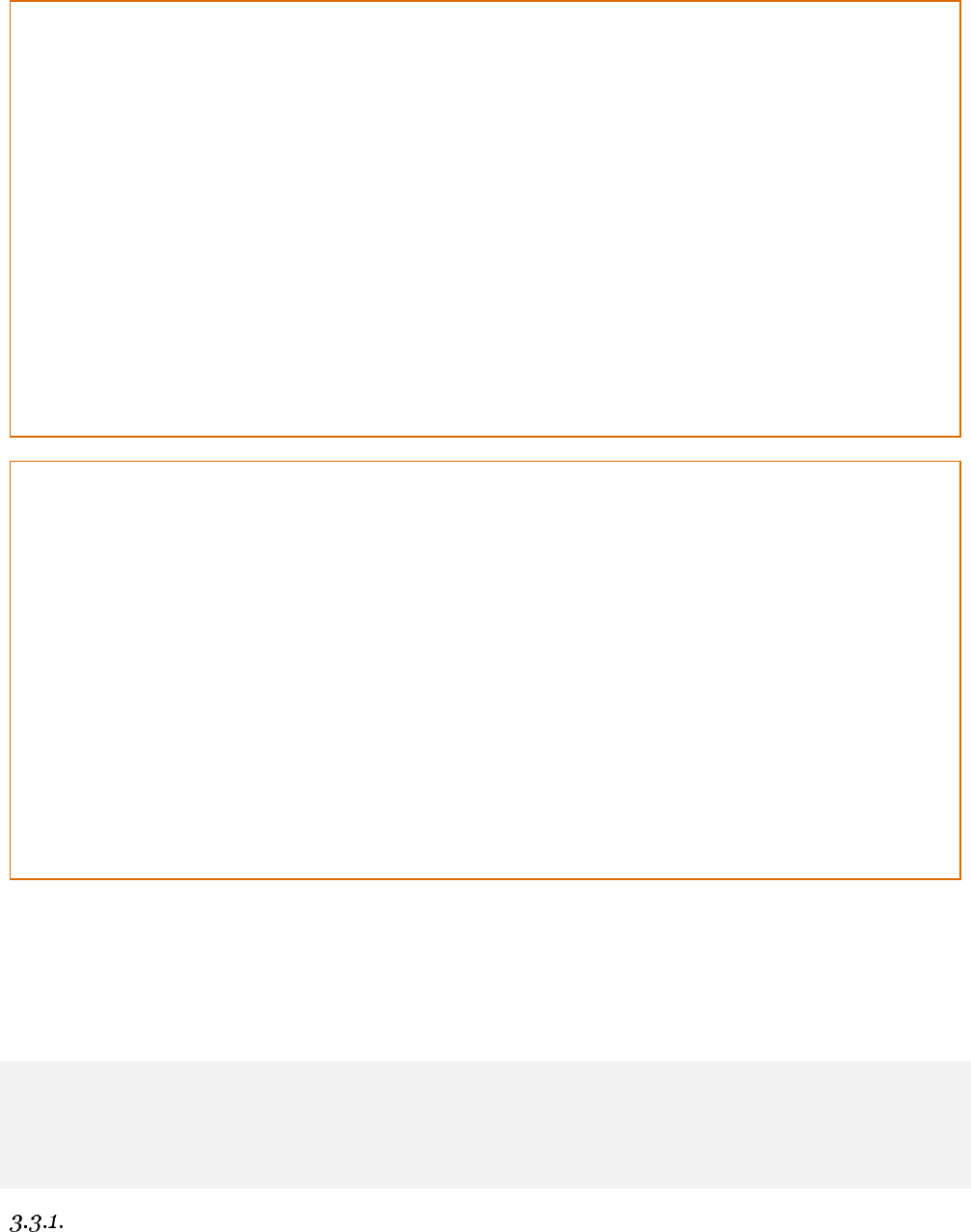

The following diagram summarises the requirements of IFRS 3:

Step 1: Identify

the element of

the acquired

group

Step 2: Assess

capability of the

group to produce

outputs

Step 3: Assess

market participant’s

ability to produce

outputs

Input:

What did the acquirer buy?

Output:

What did the acquirer get, and want to

get, out of this acquisition?

Process:

Are there any existing processes

transferred to produce the output?

What are the missing inputs and/or

processes to produce/achieve the

outputs?

Are market participants capable of

continuing to produce outputs?

Business Assets

Business Assets

Process: are there any inherent

processes attached to the inputs?

Are there sufficient inputs and

processes to produce outputs?

Yes

Yes

Yes

No

NoNo

Yes

No

Inputs and outputs alone (for example, the acquisition of a single-tenant property) would not lead to a business

combination. Furthermore, if the ‘processes’ are insignificant to the arrangement as a whole, this should not in

isolation cause the transaction to be a business combination (for example, the provision of a caretaker who is

responsible for security and basic maintenance).

An example of acquisition of significant processes would be the acquisition of the management team of a

shopping mall which is responsible for strategy around tenant mix, tenant selection, rent reviews, management

of communal areas and marketing of the centre to shoppers. This sort of strategic management would suggest

that the transaction is a business combination rather than an asset acquisition.

The table below sets out the types of process that can be viewed as purely administrative and those that are

more strategic and might indicate that a business has been acquired. The items in the table are not an

exhaustive list of factors, and the facts and circumstances of each transaction must be carefully assessed on a

case-by-case basis.

Applying IFRS for the real estate industry

PwC 11

Indicators of business combinations

Not necessarily indicators of business combination

on their own

Substantive processes and/or services acquired/provided:

Administrative processes and/or ancillary services

acquired/provided:

Lease management (rent reviews, negotiation of terms)

Security

Management of common areas to promote increased

footfall (for example, themed evenings, marketing)

Cleaning

Selection of tenants

Rent collection/invoicing

Investment decisions

Caretaker

Marketing decisions

The criteria set out above could be applied to the acquisition of more than one investment property.

For example, if the acquirer acquired one property, or a small number of properties, from a seller’s asset

portfolio which is managed centrally, the acquirer is unlikely to have acquired the benefit of the seller’s strategic

activities, and so the acquisition is unlikely to be viewed as a business combination. However, if the acquirer

buys almost all of the portfolio, including the portfolio management, the acquirer will be getting the benefit of

the seller’s portfolio management, which is indicative of a business combination.

It is necessary to look at what has been acquired, rather than the acquirer’s subsequent intentions. An entity

might buy a business solely for the assets within that business, with the intention of disregarding the processes

and management within that business. The intention to disregard the acquired processes does not mean that

the acquisition should not be treated as a business combination.

Impact of proposed amendment to IFRS 3

The requirements of IFRS 3 in relation to whether a transaction meets the definition of a business combination

are currently under review. The IASB has issued an exposure draft that proposes clarifications to the definition

of a business, as well as additional illustrative examples, including those relevant to the real estate industry.

A significant change in the proposed amendment is the requirement for an entity to assess whether

substantially all of the fair value of the gross assets acquired is concentrated in a single asset or group of similar

assets. If such a concentration exists, the transaction is not viewed as an acquisition of a business.

In the context of real estate, this will be relevant where the value of the acquired entity is concentrated in one

property, or a group of similar properties.

Example – Acquisition of a group of commercial office properties 1

Background

Entity W owns and manages a group of commercial real estate investment properties. It purchases a

commercial office property in a large city. The purchased property is 90% occupied, and entity W will

become a party to the lease agreements on acquisition. Entity W will replace existing security, cleaning and

maintenance contracts with new contracts. In addition, the existing property management agreement will be

terminated, and entity W will undertake all property management functions, such as collecting rent and

supervising work. In connection with the transaction, entity W will also hire the current leasing and other key

strategic management personnel involved with the operations of the property.

Is the acquired group a business?

Applying IFRS for the real estate industry

PwC 12

Solution

Yes. It is likely that the acquired group is a business.

Step 1: Identify the elements of the acquired group:

Inputs

Tangible items: commercial property

Intangible items: lease agreements

Other items not necessarily recognised in the financial statements: key

leasing and management personnel

Processes

Strategic management team processes

Personnel with requisite skills and experience

Outputs

The right to receive cash flows in the form of rental income

Potential capital growth in the property

Step 2: Assess the capability of the group to produce outputs

Rental income (that is, an output) is present immediately after the acquisition.

Step 3: Assess the capability of a market participant to produce outputs if missing elements exist

In this case, entity W has acquired all processes and key personnel associated with the property, even though

it subsequently chooses to replace some non-strategic processes with its own. In entity W’s case, it was able

to easily replace the elements that it chose not to take on from the seller. This assessment requires judgement

and is based on facts and circumstances in each situation. In particular, judgement is required in

determining whether any missing elements would prevent the acquired group from being a business.

Example – Acquisition of a group of commercial office properties 2

Background

Entity X is an owner and manager of commercial office towers across the east coast of Australia.

Entity X has purchased a portfolio of commercial properties on Australia’s west coast. Entity X has no

existing operations in this location, and it has limited local market knowledge and experience.

The acquired portfolio of commercial property has 85% occupancy on average, with leases being executed

between the tenants and the property’s freeholder. Entity X becomes a party to these lease agreements on

acquisition of the freehold title to the commercial properties.

Existing security, cleaning and maintenance contracts are novated to entity X on acquisition of the property.

The existing property management agreement will be terminated. Entity X will undertake all property

management functions: tenant management, collection of rent, and supervision of contract work at the

commercial properties.

Entity X will employ a number of the seller’s employees, including the regional leasing managers and other

key strategic management personnel. These employees will be responsible for:

the property’s leasing profile and tenant mix;

capital expenditure on the property (for example, decisions to repair, renovate, redevelop and expand);

additional investment and divestment decisions (for example, to buy or sell additional properties); and

other decisions concerning the strategic positioning of the west coast portfolio.

Applying IFRS for the real estate industry

PwC 13

The acquisition price has been based on an independent valuation of the commercial properties individually,

using discounted net cash flows, and taking into consideration rental returns less cash outflows on property

outgoings, over a 10-year period.

Is the acquired group of assets a business?

Solution

Yes. The acquired portfolio is a business.

Step 1: Identify the elements of the acquired group:

Outputs

Tangible items: the commercial office towers

Intangible items: existing lease agreements with tenants, security, cleaning and

maintenance contracts

Other items not necessarily recognised in the financial statements: management

team, management knowledge of the west coast Australian market and portfolio

Processes

Strategic management team processes

Expertise

Industry knowledge

Outputs

The right to receive cash flows in the form of rental income

Potential capital growth in the property

Step 2: Assess the capability of the group to produce outputs

Entity X has acquired processes in the strategic management of the commercial properties. These processes

will allow entity X to realise the value of the commercial properties and generate outputs, through both rental

returns and future growth in the valuation of the properties.

Step 3: Assess the capability of a market participant to produce outputs if missing elements exist

Entity X acquired inputs and processes that allow the generation of outputs. No further analysis concerning

the capability of a market participant to produce outputs is required.

Example – Acquisition of an empty building

Background

Entity Y has acquired an empty building during the year. The building has no tenants on acquisition. The

building contains no furniture. Entity Y will undertake the day-to-day property management. Entity Y did

not hire any existing employees.

Is the acquired group of assets a business?

Solution

No. The acquired portfolio is not a business.

Step 1: Identify the elements of the acquired group:

Outputs

Tangible items: the building

Intangible items: none

Other items not necessarily recognised in the financial statements: none

Processes

None

Outputs

Access to economic benefits arising from future leases

Applying IFRS for the real estate industry

PwC 14

Step 2: Assess the capability of the group to produce outputs

Processes that allow entity Y to find tenants, run the day-to-day operations and strategically position the

property in order to secure future tenants are missing. These would include:

marketing to new tenants;

management of the property’s leasing profile and tenant mix;

management of capital expenditure on the property (for example, decisions to repair, renovate,

redevelop and/or expand the commercial office tower); and

management of the initial and continued funding of the property.

Entity Y will not be able to produce outputs without these processes.

Step 3: Assess the capability of a market participant to produce outputs if missing elements exist

Entity Y is an owner and manager of real estate. No tenants or management of the building were acquired.

The building will form part of its larger portfolio going forward; entity Y’s management will perform this role.

Accounting treatment for business combinations and asset acquisitions

The accounting treatment for an acquisition that is a business combination differs from the accounting when

acquiring a group of assets that does not meet the definition of a business (that is, an asset acquisition).

The key considerations are explained below:

Asset acquisition

Business combination

Standard

IFRS 3 – apply scope exemption explained

in paragraph 2(b)

1

IFRS 3

Assets and liabilities

Allocate the purchase price to the individual

identifiable assets and liabilities on the

basis of their relative fair values

Recognise and measure the identifiable

assets and liabilities at their acquisition-

date fair values

Deferred tax

No deferred tax is recognised under IAS 12,

given the initial recognition exception [IAS

12 para 15(b)]

Deferred tax is recognised in accordance

with IAS 12

Goodwill

Not recognised

Recognise any related goodwill or negative

goodwill

Contingent liabilities

Not recognised, although the presence of

contingent liabilities might impact

transaction price and asset valuation

Contingent liabilities that are a present

obligation arising from past events and can

be reliably measured should be recognised

at fair value. This is the case even if it is not

probable that a future outflow of economic

benefits will occur

Transaction costs

Form part of the cost of the asset

Expensed in the period incurred

1

Paragraph 2(b) of IFRS 3 scopes out the acquisition of an asset or a group of assets that does not meet the definition of a

business. In such cases, the acquirer recognises the acquired assets and assumed liabilities in accordance with the relevant

standards. The cost should be allocated to the individual identifiable assets and liabilities on the basis of their relative fair

values at the purchase date.

Applying IFRS for the real estate industry

PwC 15

Asset acquisition

Business combination

Subsequent

measurement

implications

Follow relevant standards for each asset

Follow relevant standards for each asset

For contingent liabilities, these should be

measured at the higher of:

a the amount that would be recognised

under IAS 37; and

b the amount initially recognised less, if

appropriate, the cumulative income

recognised

Annual impairment test for any recognised

goodwill is required (see section 3.4.5)

Accounting for portfolio premiums/discounts

Entities acquire real estate properties either individually or in a portfolio. The price paid to acquire a portfolio

of properties in a single transaction could differ from the sum of the fair values of the individual properties.

Portfolio premiums (discounts) are the excess (shortfall) of the market value of a portfolio of properties over the

aggregate market value of the properties taken individually. Such premiums (discounts) affect the allocation

of consideration.

Portfolio premiums could arise as a result of a purchaser’s ability to build a portfolio immediately rather than

over a period of time, short supply in the market, or because of saved transaction costs. In some instances,

(expected) portfolio synergies might also result in portfolio premiums. In such a case, it is important to consider

whether the existence of a portfolio premium is an indicator of a business combination as opposed to the

acquisition of a group of assets.

Portfolio discounts could be granted by a seller in order to encourage a single buyer to purchase a large number

of properties, and thereby avoid future marketing and other administrative costs associated with selling

properties one-by-one.

The accounting for such portfolio premiums (discounts) at initial recognition differs, depending on whether the

transaction qualifies as a business combination or not.

The following table summarises the principles of accounting for portfolio premiums and discounts paid when

acquiring a portfolio of real estate properties:

Portfolio premiums

Business combination

Asset deal

Initial

measurement

The assets and liabilities acquired are

recognised at fair value, so any premiums or

discounts affect the amount of goodwill

arising from acquisition accounting.

If the discount results in negative goodwill

(bargain purchase), the gain is recognised in

profit or loss.

The consideration is allocated to the

underlying assets proportionately to their fair

value. Premiums (discounts) might result in a

higher (lower) amount being allocated to the

investment property when compared to its

fair value.

2.4. Asset acquisitions: Measurement at initial recognition

The rules for recognition of real estate that meets the definition of investment property are similar to those

for all other assets. Investment properties are initially recognised at cost, including transaction costs.

[IAS 40 para 20].

Cost is the amount of cash or cash equivalents paid or the fair value of other consideration given to acquire an

asset at the time of its acquisition or construction. [IAS 40 para 5].

Applying IFRS for the real estate industry

PwC 16

An entity might acquire investment property for an initial payment plus agreed additional payments contingent

on future events, outcomes or the ultimate sale of the acquired asset at a threshold price. The entity will usually

be contractually or statutorily obligated to make the additional payment if the future event or condition occurs.

This is often described as variable or contingent consideration for an asset. The accounting for contingent

consideration of an asset has been discussed by the IFRS Interpretations Committee (IC), although the IC has

not currently concluded on this issue.

There is diversity in practice in accounting for contingent consideration of an asset, with two approaches observed

in practice. The first is a cost accumulation model, whereby contingent consideration is not taken into account on

initial recognition of the asset, but it is added to the cost of the asset initially recorded, when incurred, or when a

related liability is remeasured for changes in cash flows. The second approach is a financial liability model,

whereby the estimated future amounts payable for contingent consideration are recorded on initial recognition of

the asset, with a corresponding liability. Any remeasurements of the related liability and any additional payments

are either recognised in the income statement or capitalised. The cost accumulation model is more common in

practice. Both approaches to accounting for contingent consideration of an asset acquisition are acceptable. This is

a policy choice that should be applied consistently to all similar transactions and appropriately disclosed.

Accounting for transaction costs, start-up costs and subsequent costs shortly

after acquisition

Cost is the purchase price, including directly attributable expenditures. Such expenditures include transaction

costs (such as legal fees and property transfer taxes) and, for properties under construction, borrowing costs in

accordance with IAS 23.

Except for transaction costs relating to acquisitions meeting the definition of a business combination, external

transaction costs are included in the cost of acquisition of the investment property.

The cost of acquired investment property excludes internal transaction costs (for example, the cost of an entity’s

in-house lawyer who spends a substantial amount of time drafting the purchase agreement and negotiating

legal terms with the seller’s lawyers). The entity cannot apportion the in-house lawyer’s salary and include an

estimated amount related to the work on the acquisition of a property into the cost of that property. The in-

house lawyer’s employment-related costs are internal costs that relate to ‘general and administrative costs’, and

they are not directly attributable to the acquisition of the property.

Example – Market study research costs

Background

Entity Y purchased an investment property in Lisbon. It performed a study of the real estate market in

Portugal before it purchased the property. Management proposes to capitalise the costs of this study.

Can management capitalise the real estate study costs?

Solution

No. The costs cannot be capitalised, since the costs of the market study are not directly related to the

acquired property. Such costs are pre-acquisition costs, and they are expensed as incurred.

Example – Determining fair value: treatment of transaction costs

Background

Entity A has a 31 December year end, and it adopts the fair value model for its investment properties

(see section 3.5).

Entity A acquired a property in December 20X5 at a cost of CU100, and it incurred transaction costs

amounting to CU5. There is no movement in the underlying market value of the property between the

acquisition date and the year-end date, so the fair value of the investment property at 31 December 20X5

is CU100.

Applying IFRS for the real estate industry

PwC 17

How should the entity account for the transaction costs incurred?

Solution

Investment property is initially measured at the cost of CU100, including transaction costs of CU5. [IAS 40

para 20]. Transaction costs include legal fees, property transfer taxes, etc., that are directly attributable to the

acquisition of the property. [IAS 40 para 21]. However, investment property measured subsequently at fair

value cannot be stated at an amount that exceeds its fair value. At 31 December 20X5, entity A should report

its investment property at the fair value of CU100 and recognise a loss of CU5 in its income statement.

The cost of an investment property excludes items such as:

start-up costs, unless they are necessary to bring the property to its working condition;

initial operating losses incurred before the investment property achieves the planned level of

occupancy; and

abnormal amounts of wasted material, labour or other resources incurred in constructing or developing

the property.

Such costs, incurred in the period after the acquisition or completion of an investment property, do not form part

of the investment property’s carrying amount, and they should be expensed as incurred. [IAS 40 paras 21–23].

An entity might incur costs subsequent to completion of a property but before it can be put to its intended use

(for example, where a regulatory approval must be obtained first).

Costs incurred subsequent to the completion of the property as explained above are:

expensed where they relate to maintenance of the building and attracting new tenants; or

capitalised where they enhance the value of the asset or where they help to bringing the asset to an

operational condition.

Example – Costs incurred subsequent to completion: prior to being fully let

Background

Entity M develops an office building for rental. Subsequent to completion of the building, it incurs expenses

(such as security, utilities and marketing) before the building has secured a reasonable level of occupancy.

The time between the building’s completion and securing a reasonable number of tenants is three months.

Management considers capitalising these operating costs that are incurred in this period.

Can entity M capitalise costs that are incurred after the date of completion of the property and prior to it

being fully let?

Solution

No. The costs should be expensed as incurred. These costs relate to maintaining the building and attracting

tenants. They are not necessary in bringing the asset to an operational condition.

Applying IFRS for the real estate industry

PwC 18

Example – Costs incurred subsequent to completion and prior to approval by relevant

government agency

Background

Entity N develops an office building for rental and incurs expenses (such as security and utilities) subsequent

to completion. The building was physically completed on 31 March, but the local health and safety regulator

did not clear the property for use until 30 June, when the security system met the required conditions. The

delay of three months in receiving health and safety approval is standard for the type and location of the

building. Entity N incurred CU100,000 security expenses in the period between 31 March and 30 June.

These costs were necessary in order to ensure that the required conditions for health and safety approval

could be satisfied.

Can entity N capitalise those costs in the period between the date of completion and the date when the

building receives approval for use from the relevant government agency?

Solution

Yes. The security expenses incurred during the period from 31 March to 30 June should be capitalised. The

legal requirement to receive the regulatory clearance meant that the building could not be put to its intended

use, although construction was completed on 31 March.

2.5. Accounting for forward contracts and options to acquire

real estate

Entities might enter into forward contracts or options for purchasing investment property. Contracts to buy a

non-financial asset (such as property) that are entered into for the purposes of receipt of that non-financial

asset are outside the scope of IAS 39/IFRS 9. [IAS 32 para 8]. Since the contract will be settled by physical

delivery of property (typically land) rather than by delivery of a financial asset or exchange of financial

instruments, it is not accounted for as a derivative (‘own use exemption’).

Entities usually make a small initial payment to enter into these contracts. This initial payment is recognised in

the balance sheet if it meets the definition of an asset. The cost can be measured reliably, since it is the amount

paid. If it is probable that the acquisition of the property will occur in the future, or economic benefits could be

derived from this option in some other way (for example, if it is possible to sell the option to a third party), the

recognition criteria for an asset are met.

The contract does not meet the definition of investment property, since it has not yet represented a current

interest in property. In substance, it is the first payment to secure the future acquisition of the property. If the

property is subsequently acquired, the amount paid for the option would form part of the cost of that property.

The amount paid to the owner of the property for the option or forward is recognised as a non-financial asset. If

future economic benefits are no longer expected to occur (for example, if acquisition of the property is no longer

probable and economic benefits cannot be derived from the option in any other way, such as the absence of the

ability to sell the option to another party or obtain a refund), the asset is derecognised. The asset would also

need to be assessed for indicators of impairment in accordance with IAS 36.

Where the asset is denominated in a foreign currency, an entity will need to determine whether the asset is

monetary or non-monetary in the context of IAS 21. For example, if the asset is non-refundable, it will be

treated as a non-monetary item; whereas, if the amount is fully refundable, it will be treated as a monetary item.

On initial recognition, the asset should be translated to the entity’s functional currency using the spot rate at the

date of the transaction. If the asset is a monetary item, it will need to be remeasured at each reporting date,

using the closing rate. If it is a non-monetary item, no remeasurement should be performed.

Applying IFRS for the real estate industry

PwC 19

Impact of IFRIC 22

IFRIC 22, effective for periods beginning on or after 1 January 2018, has confirmed the current accounting

practice for assets arising from advance payments to purchase non-monetary assets.

IFRIC 22 applies where an entity either pays or receives consideration in advance for foreign currency-

denominated contracts.

The Interpretation states that the date of the transaction, for the purpose of determining the exchange rate to

use on initial recognition of the related item, should be the date on which an entity initially recognises the non-

monetary asset or liability arising from the advance consideration.

If there are multiple payments or receipts in advance of recognising the related item, the entity should

determine the date of the transaction for each payment or receipt.

Example – Land options

Background

Entity A made a one-off payment to entity B for the option to buy entity B’s land within the next 10 years,

subject to planning permission for development being achieved. The price of the land will be based on

market value at the time of exercise, less the initial one-off payment already made. The initial one-off

payment for the option is non-refundable. Entity A plans to develop the land into investment property when

it is acquired. Entity A has a high expectation of purchasing the underlying land.

How should the initial payment for the land option be accounted for?

Solution

Provided that it is probable that entity A can derive future economic benefits from the land option, the one-

off payment is recognised as a non-financial asset in the statement of financial position.

Example – Purchase of an investment property: share deal

Background

Entity A enters into a forward contract to purchase 100% of the outstanding shares of entity X in six months’

time. Entity X holds a property that is currently rented out to a single lessee on a long-term lease contract.

The final purchase price is calculated as the pro rata share of the equity presented in the balance sheet of

entity X at the settlement date. The investment property held is accounted for under the fair value model in

entity X's financial statements. The contract does not contain any net settlement provisions.

Entity A will be required to consolidate entity X when control is transferred (see section 5.1). Entity A intends

to use the property as investment property.

Should entity A account for the forward purchase contract as a derivative within the scope of IAS 39/IFRS 9?

Solution

There are two permissible accounting approaches in this case. Entity A should select an accounting policy

approach and apply that approach consistently.

Accounting policy 1 – Forward purchase contract is accounted for as the purchase of an investment

property, based on the economic substance of the contract

The forward purchase contract has the economic substance of a contract to purchase investment property

and is outside the scope of IAS 39/IFRS 9 as a result of the own use exemption. [IAS 39 para 5; IFRS 9 para

2.4]. The economic substance needs to be considered; this is because the legal form of the purchase contract,

being a contract to purchase shares rather than an asset, should not impact the accounting.

Applying IFRS for the real estate industry

PwC 20

Accounting policy 2 – Forward purchase contract is accounted for as a derivative, based on the legal

structure of the contract

Entity A intends to purchase the outstanding shares of an entity. Therefore, the forward purchase contract is

within the scope of IAS 39/IFRS 9. Entity A has the right to receive 100% of the shares of entity X, and it has

the obligation to pay the purchase price at the settlement date. Accordingly, the forward purchase contract is

within the scope of IAS 39/IFRS 9.

Example – Purchase of an investment property: asset deal

Background

Entity A enters into a contract to purchase a property in six months’ time. Entity A is required to pay the

fixed purchase price for the property, and the counterparty is required to transfer all rights attached to the

property at the future settlement date. The contract does not contain any net settlement provision. Entity A

pays a small signing fee to the seller in order to enter into the purchase contract. The fee is deductible from

the final amount that entity A pays at the settlement date, and it is considered by the entity as a down

payment.

Entity A intends to use the property, which is rented out to a single lessee on a long-term lease contract, as an

investment property in accordance with IAS 40.

Should entity A account for the forward purchase contract to buy an investment property as a derivative

within the scope of IAS 39/IFRS 9?

Solution

Entity A enters into a contract to purchase a non-financial instrument which cannot be settled net in cash

and which has been entered into and is held for the purpose of delivery of the investment property for its own

use. The fee should be recognised as a deposit on the balance sheet.

2.6. Special considerations: investment properties under

construction

An entity might enter into a binding forward purchase agreement to purchase a completed property after

construction is completed. Where the contract requires the entity to pay a fixed purchase price, the entity will

need to consider whether the contract is onerous. A provision for onerous contracts is recognised if the

unavoidable costs of meeting the obligations under the contract or exiting from it exceed the economic benefits

expected to be received under it. [IAS 37 paras 66–69].

For example, if this fixed price had a net present value of CU100 million at the reporting date, and the

estimated economic benefits of the completed investment property at the reporting date is below that (say,

CU80 million), a loss of CU20 million is recognised immediately in the income statement. The resulting

provision is recognised on the balance sheet.

If there is an onerous contract as defined above, an impairment test is performed on any asset dedicated to the

contract (for example, prepayments made in relation to the purchase). Such assets relating to an onerous

contract are written down to the recoverable amount (see section 3.4 for further guidance on impairment), if

this is less than the carrying amount. [IAS 37 para 69]. A provision is recognised only after such asset is reduced

to zero.

Regardless of the assessment as to whether or not there is an onerous contract, contractual obligations to

purchase, construct or develop investment property, or for repairs, maintenance or enhancements, should be

disclosed. [IAS 40 para 75(h)].

Applying IFRS for the real estate industry

PwC 21

2.7. Accounting for rental guarantees

Sellers of real estate might provide guarantees to the potential buyers. A typical rental guarantee contract

usually has the following characteristics:

The seller guarantees a minimum tenancy level of the building.

The buyer does not need to meet certain requirements to be eligible to receive payment.

The payments under the guarantee do not change based on market yields, but rather they represent a

percentage of the initial purchase price of the building.

From the buyers’ perspective, contracts with the above characteristics are classified as available-for-sale

financial assets measured in accordance with IAS 39. The fair value of the contract is separated from the

purchase price on initial recognition of the property.

Subsequently, the rental guarantee asset is measured at fair value at each reporting date. Any changes in

amounts recognised as part of amortised cost are recognised in profit or loss. Any other difference between the

amortised cost and fair value is recognised in other comprehensive income.

Debt instruments for which the expected cash flows have changed are subject to the provisions of paragraph

AG8 of IAS 39 as follows:

The entity should revise its estimates of receipts by adjusting the carrying amount of the financial asset.

The difference between the carrying value and the revised amount, using the revised cash flows discounted

at the original effective rate, is recognised in profit or loss.

The accounting for contracts that contain additional guarantees beyond those for tenancy levels might differ

from that noted above. Entities should carefully examine the terms of the contract.

Impact of IFRS 9

Accounting for rental guarantees will change under IFRS 9. Under IFRS 9, the rental guarantee financial asset

would be classified as at fair value through profit or loss, since payments do not comprise payments of solely

principal and interest.

Example – Rental guarantees

Background

On 1 January 20X1, entity A acquired an investment property from entity B, a property developer, for CU100.

Entity B provided a rental guarantee to entity A as follows:

Entity B guarantees to entity A that if the property is not fully rented during the first three years post

acquisition, B will compensate entity A.

The maximum amount of compensation payable to entity A is 5% of the total purchase price paid by

entity A; if entity A is unable to rent the building to any tenants and the building remains vacant for each

of the first three years, entity B will pay CU5 (being 5% of the purchase price) to entity A.

Compensation for part occupancy of the building is calculated as the proportionate amount of the

maximum guarantee; for example, for 20% vacancy, the guarantee amount to be paid would be CU1 (that

is, 20% of CU5).

The fair value of the property, without the guarantee, at the acquisition date is CU97. On 31 December 20X1,

the fair value of the property without the guarantee is CU95. There are no transaction costs, no VAT and no

transfer tax. Entity A has an accounting policy to measure investment property at fair value.

At the acquisition date, the property is partially rented out (80%). Entity A expects the vacancy rates to be

constant over the next three years. Accordingly, entity A expects to receive CU3 over the next three years

Applying IFRS for the real estate industry

PwC 22

(CU1 per year). The fair value of the rental guarantee has been determined to be CU3 (for simplicity, the time

value of money has been ignored).

On 31 December 20X1, entity A received payment of CU1 compensation for the first year. Due to a change in

market conditions, the estimated vacancy rate for the second year increased to 40%. Entity A expects that

this will also be the case for the third year. The new cash flow projection estimates a payment of CU2 per year

for the next two years, resulting in a fair value of the rental guarantee at 31 December 20X1 of CU4.

How should entity A account for a rental guarantee provided by the seller of a property?

Solution

Entity A recognises the property and a rental guarantee financial asset on initial recognition. The financial

guarantee is recognised at fair value on initial recognition (CU3), and the remaining amount is allocated to

the investment property.

On initial recognition, the following is recorded:

Dr (CU)

Cr (CU)

Investment property (allocated cost)

97

-

Rental guarantee financial asset at fair value

3

-

Cash

-

100

As at 31 December 20X1, the investment property is measured at fair value, and fair value changes are

recognised in profit or loss.

Dr (CU)

Cr (CU)

Profit or loss

2

-

Investment property

-

2

Entity A receives a payment of CU1 from entity B, since the vacancy rate for the first year was 80%.

Dr (CU)

Cr (CU)

Cash

1

-

Rental guarantee financial asset at fair value

-

1

The carrying value of the rental guarantee financial asset (CU2) is then remeasured to fair value. To estimate

the fair value, entity A revises its estimates of the cash flows to be received from entity B over the next two

years. Entity A recalculates the carrying amount by computing the present value of estimated future cash

flows at the financial instrument's original effective interest rate.

The fair value of the available-for-sale asset would be CU4 (ignoring discounting). Since the change in

carrying amount is due to a change in expected cash flows calculated in accordance with paragraph AG8 of

IAS 39, the resulting increase in carrying value is recorded through profit or loss. In the event that there were

any further fair value changes beyond changes in expected future cash flows (for example, a change in market

rates that would have an impact on the discount rate used to measure the fair value), these would have been

recorded in other comprehensive income.

Dr (CU)

Cr (CU)

Rental guarantee financial asset

2

-

Profit or loss

-

2

Applying IFRS for the real estate industry

PwC 23

2.8. Development properties: accounting for the costs of

construction

Capitalisation of construction costs

Investment property under construction is initially measured at cost. Cost is usually the price paid to the

developer to construct the property, together with any directly attributable costs of bringing the asset to the

condition necessary for it to be capable of operating in the manner intended by management.

Costs that are eligible for capitalisation include, but are not limited to:

contract costs with the developer;

architecture fees;

civil engineer fees; and

staff costs for employees employed specifically for the construction process.

Costs that are not eligible for capitalisation include, but are not limited to:

feasibility studies in identifying development opportunities; and

staff costs for project management if these would be incurred irrespective of any development.

Demolition costs

An entity might acquire a property and demolish some of the existing buildings in order to construct new

buildings. Demolition costs are capitalised as part of the investment property if they are directly attributable to

bringing the asset to the location and condition for its intended use, [IAS 16 paras 16, 17(b)]. Depending on the

condition of the acquired property, these costs might be recognised as part of the cost of the land or the cost of

the building. Correct classification will impact future depreciation where the cost model is applied and the land

and building are subject to different depreciation rates.

Example – Demolition of a building: Scenario 1

Background

Entity A acquires a property for CU100 million.

The fair value of the property (land and building) is represented by the value of the land only, because the

current building on the land is derelict and unusable.

The building is demolished after purchase, in order to construct a new building in its place. Entity A incurs

demolition costs of CU3 million.

How should entity A account for the acquisition cost of the property and the costs of demolition?

Solution

Entity A should recognise CU100 million as the cost of the land, and it should not allocate any part of the

purchase price to the building. The purchased building is derelict and does not have stand-alone value, since

no market participant would be willing to pay consideration for an unusable building. [IAS 16 para 7]. The

economic rationale behind the purchase was to acquire land rather than land and a building. The sole

purpose of the demolition was to bring the land to its intended use, because it would not be available for use

until the building was demolished. Therefore, all consideration paid (CU100 million) should be allocated to

the land.

The demolition costs of CU3 million are capitalised as part of the cost of the land. In accordance with

paragraphs 16 and 17(b) of IAS 16, this represents costs directly attributable to bringing the land to the

condition necessary for it to be capable of being developed. Without demolishing the existing building, the

intended use of the land cannot be realised.

Applying IFRS for the real estate industry

PwC 24

Cost of:

Land (CU million)

Building (CU million)

Initial acquisition costs

100

-

Demolition

3

-

Cost – post demolition

103

-

Example – Demolition of a building: Scenario 2

Background

Entity B purchases land together with a building. The purchase price is CU200 million. The fair value of the

property is CU190 million for the land and CU10 million for the building. The building has value, because a

market participant would normally use the building rather than demolish it.

Entity B plans to demolish the building immediately after purchase, in order to construct a new building in

its place. The costs of demolishing the old building will be CU3 million.

How should entity B account for the acquisition cost of the property and the demolition costs?

Solution

Entity B should recognise CU190 million as the cost of the land and CU10 million as the cost of the purchased

building. This is because the purchased building has value, based on the fact that a market participant would

normally use the building rather than demolish it. The intended use of the land has already been achieved –

in contrast to the previous example, where the intended use had not been achieved because of the presence of

the derelict building on the land. On demolition, the carrying value of the building is derecognised and

expensed to the income statement.

The demolition costs of CU3 million are capitalised as part of the cost of the new building. In line with

paragraphs 16 and 17(b) of IAS 16, this represents costs directly attributable to constructing the new building,

and they are capitalised when incurred.

Cost of:

Land (CU million)

Building (CU million)

Initial acquisition costs

190

10

Demolition of old building

(10)

Demolition costs – part of new building

3

Cost – post demolition

190

3

Borrowing costs for properties under construction

The cost of investment property might include borrowing costs incurred during the period of construction.

Under IAS 23, borrowing costs are capitalised if an asset takes a substantial period of time to get ready for its

intended use. Capitalisation of borrowing costs is optional for qualifying assets that are measured at fair value

(for example, investment property under IAS 40). [IAS 23 para 4(a)].

Borrowing costs include, but are not limited to:

1. Interest expense calculated using the effective interest method, as described in IFRS 9/IAS 39;

2. Finance charges in respect of finance leases; and

3. Exchange differences arising from foreign currency borrowings, to the extent that they are regarded as

an adjustment to interest costs.

Applying IFRS for the real estate industry

PwC 25

Borrowing costs should be capitalised while construction is actively underway.

These costs include the costs of:

1. specific funds borrowed for the purpose of financing the construction of the asset; and

2. general borrowings, being all borrowings that are not specific borrowings for the purpose of obtaining a

qualifying asset. The general borrowing costs attributable to an asset’s construction should be calculated by

reference to the entity’s weighted average cost of general borrowings.

Capitalisation starts when all three of the following conditions are met:

1. expenditures for the asset are incurred;

2. borrowing costs are incurred, and

3. the activities necessary to prepare the asset for its intended use are in progress.

Capitalisation of borrowing costs in respect of real estate developments can commence before the physical

construction of the property (for example, when obtaining permits, completing architectural drawings, or other

activities necessary to prepare the property for its intended use.

Example – Capitalisation of borrowing costs

Background

Entity A contracts a third party for the construction of a building. Entity A will make progress payments to

the third party over the construction period of the building.

Entity A obtains a loan from the bank to finance the progress payments made to the third party, and it incurs

borrowings costs on this loan.

How should entity A account for the borrowing costs incurred?

Solution

The borrowing costs incurred by entity A to finance prepayments made to a third party to construct the

property are capitalised on the same basis as the borrowing costs incurred on an asset that is constructed by

the entity itself.

Capitalisation should start when:

a) expenditures are incurred – expenditures on the asset are incurred when the prepayments are made;

b) borrowing costs are incurred – borrowing costs are incurred when borrowing is obtained; and

c) the activities necessary to prepare the asset for its intended use are in progress – this is met when a

third party has started the construction process; determining whether construction is in progress will

likely require information directly from the contractor.

Income arising on redevelopment of property

Properties might need to be redeveloped following initial acquisition. Redevelopment might include structural