1

Contents

Introduction .................................................................................................................................................. 2

A Primer on VBA ............................................................................................................................................ 2

Subroutines, Programs, and Macros ......................................................................................................... 3

Object Models ............................................................................................................................................... 4

Using the Visual Basic Editor (VBE) ............................................................................................................... 6

Introduction to the @RISK XDK .................................................................................................................... 7

Setting Library References ............................................................................................................................ 9

Writing Your First @RISK Program .............................................................................................................. 10

@RISK Automation Guidelines.................................................................................................................... 11

Getting Started: the “Root” Object ......................................................................................................... 11

Running a Simulation .............................................................................................................................. 12

Changing Simulation Settings ................................................................................................................. 12

Displaying Numeric Results of a Simulation ........................................................................................... 12

Displaying Graphical Results of a Simulation .......................................................................................... 13

Creating Reports ..................................................................................................................................... 22

Listing Inputs and Outputs, and Graphing Input Distributions ............................................................... 22

Fitting Distributions to Data .................................................................................................................... 23

Creating Filters ........................................................................................................................................ 26

Goal Seek Analysis................................................................................................................................... 28

Advanced Sensitivity Analysis ................................................................................................................. 29

Stress Analysis ......................................................................................................................................... 30

Automating RISKOptimizer ..................................................................................................................... 31

Some General VBA Tips ............................................................................................................................... 33

File Format (xlsm) ................................................................................................................................... 33

Running a Macro ..................................................................................................................................... 34

ThisWorkbook ......................................................................................................................................... 34

Worksheet Code Names ......................................................................................................................... 34

With Blocks ............................................................................................................................................. 35

Intellisense .............................................................................................................................................. 35

Object Browser ....................................................................................................................................... 36

Constants and Enumerations .................................................................................................................. 37

2

Appendix ..................................................................................................................................................... 39

Updating @RISK 6.x or 7.x Automation Code to Run in @RISK 8.x ........................................................ 39

Updating RISKOptimizer 6.x or 7.x Automation Code to Run in @RISK 8.x ............................................ 45

Demand-Loading @RISK ......................................................................................................................... 47

Automating @RISK from .NET ................................................................................................................. 48

Automating RISKOptimizer from .NET .................................................................................................... 49

Introduction

The purpose of this document is to introduce the @RISK Excel Developer Kit (XDK) and explain how you

can use VBA to automate @RISK.

1

The term “automate” simply means that you write a program in VBA

to make @RISK do what you normally do through the @RISK user interface. For example, suppose you

often need to modify a financial planning simulation model. Each time you do this, you will change some

inputs distributions or their parameters, run one or more simulations, request various reports, and

create useful graphs. This requires a considerable number of steps—the same steps—each time you do

it. Wouldn’t it be nice to click a button and have all of these steps magically happen? This is exactly the

type of thing you will learn how to do with the @RISK XDK. In fact, it is surprisingly easy.

A Primer on VBA

2

As stated above, VBA is the programming language for Excel. It is also the programming language for

other applications in Microsoft Office: Word, PowerPoint, and Outlook, for example. It is even the

programming language for some non-Microsoft products. To understand how this works, it helps to

separate the name VBA into two parts: “Visual Basic” and “for Applications.” You can think of Visual

Basic, or VB, as the “backbone” programming language. It contains programming elements that all

programmers use, regardless of programming language or the type of development task. For example, it

contains subroutines, variable types, logical constructs such as If-Then-Else, loops for repetitive tasks,

arrays for storing lists, and much more. Actually, there are non-VBA versions of VB. For example, you

might be familiar with VB.NET. All of these versions of VB, including VBA, are extremely popular because

VB is fairly easy to learn and quite powerful. In any case, to learn VBA for Excel or @RISK, you must first

learn the backbone VB language.

The following is a typical segment of VB code. Even if you know nothing about programming, you will

probably have little trouble understanding what this code accomplishes. Again, this is the attraction of

VB. It is relatively easy to learn and understand. Note the lines that begin with an apostrophe. These

lines are comments. They are ignored by VBA when the program runs, but they are very useful for

documentation.

1

You must have the Professional or Industrial Edition of @RISK to run any automation code. The Standard Edition of

@RISK does not support automation.

2

If you are already familiar with VBA for Excel, you can skip to the section “Introduction to the @RISK XDK” on

page 5.

3

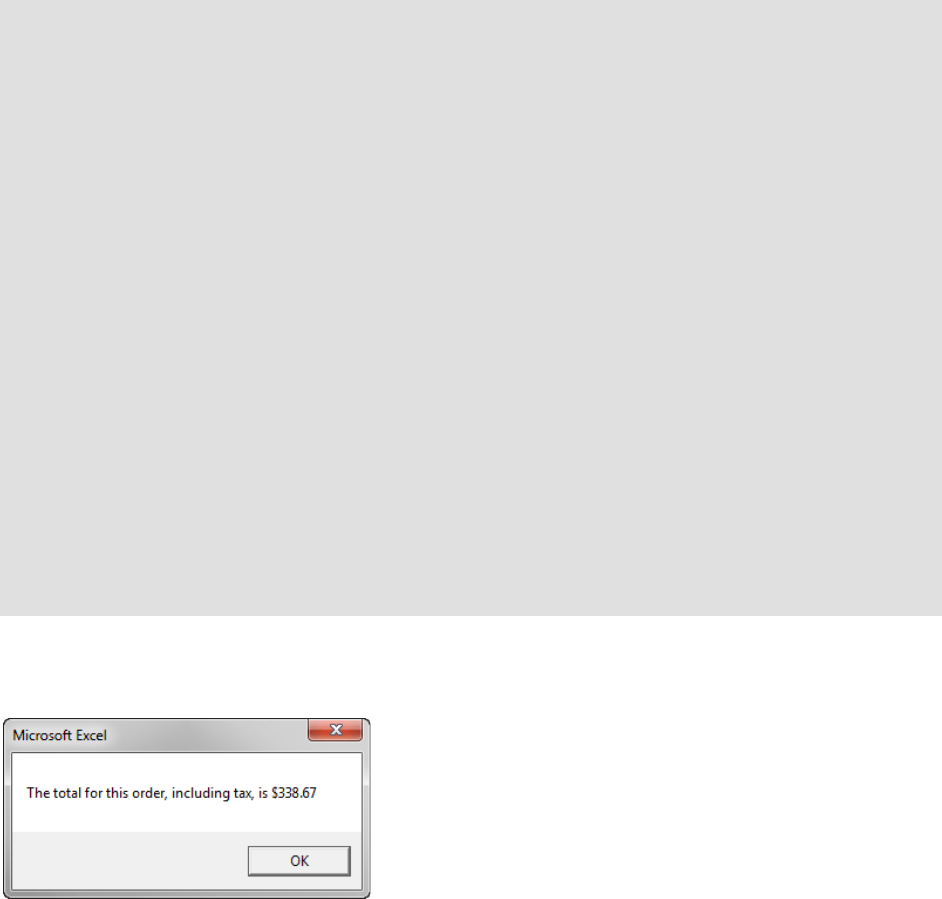

Sub Invoice()

' Declare variables.

Dim nProducts As Integer, i As Integer

Dim total As Currency, subTotal As Currency

Dim nPurchased As Variant, unitPrice As Variant

' Define constants for this business.

Const taxRate = 0.06

Const cutoff1 = 50, cutoff2 = 100

Const discount1 = 0.05, discount2 = 0.1

' Enter information about this order

nProducts = 4

nPurchased = Array(5, 2, 1, 6)

unitPrice = Array(20, 10, 50, 30)

total = 0

' Loop over all products purchased.

For i = 1 To nProducts

' Calculate revenue, including possible discount, for this product.

subTotal = nPurchased(i) * unitPrice(i)

If subTotal >= cutoff2 Then

subTotal = (1 - discount2) * subTotal

ElseIf subTotal >= cutoff1 Then

subTotal = (1 - discount1) * subTotal

End If

' Add to total for this order.

total = total + subTotal

Next

' Add tax.

total = (1 + taxRate) * total

' Display result.

MsgBox "The total for this order, including tax, is " & Format(total, "$#,#00.00")

End Sub

If you run this code in Excel, you will see the display (a message box) in Figure 1.

Figure 1 Result of VBA Program

Subroutines, Programs, and Macros

Before proceeding, it is useful to discuss three terms you often hear: subroutine, program, and macro. A

subroutine is any section of code that begins with the keyword Sub and ends with the keyword End Sub.

Its purpose is typically to perform one specific task. A program is a collection of one or more related

subroutines that achieves an overall goal. In practice, long programs are often broken up into smaller

subroutines for enhanced readability and easier debugging. A macro is essentially the same as a

program, and it is the term favored by many Excel programmers. However, if your programs are

relatively short, consisting of a single subroutine, the terms subroutine, program, and macro are

practically synonymous and are often used interchangeably.

4

Object Models

The above Invoice subroutine can be run in Excel, but it really has nothing to do with Excel. There are no

references to ranges, formulas, worksheets, charts, or other items you use in Excel. The code is pure VB.

But now we come to the “for Applications” part of VBA. All of the familiar items in Excel, which will now

be called objects, are part of an object model that Excel provides to programmers through VBA. This

means that you as a programmer can reference these objects in your VBA code. In short, this object

model allows you to “make things happen” through VBA code, rather than through the usual Excel user

interface. In this way, you can automate Excel with VBA.

So what does an object model, or Excel’s object model in particular, look like? At the top level, it is

simply a list of things—objects—that the software contains. Excel’s object model is quite large because

everything you see in Excel is an object. One of the most common objects is the Range object: any range

of cells (including a single cell). But there are over a hundred more objects, including the Worksheet

object, the Chart object, the PivotTable object, and so on. There are also singular and plural objects. For

example, there is the plural Worksheets object, the collection of all worksheets in an Excel workbook,

and there is the singular Worksheet object, a particular worksheet in the workbook.

Figure 2 displays a partial list of the objects in Excel, plural (yellow) and singular (blue).

5

Figure 2 Excel Object Model

However, there is much more to an object model than the list of its objects. First, there is a hierarchy

among many objects. Basically, this means that you often need to “drill down” to get to the object you

want. A good example is a Range object, such as cell B3. The idea is that a range is contained in a

worksheet, which is contained in a workbook. So the hierarchy is Workbook→Worksheet→Range, and

the following line of code is typical:

ActiveWorkbook.Worksheets(“Costs”).Range(“B3”).Value = 10

You read this as: Starting in the active workbook, go to cell B3 of the worksheet named Costs, and enter

the value 10. This concept of hierarchy is crucial to learning VBA for Excel or @RISK.

6

Second, most objects have properties and methods.

(Methods are also called functions.) If you think of

objects as “nouns,” then you can think of properties as “adjectives” and methods as “verbs.” Properties

describe an object, and methods indicate what you can do to, or with, an object. For example, a Range

object has a Value property, which was used in the above line of code. Similarly, a Font object has a

Color property, a Size property, and many others. A typical object with methods is the Worksheet

object. It has a Delete method, a Move method, and a few others.

Although less common, many objects also have events that they respond to. A good example is the

Open event of a Workbook object. This event occurs—it “fires”—when you open the workbook. VBA

allows you to write event handlers for the event. This is code that is executed when the event fires.

As you begin VBA programming for Excel, you gradually learn the most common objects, the hierarchies

between them, their most common properties, methods, and events, and the syntax for using these in

VBA code. It takes practice and perseverance, but if you want to make Excel “sing and dance” with the

click of a button, this is time well spent.

By now, you should be starting to see the big VBA picture. Just as the Excel application can be

automated through its object model, other applications can be automated through their object models.

Microsoft Word is a typical example. Its objects are not the same as Excel’s. Instead of Worksheet,

Range, and other typical Excel objects, Word has Sentence, Paragraph, and other objects that are useful

in word processing, and these objects have their own hierarchies, properties, methods, and events.

Fortunately, if you already know VBA for Excel and you want to learn VBA for Word, all you need to

learn is the object model for Word. The backbone VB language is exactly the same in both applications.

Admittedly, it is not a trivial task to learn a new application’s object model, but knowing VB for one

application, like Excel, provides a big head start for learning VB for another application, like Word.

Using the Visual Basic Editor (VBE)

You will be doing all of your programming in the Visual Basic Editor (VBE). The easiest way is to open

VBE from Excel is to press Alt+F11. Alternatively, if the Excel Developer tab is visible, you can click the

Visual Basic button on its ribbon. The VBE window appears in Figure 3. In particular, the Project pane on

the left shows a list of all open workbooks. (To get back to the Excel window, you can click the Excel icon

on the toolbar below the menu bar.)

7

Figure 3 Visual Basic Editor

As you can see in the figure, the selected file contains a module. You will write all of your code in

modules. (Actually, there are exceptions to this, but they aren’t discussed here.) By default, a file

doesn’t contain a module, but you can insert one through the Insert menu. Then you will see a big white

space on the right where you can start typing your code. Some of the code for this particular module

appears in the figure.

Introduction to the @RISK XDK

Like Excel and Word, @RISK has its own object model, part of which is shown in Figure 4. It can be used

to change application or simulation settings, run simulations, generate summary statistics or graph of

inputs or outputs, create reports, and more. The details of these possibilities are discussed in some

detail later in this document and in the accompanying @RISK XDK example files.

Two questions probably come to mind. Do you really need to learn how to automate @RISK with VBA,

and, if you do, how do you learn the language?

There are at least two reasons why you might want to automate @RISK with VBA. First, it lets you

automate tasks that you perform repeatedly. For example, suppose you need to download the most

current data from a website, use @RISK to fit a distribution to the data, run an @RISK simulation, and

finally create some standard @RISK reports. If you do this once or twice, it is probably not worth the

effort to write a VBA program to automate the process. However, if you do this repeatedly, a VBA

program can replace many mouse clicks with a single click. Indeed, this is why VBA for Excel is so popular

among users—it lets them automate repetitive tasks with the click of a button. The same motivation

certainly applies to repetitive tasks in @RISK.

8

Figure 4 @RISK Object Model

Second, suppose you are developing models for colleagues or clients who have little experience with

@RISK. Instead of teaching them how the @RISK user interface works, it might be easier to develop a

VBA application that allows them to simply click a button, or possibly click a menu item from your own

customized menu, to make things happen. These “things” could include (1) entering @RISK distributions

into particular cells, (2) designating @RISK outputs, (3) changing @RISK settings, (4) running the

simulation, (5) displaying selected graphs and/or summary statistics, and other @RISK tasks.

Assuming you think VBA for @RISK is for you, how do you learn the language? First, you need some

facility in VBA for Excel. As discussed earlier, this requires you to learn the fundamentals of the VB

“backbone” language and the basics of the Excel object model. There are a number of reference books

on VBA for Excel, as well as Excel’s own online help. One recommendation is the first 11 chapters of VBA

for Modelers by Albright. This book provides concise explanations and plenty of example code to get you

up to speed in both the VB language and the Excel object model.

Once you are familiar with VBA for Excel, you have at least four options—which are not mutually

exclusive—for extending your knowledge to VBA for @RISK.

1. You can continue reading this document. It provides an overview of what can be done, and it

provides sample code for how to do it. Alternatively, you can watch the first two introductory videos

9

that cover much of the same material. They are available from the Developer Kit (XDK) item under

@RISK Help.

2. You can do what all good programmers do—mimic code written by others. Examples of programs

written for @RISK are provided in a number of @RISK XDK example files. (They can be found from

Developer Kit (XDK) item under @RISK Help.) Once you see how something is done, such as

changing an @RISK setting or creating an @RISK graph, you will probably have little difficulty

adapting the code for your own use.

3. You can open one of the Reference documents from the Developer Kit (XDK) item under @RISK Help

and start browsing. These documents are quite long, and no sane person would ever read them

from beginning to end, but they give you a quick sense of the @RISK object model (or the

RISKOptimizer object model), and they often enable you to find the specific details you need for

your program.

4. You can open the Object Browser that is part of the Visual Basic Editor. This is particularly useful if

you are in the midst of writing a program and need information on one specific detail. The Object

Browser is discussed later in this document.

By the way, if you are familiar with VBA for Excel, you might want to start by recording macros for

@RISK, just as you can do for Excel. Unfortunately, this doesn’t work. If you turn on the recorder and

start clicking @RISK buttons, you will get some recorded code, but it will be entirely irrelevant. To

automate @RISK, you have to write the code.

Setting Library References

Before you can access the @RISK XDK with VBA code, you must first set references to two @RISK

libraries (from References in the Tools menu of the Visual Basic Editor). These are the RiskXLA and

Palisade_Risk_XDK8 references, illustrated in Figure 5. (The former references the Risk.xla add-in file.

The latter contains the @RISK Object Model.) This should be the first step before writing any VBA

macros to automate @RISK. If you plan to automate RISKOptimizer, you will need to check Palisade

RISKOptimizer 8.x for Excel Developer Kit reference too; that reference is also listed in the screen shot.

10

Figure 5 @RISK References

Writing Your First @RISK Program

This section won’t teach you a lot about VBA for @RISK, but it will give you the thrill of developing a

simple @RISK application with VBA—and getting it to work! Here are the steps:

1. Launch @RISK. (This document assumes you are using version 8.x.)

2. Select the Tutorial (before Code Added) item from the Automating @RISK (XDK) menu under

the Resources ribbon item and save it to a folder on your hard drive. This file contains a simple

@RISK model with several revenue and cost inputs and a single NPV output.

3. Open the Visual Basic Editor (VBE) with left Alt+F11.

4. Make sure the correct item is selected in the Project pane. Then from the VBE’s Insert menu,

select Module.

5. From the VBE’s Tools menu, select References, check the two @RISK items shown in Figure 5,

RiskXLA and Palisade_Risk_XDK8, and click OK.

6. Copy the following code and paste it into the Module window.

3

Option Explicit

Sub FirstProgram()

' Obtain object representing the worksheet where we'll place the results.

Dim modelWorksheet As Worksheet

Set modelWorksheet = Worksheets("Model")

3

The top line, Option Explicit, forces you to declare all variables you use in your program, a highly recommended

programming practice. To make this line appear automatically at the top of all your modules, select Options from

the Tools menu in the Visual Basic Editor and check Require Variable Declaration in the Editor tab.

11

' Change some simulation settings

With Risk.Simulation.Settings

.NumSimulations = 1

.NumIterations = 5000

.AutomaticResultsDisplay = RiskAutomaticResultsDisplay_NoAutomaticResults

End With

' Run simulation

Risk.Simulation.Start

' Display results

With Risk.Simulation.Results

' Summary statistics of output

With .GetSimulatedOutput("NPV")

modelWorksheet.Range("C19").Value = .Mean

modelWorksheet.Range("C20").Value = .StdDeviation

modelWorksheet.Range("C21").Value = .PToX(0.05)

modelWorksheet.Range("C22").Value = .PToX(0.95)

End With

' Use cell E19 to define the location of the graph.

Dim left As Long

Dim top As Long

left = modelWorksheet.Range("E19").left

top = modelWorksheet.Range("E19").top

' Graph of output distribution

With .GraphDistribution("NPV")

.ImageToWorksheet modelWorksheet, RiskImageFormat_BMP, left, top, 300, 250

End With

End With

End Sub

7. From the VBE’s Run menu, select Run Sub/Userform (or press the F5 key). In seconds, your

active Model worksheet should fill up: the @RISK simulation will run and selected numerical and

graphical results will appear. Now you see what automation is all about!

This program should be fairly simple to read, even if you know very little about VBA. The results of this

exercise should be just like in the workbook that can be opened using the Tutorial (after Code Added)

menu item. The next “Guidelines” section explains many of the details, and the following “VBA Tips”

section provides some general tips on using VBA effectively.

@RISK Automation Guidelines

This section provides some guidelines for automating @RISK with VBA code. The guidelines in this

section are purposely kept brief and are intended only to get you started and alert you to a few

technical issues. To see complete applications of @RISK automation, you should look at the examples,

available in the Automating @RISK XDK menu under the Resources ribbon item. Also, you can always

visit the @RISK XDK Reference documents or the Object Browser in the Visual Basic Editor.

Getting Started: the “Root” Object

The “root” object that everything starts from is the Risk object, a reference to @RISK. All other @RISK

objects are down the hierarchy from it. For example, you will see Risk.Model, Risk.Simulation, and

others. Many of these will be discussed shortly.

12

Technical Note: Risk Function versus AtRisk Object

There is a subtle issue here you should be aware of. As it is used here, Risk is a function in the RiskXLA

library that returns an AtRisk object from the object library. To put it another way, if you did not

reference the RiskXLA library and wrote a typical line such as the following, Risk wouldn’t be recognized.

Risk.Simulation.Settings.NumIterations = 1000

However, if you do reference RiskXLA, as you should, you can simply write Risk, followed by any of its

properties or methods, and it will work fine. (In particular, you do not need to declare Risk as an object

variable.)

Running a Simulation

Risk.Simulation refers to the simulation model currently open. You can use it to run a simulation with a

single line of code:

Risk.Simulation.Start

Technical Note: What Is a Simulation?

It is important to realize what a “simulation” refers to, either in VBA or in the @RISK user interface itself.

It refers to everything that is currently open. For example, if you have logically distinct simulations in

multiple worksheets of a workbook, Risk.Simulation refers to all of them. Or if you have multiple

workbooks open, each with its own logically distinct simulation, Risk.Simulation again refers to all of

them. There is no way to refer to one specific simulation among many, so be careful!

Changing Simulation Settings

You get to the simulation settings with Risk.Simulation.Settings. Then you can have code such as the

following that changes a few settings. Of course, this code should come before the line that runs the

simulation.

With Risk.Simulation.Settings

.NumSimulations = 5

.NumIterations = 5000

.AutomaticResultsDisplay = RiskAutomaticResultsDisplay_NoAutomaticResults

End With

Risk.RefreshUI ‘ this line ensures that the Excel ribbon will update to show the changes

Displaying Numeric Results of a Simulation

Once you run a simulation, you can get to the results with Risk.Simulation.Results. This can be followed

by two functions, GetSimulatedInput and GetSimulatedOutput, which enable you to get summary

statistics such as the mean, the standard deviation, and percentiles of an input or output. For example,

the following line enters the mean of the Profit output in cell B20.

Range(“B20”).Value = Risk.Simulation.Results.GetSimulatedOutput(“Profit”).Mean

Alternatively, assuming multiple simulations are run, the following line enters the 5

th

percentile of the

Q1_Cost input for simulation #3 in cell B15.

Range(“B15”).Value = Risk.Simulation.Results.GetSimulatedInput(“Q1_Cost”,3).PToX(0.05)

13

The arguments of GetSimulatedOutput specify the output you want. The first argument is either the

name of the output, implicitly or explicitly defined in the RiskOutput function, or a cell reference. (It can

also be an integer, such as 3, meaning the third output, but this isn’t usually a good practice unless you

are sure of the ordering of the outputs.) An optional second argument when there are multiple

simulations is the index of the simulation. The arguments of GetSimulatedInput are similar, except that

if a name is used for the first argument, it must be the name specified in the RiskName property

function. For example, if the formula in an input cell is =RiskNormal(1000,100,RiskName(“Q1_Cost”)),

then the name “Q1_Cost” can be referenced.

Note that if you ask for the results of a simulation that has not yet been run, you will get an error. You

can check for this with the following line:

If Not Risk.Simulation.Results.Exist Then Risk.Simulation.Start

Alternatively, if this condition is true (no simulation results exist), you could display an error message,

informing the user that a simulation needs to be run, and then quit prematurely. The following code

illustrates what this might look like.

Sub RunWithErrorCheck()

If Not Risk.Simulation.Results.Exist Then

MsgBox "You need to run a simulation first.", vbInformation

Exit Sub

Else

Range("B20").Value = Risk.Simulation.Results.GetSimulatedOutput("Profit").Mean

End If

End Sub

Displaying Graphical Results of a Simulation

You can use the RiskGraph object to create a variety of graphs. Starting with Risk.Simulation.Results,

you can use a number of functions that return a RiskGraph object: GraphDistribution, GraphScatter,

GraphSensitivityTornado, etc. Because these functions return different types of graphs, their arguments

vary slightly, as will be explained shortly. However, you typically use the following three steps with all of

them.

1. Set a reference to a graph.

Dim rGraph As RiskGraph

Set rGraph = Risk.Simulation.Results.GraphDistribution(“Profit”)

2. Change one or more properties of the graph.

rGraph.TitleMainText = “Distribution of Profit”

3. Send the image of the graph to a worksheet, where the last four arguments determine the size and

position of the graph. (You can also send the image to the clipboard or to a file with the

ImageToClipboard or ImageToFile functions.)

rGraph.ImageToWorksheet ActiveSheet, RiskImageFormat_BMP, 100, 100, 300, 250

Equivalently, you can do all of these steps with the following With block, without requiring the rGraph

variable. Note that the first line creates an implicit RiskGraph object, so that you can refer to its

TitleMainText property and its ImageToWorksheet method in the next two lines.

With Risk.Simulation.Results.GraphDistribution(“Profit”)

.TitleMainText = “Distribution of Profit”

.ImageToWorksheet ActiveSheet, RiskImageFormat_BMP, 100, 100, 300, 250

End With

14

Should you use explicit object variables such as rGraph? This is a matter of personal preference, and it

sometimes depends on the situation. However, once you get used to programming with object models,

you will probably prefer to omit such variables whenever possible.

The following sections provide more information about the graph types. Of course, you can find detailed

information in online help or the Object Browser. Keep in mind that the graphs shown in the figures are

“plain vanilla” versions, which often suffice. However, you can change the many properties of a

RiskGraph object to fine-tune the graph as you like: the titles, the axes, the plot area color, and so on.

GraphDistribution Function

The GraphDistribution function is usually used to graph the distribution of an output, although it can

also be used to graph the distribution of an input. This function takes an output, an input, or an array of

inputs and/or outputs as its first argument and an optional second argument that can be a simulation

index or an array of simulation indexes.

4

Here is a simple example. The result appears in Figure 6.

Sub GraphDistribution_Histogram()

Risk.Simulation.Start

With Risk.Simulation.Results.GraphDistribution("Profit")

.ImageToWorksheet ActiveSheet, RiskImageFormat_BMP, 10, 300, 300, 250

End With

End Sub

By default, this code provides a histogram, but you can use the DistributionDisplayFormat property to

change the display type. For example, the following code changes the display type to a cumulative

ascending graph, as shown in Figure 7.

Sub GraphDistribution_CumulativeAscending()

Risk.Simulation.Start

With Risk.Simulation.Results.GraphDistribution("Profit")

.DistributionDisplayFormat = RiskDistributionDisplayFormat_CumulativeAscending

.ImageToWorksheet ActiveSheet, RiskImageFormat_BMP, 10, 300, 300, 250

End With

End Sub

4

Actually, if you are graphing an input, there is an optional third Boolean argument, indicating whether you want

to suppress an overlay of the theoretical distribution on the graph. It is False by default.

15

Figure 6 Graph of Profit Distribution

Figure 7 Cumulative Ascending Graph of Profit Distribution

The following code requests a graph of a Profit output, overlaid with a Q1_Cost input, for simulation #2.

The last argument, True, indicates that the theoretical distribution of the input should be suppressed.

The result is shown in Figure 8.

Sub GraphDistribution_HistogramOverlay1()

Risk.Simulation.Start

With Risk.Simulation.Results.GraphDistribution(Array("Profit", "Q1_Cost"), 2, True)

.ImageToWorksheet ActiveSheet, RiskImageFormat_BMP, 10, 300, 300, 250

End With

End Sub

As another example, the following code requests a graph of Profit for simulation #1, overlaid with a

similar graph for simulation #3, as shown in Figure 9.

16

Sub GraphDistribution_HistogramOverlay2()

Risk.Simulation.Start

With Risk.Simulation.Results.GraphDistribution("Profit", Array(1, 3))

.ImageToWorksheet ActiveSheet, RiskImageFormat_BMP, 10, 300, 300, 250

End With

End Sub

Figure 8 Graph of Profit Distribution with Q1_Cost Overlay for Simulation #2

Figure 9 Graph of Profit Distribution for Simulations #1 and #3

17

GraphSummaryBoxPlot/GraphSummaryTrend Functions

The GraphSummaryBoxPlot/GraphSummaryTrend functions are usually used to graph a time series of

outputs, such as monthly cash flows. Their arguments include a reference to the output range and an

optional simulation index. This last argument can be an array of simulation indexes, in which case the

curves are shown side-by-side. The following code generates the summary trend graph in Figure 10 for

the cash flows from simulation #3.

Sub GraphSummary_Trend()

Risk.Simulation.Start

With Risk.Simulation.Results.GraphSummaryTrend(Range("Cash_Flow"), 3)

.ImageToWorksheet ActiveSheet, RiskImageFormat_BMP, 10, 300, 300, 250

End With

End Sub

Similarly, the following code generates the summary box plot in Figure 11.

Sub GraphSummary_BoxPlot()

Risk.Simulation.Start

With Risk.Simulation.Results.GraphSummaryBoxPlot(Range("Cash_Flow"), 3)

.ImageToWorksheet ActiveSheet, RiskImageFormat_PNG, 10, 300, 300, 250

End With

End Sub

Figure 10 Summary Trend Graph of Cash Flows for Simulation #3

18

Figure 11 Summary Box Plot of Cash Flows for Simulation #3

GraphScatter Function

The GraphScatter function returns a scatter graph. It requires at least two arguments, the first for the X-

axis and the second for the Y-axis, and an optional third argument equal to a single simulation index (an

array isn’t allowed). Each of the first two arguments can be an output, an input, or an array of outputs

and/or inputs. (Note that if you try to create a scatter graph of a variable versus itself, you will get an

empty graph.) Here is a simple example of the Profit output versus the Q1_Cost input. It results in the

graph in Figure 12.

Sub GraphScatter_OneScatter()

Risk.Simulation.Start

With Risk.Simulation.Results.GraphScatter("Q1_Cost", "Profit")

.ImageToWorksheet ActiveSheet, RiskImageFormat_PNG, 10, 300, 300, 250

End With

End Sub

The following code creates two scatters (in the same graph) for simulation #2, as shown in Figure 13.

The first is of Profit versus Q1_Cost, and the second is of Profit versus Q1_Revenue.

Sub GraphScatter_TwoScatters()

Risk.Simulation.Start

With Risk.Simulation.Results.GraphScatter(Array("Q1_Cost", "Q1_Revenue"), "Profit", 2)

.ImageToWorksheet ActiveSheet, RiskImageFormat_PNG, 10, 300, 300, 250

End With

End Sub

19

Figure 12 Scatter Graph of Profit versus Q1_Cost

Figure 13 Scatters of Profit versus Q1_Cost and Profit versus Q1_Revenue for Simulation #2

GraphSensitivityTornado Function

The GraphSensitivityTornado function returns a tornado graph, which is used to see how sensitive an

output is to the inputs. It has two required arguments, a reference to an output and a

RiskSensitivitySettings object. Among the RiskSensitivitySettings properties is the CalculationMethod: for

example, we can calculate sensitivities using correlation coefficients or regression coefficients.

20

The following code generates a tornado graph for the Net Present Value using the

“RiskSensitivityTornadoFormat_ChangeInOutputStatistic” calculation method with a maximum of 4 bars,

as shown in Figure 14. To get any of the other tornado types, you simply change the second argument to

one of the constants listed above.

Sub GraphTornado_ChangeInMean()

Risk.Simulation.Start

Dim sensSettings As New RiskSensitivitySettings

sensSettings.CalculationMethod = RiskSensitivityTornadoFormat_ChangeInOutputStatistic

sensSettings.GraphMaxTornadoBars = 4

With Risk.Simulation.Results.GraphSensitivityTornado("NPV", sensSettings)

.ImageToWorksheet ActiveSheet, RiskImageFormat_PNG, 10, 300, 300, 250

End With

End Sub

GraphSensitivitySpider Function

The GraphSensitivitySpider function returns a spider graph, another type of graph for seeing how

sensitive an output is to the inputs. It has only one required argument, a reference to the output.

The following code generates a spider graph for Profit with a maximum of 4 lines, as shown in Figure 15.

Sub GraphSpider()

Risk.Simulation.Start

Dim sensSettings As New RiskSensitivitySettings

sensSettings.GraphMaxSpiderLines = 4

With Risk.Simulation.Results.GraphSensitivitySpider("NPV", sensSettings)

.ImageToWorksheet ActiveSheet, RiskImageFormat_PNG, 10, 300, 300, 250

End With

End Sub

Figure 14 Tornado Graph for NPV

21

Figure 15 Spider Graph for NPV

GraphScenarioTornado Function

The GraphScenarioTornado function returns a type of tornado graph for seeing which inputs are most

responsible for an output scenario. A typical example appears in Figure 16. The scenario is that the NPV

output is greater than its 90

th

percentile, and the question is which inputs are most responsible (in the

sense of being at their extremes) for these large NPV values. As you can see, the Product_lifetime input

is at the top of the list. Its “subset median,” the median of its values in the subset of iterations where

the scenario occurs, is at the 87.5

th

percentile of the median of this input for all iterations. The other

number listed, 1.33, is the difference between the input’s subset median and its overall median, divided

by the standard deviation of the input for all iterations. In other words, the input’s subset median for

the scenario is 1.33 standard deviations above its overall median.

The function has four required arguments: (1) a reference to the output, (2) a minimum scenario value,

(3) a maximum scenario value, (4) whether the minimum and maximum values are percentiles (as

opposed to actual values. The following code is typical and leads to the graph in Figure 16.

Sub GraphScenarioTornado()

Risk.Simulation.Start

With Risk.Simulation.Results.GraphScenarioTornado("NPV", 0.9, 1, True)

.ImageToWorksheet ActiveSheet, RiskImageFormat_PNG, 10, 300, 300, 250

End With

End Sub

22

Figure 16 Scenario Tornado Graph for NPV

Creating Reports

The standard @RISK reports found on the ribbon can also be created using code. The options available

in the dialogs used to generate reports are also available in code. The code below will make a report

showing all the outputs, save it to the specified location as a PDF file, and open the file.

With Risk.Simulation

' Generate a report using one of the built-in formats.

' Select to make it a PDF file on the desktop and to open it for the user to view.

.Results.Reports.CreateOutputReport RiskReportOutputsSubType_CompactOutput, _

RiskDistributionDisplayFormat_ProbabilityDensity, _

RiskReportDestinationType_PDF, _

"C:\Users\John\Desktop\AtRiskXDKReport.pdf", _

True

End With

Listing Inputs and Outputs, and Graphing Input Distributions

It is sometimes handy to list of all @RISK inputs and outputs in a worksheet. You can do this in VBA with

Risk.Model, as shown in the following code:

Sub ListInputsOutputs()

Dim i As Long

Dim left As Long, top As Long, width As Long, height As Long

Dim modelDefinition As RiskModelDefinition

Dim modelInput As RiskModelDefinitionInput

Dim modelOutput As RiskModelDefinitionOutput

‘Storing reference to this object in a variable is optional.

‘Passing True as the parameter will cause the workbooks to be rescanned for changes;

‘this will ensure that the information is up-to-date, reflecting the latest

23

‘changes made by the user.

‘Pass False for performance reasons, if you know changes have not occurred.

Set modelDefinition = Risk.Model.GetModelDefinition(True)

‘ Create worksheet where we will write the information about inputs and outputs.

Dim wsInputsOutputs As Excel.Worksheet

Set wsInputsOutputs = ActiveWorkbook.Worksheets.Add()

' Write information about all input functions

With wsInputsOutputs.Range("B3")

For i = 1 To modelDefinition.ModelInputs.Count

Set modelInput = modelDefinition.ModelInputs.Item(i)

.Offset(i, 0).Value = i

.Offset(i, 1).Value = modelInput.Location.Worksheet.Name

.Offset(i, 2).Value = modelInput.Location.Address

.Offset(i, 3).Value = modelInput.RiskFunction

.Offset(i, 4).Value = modelInput.Name

Next

End With

' Write information about all output functions

With wsInputsOutputs.Range("H3")

For i = 1 To modelDefinition.ModelOutputs.Count

.Offset(i, 0).Value = i

Set modelOutput = modelDefinition.ModelOutputs.Item(i)

.Offset(i, 1).Value = modelOutput.Location.Worksheet.Name

.Offset(i, 2).Value = modelOutput.Location.Address

.Offset(i, 3).Value = modelOutput.RiskFunction

.Offset(i, 4).Value = modelOutput.Name

Next

End With

' Graph theoretical input distributions

left = 10: top = 125: width = 300: height = 250

With Risk.Model

For i = 1 To modelDefinition.ModelInputs.Count

With .GraphDistribution(modelDefinition.ModelInputs.Item(i).Location)

.ImageToWorksheet wsInputsOutputs, RiskImageFormat_BMP, left, top, width, height

End With

If i < modelDefinition.ModelInputs.Count Then left = left + width + 5

Next

End With

wsInputsOutputs.Activate

End Sub

This code also illustrates another graph option, the GraphDistribution method of the RiskModel object.

(Don’t confuse this with the GraphDistribution function for simulated results discussed earlier). This

allows you to create the graph of a theoretical input distribution. Its argument can be a range, as in the

above code, an @RISK distribution function such as RiskNormal(100,10), or an array of these (for an

overlay).

Fitting Distributions to Data

If you have used @RISK’s fitting tools, either for fitting to a single column of data or for batch fitting to

several columns of data, you know that this can be done through the @RISK user interface with only a

few mouse clicks. However, this user interface has a lot of settings you can change, and this leads to a

fairly complex set of objects for fitting in the @RISK object model.

24

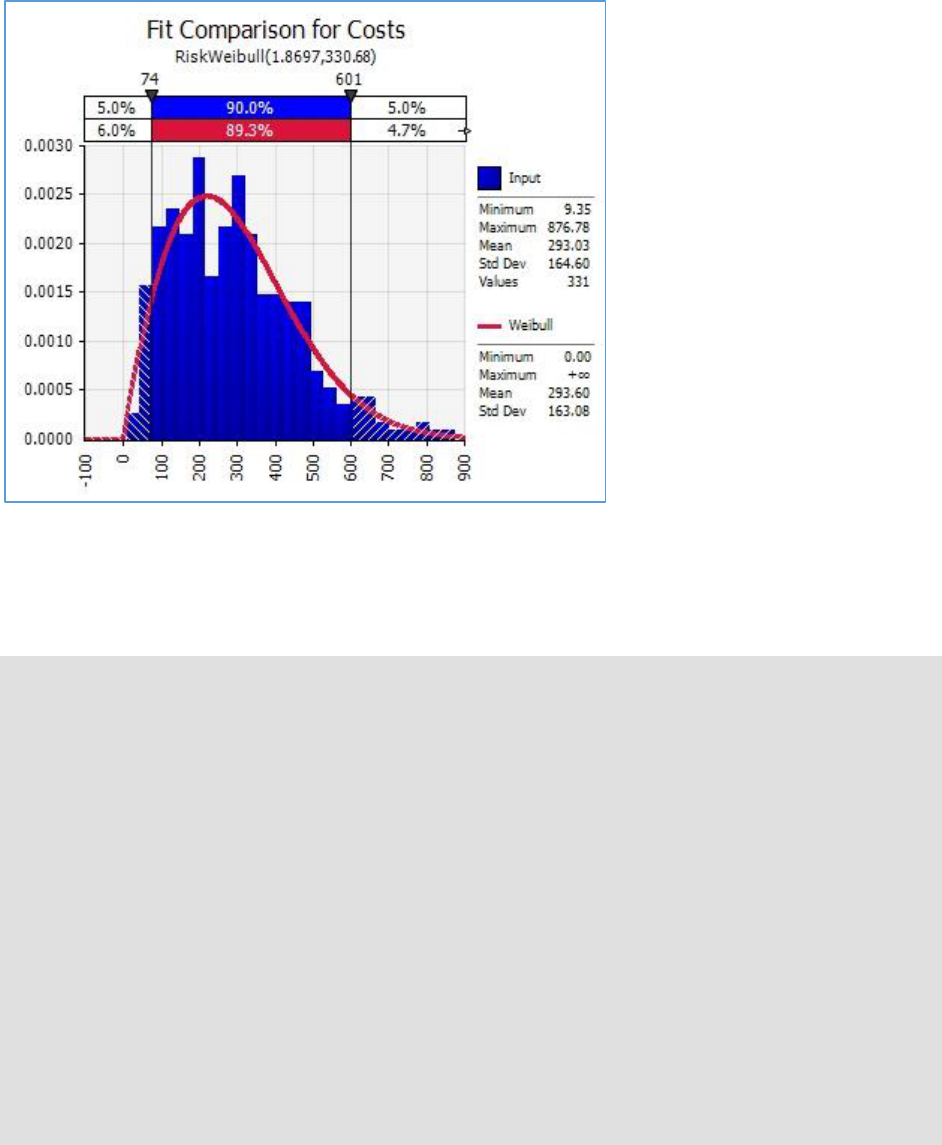

The following code illustrates the most basic features. This fits nonnegative distributions to historical

cost data. It first creates a fit definition and sets some of its properties. Then it performs the fitting, it

lists several summary statistics of the data, and it lists several summary statistics and graphs of the best-

fitting distribution. For example, the GraphFitComparison function creates the graph in Figure 17. This

shows the best-fitting distribution superimposed on the histogram of the cost data.

Sub FitTest()

Dim msg As String

' Delete graphs if any

DeleteGraphs wsData

' Delete named fit if it already exists

On Error Resume Next

Risk.Fits.Item("Costs").Delete

' Create fit definition

With Risk.Fits.Add(Range("Cost_Data"), RiskFitDataType_ContinuousSamples, "Costs")

.BestFitSelectorStatistic = RiskFitStatistic_AIC

.LowerLimitType = RiskFitLimitType_Fixed

.LowerLimitValue = 0

.UpperLimitType = RiskFitLimitType_Open

.SuppressQuestionableFits = True

With .PerformFit

With .FitInput

' Information about data

msg = "Summary stats of data:" & vbCrLf & vbCrLf

msg = msg & "Mean: " & Format(.Mean, "#,##0.00") & vbCrLf

msg = msg & "Std Dev: " & Format(.StdDeviation, "#,##0.00") & vbCrLf

msg = msg & "5th percentile: " & Format(.PToX(0.05), "#,##0.00") & vbCrLf

msg = msg & "95th percentile: " & Format(.PToX(0.95), "#,##0.00")

MsgBox msg

End With

With .BestFit(RiskFitStatistic_AIC)

' Information about best fit

msg = "Information about best fit:" & vbCrLf & vbCrLf

msg = msg & "Distribution: " & .DistributionFunction & vbCrLf

msg = msg & "Mean: " & Format(.Mean, "#,##0.00") & vbCrLf

msg = msg & "Std Dev: " & Format(.StdDeviation, "#,##0.00") & vbCrLf

msg = msg & "5th percentile: " & Format(.PToX(0.05), "#,##0.00") & vbCrLf

msg = msg & "95th percentile: " & Format(.PToX(0.95), "#,##0.00")

MsgBox msg

' Graphs of best fit

.GraphFitComparison.ImageToWorksheet wsData, RiskImageFormat_JPG, 100, 50, 300,

250

.GraphPP.ImageToWorksheet wsData, RiskImageFormat_JPG, 420, 50, 300, 250

.GraphQQ.ImageToWorksheet wsData, RiskImageFormat_JPG, 740, 50, 300, 250

End With

End With

End With

End Sub

25

Figure 17 Fit Comparison Graph

The following code, is typical for a batch fit. The fit definition is now created with the AddBatch function

(not the Add function as above), and the properties of the fit definition now include a few properties

that pertain only to batch fits. The code also illustrates how you can restrict the distributions to be fit

with the EstimatedFitsSetList function, followed by an array of distribution names.

Sub BatchFit()

Dim distList(1 To 4) As String

' Delete named fit if it already exists

On Error Resume Next

Risk.Fits.Item("Cost_Fits").Delete

' Distributions to try

distList(1) = "Gamma"

distList(2) = "LogLogistic"

distList(3) = "Weibull"

distList(4) = "Lognorm"

' Set up and run a batch fit

With Risk.Fits.AddBatch(Range("Cost_Data"), RiskFitDataType_ContinuousSamples, "Cost_Fits")

' Batch fit properties

.BatchFitReportIncludeCorrelations = True

.BatchFitReportIncludeDetailWorksheets = True

.BatchFitReportInNewWorkbook = False

.BatchFitReportStyle = RiskBatchFitReportStyle_Standard

.BestFitSelectorStatistic = RiskFitStatistic_AIC

' Try only the distributions in the distList array

.EstimatedFitsList_SetArray distList

.PerformFit

End With

End Sub

26

Programming Tip: Using "Add" in a line "With" line

The above FitTest and BatchFit macros illustrate a very handy VBA programming construction you might

have missed, one that you will see throughout the XDK example files. Consider the following line:

With Risk.Fits.Add(Range("Cost_Data"), RiskFitDataType_ContinuousSamples, "Costs")

This line not only adds an item to a collection—a RiskFitDefinition object to the collection of

RiskFitDefinition objects—but it implicitly returns this RiskFitDefinition object so that you can access its

properties and methods directly in the With block. As a beginning programmer, you might find it more

natural to define an explicit RiskFitDefinition object, “set” it, and then work with the explicit object, as

follows:

Dim rFit As RiskFitDefinition

Set rFit = Risk.Fits.Add(Range("Cost_Data"), RiskFitDataType_ContinuousSamples, "Costs")

With rFit

This is fine, but these three lines are equivalent to the single line above, and the latter is more compact.

There are indeed times when you will need an explicit object variable (like rFit), so that you can use it

later in your code. But if you don’t need it, you should consider using the more compact version. By the

way, this tip applies to VBA programming for Excel, not just for @RISK.

Creating Filters

The @RISK Filter tool lets you “filter out” results that don’t meet certain conditions. There are two types

of filters, standard and iteration. A standard filter is useful when we want to look at only those values of

an output that satisfy a certain condition. For example, the following code adds a standard filter on an

output named "NPV" (for Net Present Value) output. The filter conditions are essentially that NPV is

negative, and the resulting graph appears in Figure 18. As in the @RISK user interface for filters, you

must first “do” something, usually add one or more filters or clear the filters, and apply the changes. For

example, if the .Clear line were not followed by the .ApplyChanges line, the filters in effect wouldn’t be

cleared; they would still be in effect.

Sub FilterTest_Standard()

With Risk.Simulation

' Run simulation

.Start

With .Results

' Add standard filter to the Net Present Value output.

With .Filters

.Add "NPV", RiskFilterType_Standard, RiskNegativeInfinity, 0, False

.ApplyChanges

End With

With .GraphDistribution("NPV")

.TitleMainText = "NPV Distribution, Negative Values Only"

.ImageToWorksheet ActiveSheet, RiskImageFormat_PNG, 320, 245, 300, 250

End With

With .Filters

.Clear

.ApplyChanges

End With

End With

End With

End Sub

27

The key to this code is the Add line. This adds a filter to the collection of filters currently in effect. Its

arguments are a reference to an output (or input), the type of filter (standard or iteration), minimum

and maximum values, and whether these are actual values or percentiles. If you wanted the values to be

percentiles, you could change the Add line to something like the following.

.Add "NPV", RiskFilterType_Standard, 0.25, 0.75, True

Technical Note: Infinity Constants

Note that the filter on NPV in the above code is really “less than or equal to 0.” However, both a lower

bound and an upper bound are required when adding this filter. For the lower bound, you can use

@RISK’s built-in constant RiskNegativeInfinity. A RiskPositiveInfinity constant is also available.

Figure 18 Graph of an Output with a Standard Filter

The VBA code for an iteration filter is virtually identical, as shown below, with the resulting graph in

Figure 19. However, it is important to understand what it is doing. In this example, two iteration filters

are added: one where the year 1 cost input is above its median and one where the year 1 revenue input

is below its median. Each iteration where both of these conditions hold is “marked,” and the requested

graph for the NPV output uses only the marked iterations—in this case, about 25% of them. It turns out

that the unfiltered mean NPV for this model is about 800. Obviously, the filtered mean is much lower.

Sub FilterTest_Iteration()

With Risk.Simulation

' Run simulation

.Start

With .Results

' Add iteration filters to outputs

With .Filters

.Add "Year1_Cost", RiskFilterType_Iteration, 0.5, 1, True

28

.Add "Year1_Revenue", RiskFilterType_Iteration, 0, 0.5, True

.ApplyChanges

End With

With .GraphDistribution("NPV")

.TitleMainText = "NPV Distribution, Filters on Year 1 Inputs"

.TitleDescriptionText = “Year 1 cost above median, Year 1 revenue below median”

.ImageToWorksheet ActiveSheet, RiskImageFormat_PNG, 320, 245, 300, 250

End With

With .Filters

.Clear

.ApplyChanges

End With

End With

End With

End Sub

Figure 19 Graph of an Output with an Iteration Filter on Two Inputs

Goal Seek Analysis

The Goal Seek tool in @RISK is similar to the Goal Seek tool in Excel, which forces the value of a formula

to a specified value by changing the value in an “adjustable cell.” @RISK’s Goal Seek tool is more flexible

because it lets you force a summary measure of an output, such as the mean, the standard deviation, or

a percentile, to a specified value.

The following code illustrates the basic possibilities. From Risk.Simulation, you first create a new Goal

Seek analysis with the NewGoalSeekAnalysis function. Then you specify the adjustable cell

(VariationCell), the output cell, the type of output statistic, and required values. You can set the number

of iterations to any value, but because several simulations will be run to “sneak up on” the best value of

the adjustable cell, a very big number of iterations may result in an unacceptable runtime. Then you use

the RunAnalysis function to run Goal Seek. This function returns True if a solution is found and False

29

otherwise, so an error check should be included. For example, there might not be any value of the cost

factor that makes the 25

th

percentile of NPV equal to 800.

Sub RunGoalSeek()

' Create new Goal Seek analysis

With Risk.Simulation.NewGoalSeekAnalysis()

' Goal Seek settings

Set .VariationCell = Range("Cost_Factor")

Set .OutputCell = Range("NPV")

.OutputStatistic = RiskStatisticType_Percentile

.OutputPercentile = 0.25

.OutputTarget = 800

' Small number of iterations for Goal Seek

Risk.Simulation.Settings.NumIterations = 500

' Run Goal Seek and check if a solution is found

If Not .RunAnalysis() Then

MsgBox "Goal Seek couldn't find a solution.", vbInformation

Exit Sub

Else

MsgBox "Cost factor that makes 25th percentile of NPV equal to 800 = " _

& Format(Range("Cost_Factor").Value, "#,##0.000")

End If

End With

End Sub

Advanced Sensitivity Analysis

The @RISK Advanced Sensitivity Analysis tool provides more sensitivity options than the usual tornado

or spider graphs. For example, it allows you to perform sensitivity analysis on fixed inputs, not just on

inputs with distribution functions.

The following code is typical. It is fairly long but straightforward. From Risk.Simulation, you use the

NewAdvSensitivityAnalysis function to create a new advanced sensitivity analysis. Next, you specify an

output and an output statistic to monitor, and you specify as many inputs as you like. In this example,

the first input is a fixed value and the other four are distributions. After that, you specify how you want

the inputs to vary. In this example, the fixed input varies from 0.05 to 0.15 in 5 steps, with a base value

of 0.1. The distribution-based inputs also vary over 5 steps, but they use their 10

th

, 25

th

, 50

th

, 75

th

, and

90

th

percentiles for varying. (Note how the VariationPercentiles_SetArray function takes an array as its

argument. This explains why the percent array is created.) Finally, you specify the report placement and

the reports you want, and you run the analysis with the RunAnalysis function.

Sub AdvSensAnalysisTest()

Dim inputCellBased As RiskAdvSensInput

Dim inputDistBased(1 To 4) As RiskAdvSensInput

Dim percent(1 To 5) As Double

Dim i As Integer

' Specify output and inputs

With Risk.Simulation.NewAdvSensitivityAnalysis

' Output to analyze

Set .OutputCell = Range("NPV")

.OutputStatistic = RiskStatisticType_Mean

' Input that isn't a distribution

Set inputCellBased = .Inputs.Add(RiskAdvSensInputType_CellBasedInput, _

Range("Discount_Rate"))

' Properties of cell-based input

30

With inputCellBased

.VariationMethod = RiskAdvSensVariationMethod_MinMaxRange

.BaseValue = 0.1

.VariationMinimum = 0.05

.VariationMaximum = 0.15

.VariationNumSteps = 5

End With

' Inputs that are distributions

Set inputDistBased(1) = .Inputs.Add _

(RiskAdvSensInputType_DistributionBasedInput, Range("Fixed_Cost"))

Set inputDistBased(2) = .Inputs.Add _

(RiskAdvSensInputType_DistributionBasedInput, Range("Revenue_Year1"))

Set inputDistBased(3) = .Inputs.Add _

(RiskAdvSensInputType_DistributionBasedInput, Range("Annual_Revenue_Change"))

Set inputDistBased(4) = .Inputs.Add _

(RiskAdvSensInputType_DistributionBasedInput, Range("Variable_Cost_Percentage"))

' Percentages used in variation of distribution-based inputs

percent(1) = 0.1:percent(2) = 0.25:percent(3) = 0.5:percent(4) = 0.75:percent(5) = 0.9

For i = 1 To 4

With inputDistBased(i)

.VariationMethod = RiskAdvSensVariationMethod_DistributionPercentiles

.VariationPercentiles_SetArray percent

End With

Next

' ReportPlacement

.ReportPlacement = RiskExcelReportPlacement_ActiveWorkbook

' Reports to include

.IncludeSummaryReport = True

.IncludePercentilesGraph = False

.IncludeBoxWhiskerPlot = False

.IncludePercentChangeGraph = True

.IncludeTornadoDiagram = True

' Run sensitivity analysis

.RunAnalysis

End With

End Sub

Stress Analysis

@RISK's Stress Analysis tool allows you to compare the results from a "base" model to one where one or

more inputs are "stressed," that is, where the values of these inputs are sampled from conditional

probability distributions instead of the original distributions.

The following code illustrates a typical stress analysis. It is in an insurance context, where the input is the

random Damage and the output is the loss to the insurance company, assuming a deductible amount

near the 70

th

percentile of the damage distribution. (Any other deductible amount could be used.) The

insurance company wants to see the distribution of its loss when really large damages occur. Starting

with Risk.Simulation, you create a new stress analysis with the NewStressAnalysis function. Next, you

add one or more inputs and specify their parameters. In this example, the Damage input is constrained

to be above its 90

th

percentile, so that the stress analysis will sample damages from the top 10

percent

of the damage distribution. Then you specify the output cell to monitor, the report placement, and the

desired reports. Finally, you run the analysis with the RunAnalysis function.

Sub StressAnalysis()

' Create new Stress analysis

With Risk.Simulation.NewStressAnalysis

31

' Define input and its parameters

With .Inputs.Add(Range("Damage"))

.StressMethod = RiskStressMethod_PercentileRange

.PercentileMin = 0.9

.PercentileMax = 1

End With

' Define output

Set .OutputCell = Range("Insurance_Company_Loss")

' Specify report placement and reports, and run analysis

.ReportPlacement = RiskExcelReportPlacement_ActiveWorkbook

.IncludeSummaryReport = True

.IncludeComparisonGraphs = True

.RunAnalysis

End With

End Sub

One of the resulting graphs from this analysis appears in Figure 20. It shows the distribution of the loss

to the insurance company for the original baseline model and the model with stressing. Obviously, the

losses in the latter tend to be considerably larger. In the baseline model, the company pays nothing

about 70% of the time, and it pays a positive amount 30% of the time. In the stressed model, the

insurance company always pays.

Figure 20 Box Plots of Insurance Company Losses for Baseline and Stressed Version

Automating RISKOptimizer

RISKOptimizer is totally integrated into @RISK. Nevertheless, it has its own XDK, with its own object

model. For example, the names of most RISKOptimizer objects start with “RiskOptimizer,” whereas

@RISK objects start with “Risk.” When you automate RISKOptimizer with VBA code, you only need to set

the usual references to RiskXLA and Palisade_Risk_XDK8.

32

There are plenty of objects, properties, and methods in the RISKOptimization Object Model, but the

“flow” is fairly straightforward. You start with the object RiskOptimization which could be found as a

property of the root object Risk. You can simply type Risk.Optimization to reference the RISKOptimizer

root object. Then you create an RiskOptimizerModelWorkbook object, and from it, you define the goal,

the adjustable cells groups, the constraints, and the optimization settings. Finally, after optimizing with

the line Risk.Optimization.Optimize, you can report optimization results.

The following code is typical. Here are the basic steps.

1. It uses the outer With block to create the RiskOptimizerModelWorkbook object (implicitly).

2. It specifies that the goal is to maximize the 5

th

percentile of the Ending_Value output.

3. It removes any previous adjustable cell groups and constraints, just in case.

4. It adds an adjustable cell group of the budget type. The range for this cell group is the

Investment_Weights range, its lower and upper limits are in the Min_Weights and Max_Weights

ranges, respectively, the next three optional arguments are omitted, and the last optional argument

indicates a step size of 0.005 for a discrete search.

5. It adds a hard constraint that should be enforced on each iteration. The arguments indicate that the

“APPL_CSCO_Pct” range should be within minimum and maximum values.

6. It changes some optimization settings.

7. It changes some simulation settings.

8. It runs the optimization and reports some results.

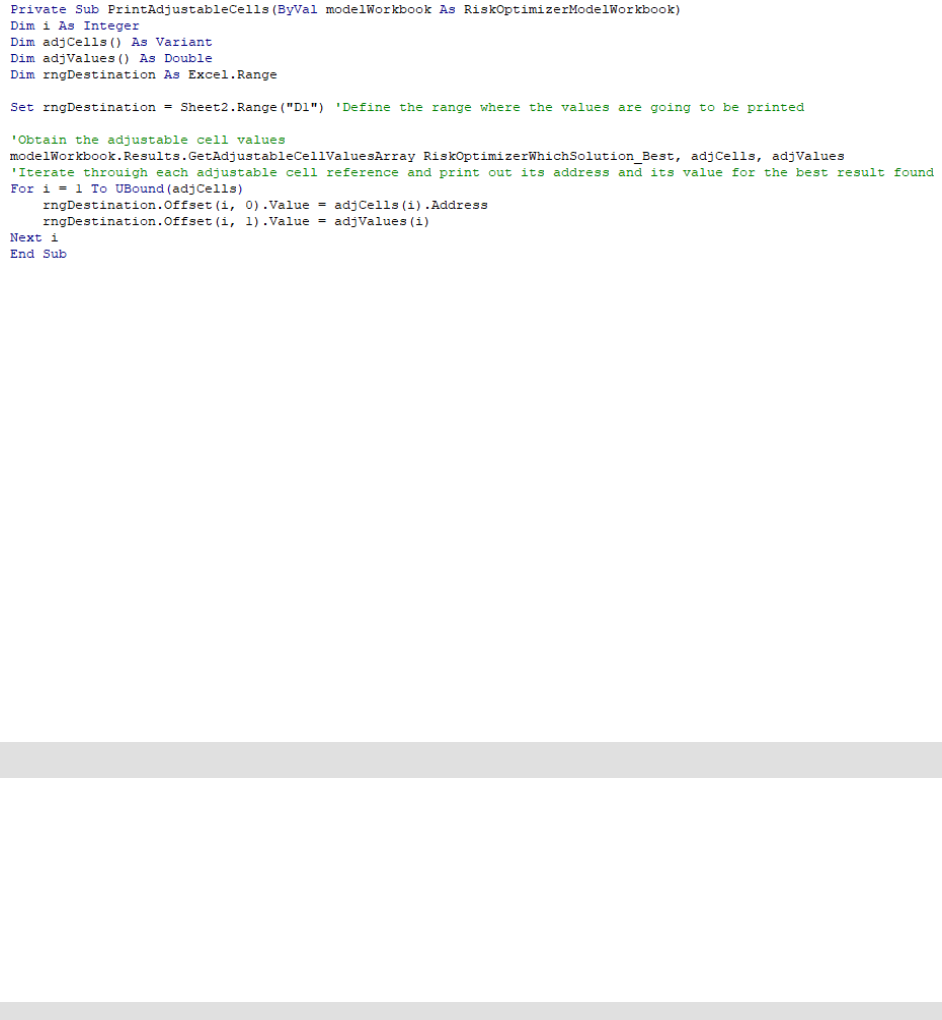

Sub RunRiskOptimizer()

Dim msg As String

' Optimization Model

With Risk.Optimization.ModelWorkbook(ActiveWorkbook)

' Goal

With .Goal

Set .CellToOptimize = Range("Ending_Value")

.StatisticToOptimize = RiskOptimizerStatistic_Percentile

.StatisticParameter = 0.05

.GoalType = RiskOptimizerGoalType_Maximize

End With

' Remove adjustable cells and constraints if any

.AdjustableCellGroups.RemoveAll

.Constraints.RemoveAll

' Add budget adjustable cell group

.AdjustableCellGroups.AddWithBudgetSolvingMethod.AdjustableCellRanges _

.AddForBudgetSolvingMethod Range("Investment_Weights"), _

Range("Min_Weights"), Range("Max_Weights"), , , , 0.005

' Constraint (just for illustration)

.Constraints.AddHardInSimpleMode RiskOptimizerConstraintEvaluationTime_EachIteration, _

Range("Min_APPL_CSCO"), RiskOptimizerConstraintOperator_LessOrEqual,

Range("APPL_CSCO_Pct"), RiskOptimizerStatistic_Value, _

0, RiskOptimizerConstraintOperator_LessOrEqual, Range("Max_APPL_CSCO"), "Limits for

APPL plus CSCO"

' Optimization settings

With .OptimizationSettings

.Engine.OptimizationEngine = RiskOptimizerEngine_Automatic

.Runtime.TrialCountStoppingCondition = True

.Runtime.TrialCount = 1000

End With

' Simulation settings

With Risk.Simulation.Settings

33

.NumIterations = 100

.AutomaticResultsDisplay = RiskAutomaticResultsDisplay_NoAutomaticResults

End With

' Run optimization

Risk.Optimization.Optimize

' Report selected results

With .Results

msg = "Time to optimize (seconds): " _

& Format((.FinishTime - .StartTime) * 24 * 60 * 60, "#,#00.0")

msg = msg & vbCrLf & "Best result: " & Format(.BestValueWithoutPenalties, "$#,#00")

End With

MsgBox msg

End With

End Sub

You can also use the RISKOptimizer XDK inside macros to obtain information about an optimization in

progress and control it, even if the model is set up and the optimization is started through the graphical

interface, not through VBA. For example, the following macro will stop the optimization if there is no

progress after 100 trials. (To ensure that this macro is called during the optimization, you need to specify

its name in the Macros tab of the Optimization Settings dialog).

Sub MyAfterStorageRoutine()

With Risk.Optimization.ModelWorkbook(ActiveWorkbook).Results

If .NumTrials >= 100 Then

If .BestValueWithPenalties = .OriginalValueWithPenalties Then

Risk.Optimization.OptimizationManager.StopOptimization

End If

End If

End With

End Sub

Technical Note: Multiple CPUs

Anytime you have code that runs in the middle of a simulation (e.g. a user-defined function or a

simulation macro) and uses anything in the @RISK object model, it is a good idea turn off the multiple

CPUs option. This can be done through the @RISK user interface: using the Settings button in the

Simulation section on the ribbon for regular simulations, or using the Advanced Tab of the Optimization

Settings dialog for optimizations; this can also be done via code.

The reason is that when multiple CPUs are used by @RISK, multiple copies of Excel can be launched to

run your simulation. Only the original Excel has access to the @RISK object model, and if one of the

copies tries to access the Risk object, an error will occur. Keep in mind that this doesn’t affect any code

you run before or after the simulation. It also isn’t an issue if your simulation macro or user-defined

function doesn’t call anything in the @RISK object library.

Some General VBA Tips

This guide concludes with a few VBA tips that you should know regardless of whether you are

automating @RISK or Excel.

File Format (xlsm)

If you save a workbook that includes VBA code, you must save it as a macro-enabled (.xlsm) file. This is

true for any Excel file that contains VBA code; it is not specific to @RISK files. Then if you open this .xlsm

34

file later on, you will be warned that it contains macros. Make sure you elect to enable the macros;

otherwise the VBA macros won’t work.

Running a Macro

If you develop a VBA program for nontechnical users, you probably won’t want them to see your code,

either for proprietary reasons or because it would be too intimidating. However, it is easy to create a

simple user interface for running the program. To do so, activate a worksheet, insert a shape such as a

rectangle, right-click it, select Assign Macro, and select your macro. You can also insert descriptive text,

such as Run Program, in the shape. From then on, a user can simply click the shape to run the program.

ThisWorkbook

You can always reference a workbook by name, as in Workbooks(“My Example File.xlsm”). Alternatively,

you can refer to the active workbook with the built-in object ActiveWorkbook. However, an even safer

reference is to ThisWorkbook, which always references the workbook containing the VBA code. (It is

safer than ActiveWorkbook because the workbook containing the code might not be active when you

run your program.)

Worksheet Code Names

The code in the example files sometimes references worksheets by their “code” names. A worksheet

actually has two names, the name you see on its tab, and a code name, which can be set only in the

Visual Basic Editor. This is illustrated in Figure 21 (see the highlighted line in the Properties section). In

this example, the notation wsModel (Model) in the Project section indicates that Model is the name on

the tab and wsModel is the code name. (Any names can be used for code names, but a common practice

is to use the prefix ws.) One reason for using code names in VBA programs is that you don’t need to

create a Worksheet object variable; you can simply write wsModel.Range(“A1”), for example. A second

reason is that if your code refers to the worksheet by name, as in Worksheets(“Model”), and someone

changes the name on the worksheet tab, an innocent enough change to make, this will break your

program. However, because code names can be changed only through the Visual Basic Editor, it is much

less likely that anyone will change them.

35

Figure 21 Code Name for Worksheet

With Blocks

In the XDK example files, you will see a lot of With blocks, sections that start with the keyword With and

end with the keyword End With. These are used by all good VBA programmers, so you should get used

to them. They allow you to avoid a lot of repetitive code, as illustrated by the following block of code.

Inside the With Risk.Simulation block, anything that starts with a period really has Risk.Simulation to

the left of it. For example, . Settings is equivalent to Risk.Simulation.Settings. As you can see, these

With blocks can be nested to avoid even more repetitive code. For example, .NumSimulations is

equivalent to Risk.Simulation.Settings.NumSimulations. It is a very good idea to indent these blocks

appropriately, as has been done here, for easier reading.

With Risk.Simulation

' Change some simulation settings

With .Settings

.NumSimulations = 3

.NumIterations = 5000

.AutomaticResultsDisplay = RiskAutomaticResultsDisplay_NoAutomaticResults

End With

End With

Intellisense

The reference to the @RISK library mentioned earlier is not only required to make your @RISK code

work properly, but it provides you with an invaluable programming aid: Intellisense. As an example,

consider the following line:

Risk.Simulation.Settings.AutomaticResultsDisplay = RiskAutomaticResultsDisplay_NoAutomaticResults

36

Could you remember all of this? Fortunately, you don’t have to. As soon as you type Risk. (including the

period), you will see a list you can choose from. Then when you choose Simulation from the list and

type a period, you will see another list to choose from. And so on. To cap it off, when you have entered

everything to the left of the equals sign and then type the equals sign, you will see a list of the

appropriate @RISK constants for the AutomaticResultsDisplay property that you can choose from. If you

are already an Excel programmer, you undoubtedly appreciate the power of Intellisense, and you will be

happy to know that it extends to VBA for @RISK. If you are not yet familiar with Intellisense, you are in

for a big treat!

Object Browser

A great source of information is the VBA Object Browser. To see this, make sure a file with a reference to

the @RISK library is selected in Project pane. Then select Palisade_Risk_XDK8 from the libraries

dropdown list. This Object Browser shows all of the @RISK objects on the left and all of their properties

and methods on the right. Also, when you select an item on the right, you get some limited help, such as

the list of a function’s arguments, at the bottom of the window. Remember that such help is only a few

mouse clicks away as you are doing your programming. It often provides just the detail you need to get

you past a programming hurdle.

Figure 22 Visual Basic Object Browser

37

Constants and Enumerations

The line .AutomaticResultsDisplay = RiskAutomaticResultsDisplay_NoAutomaticResults contains one

of many built-in @RISK constants, in this case, RiskAutomaticResultsDisplay_NoAutomaticResults. All of

these constants begin with Risk, and they all have integer values, such as 3 or 445. However, because no

person could ever remember these values, they are instead given meaningful names that programmers

can use in their VBA code. You can find the names in the Object Browser. For example, Figure 23 lists the

constants (on the right) for the four possible settings of the AutomaticResultsDisplay property.

Together, this set of four constants is called an enumeration. (Strictly speaking, the

AutomaticResultsDisplay property returns the RiskAutomaticResultsDisplay enumeration. This is only

one of several enumerations available in @RISK, indicated by the double-yellow icons in the figure.

5

)

Figure 23 RiskAutomaticResultsDisplay Enumeration

5

Excel also has many enumerations. Its built-in constants all begin with xl, as in xlDown, xlToRight, and so on.

38

@Risk XDK also includes some stand-alone constants that do not belong to enumerations, for example

RiskAutoNumIterations in this code:

With Risk.Simulation

' Change some simulation settings

With .Settings

' non-enumerated constant

.NumIterations = RiskAutoNumIterations

' enumerated constant

.AutomaticResultsDisplay = RiskAutomaticResultsDisplay_NoAutomaticResults

End With

End With

To find the non-enumerated constants in the Object Browser, we need to select RiskXLA as the library to

view, and then click XDK in the list of classes, as shown in Figure 24.

Figure 24 @Risk XDK Non-Enumerated Constants

39

Appendix

The document to this point contains all of the information you need to get started with VBA for @RISK.

This appendix contains extra information, some of which is rather technical, that might come in handy.

Updating @RISK 6.x or 7.x Automation Code to Run in @RISK 8.x

Overview

Moving to version 8, Palisade has reviewed and improved the XDK interface, taking into account new

features and the needs of .NET programmers. This resulted in some changes to the Object Model,

method names and parameters, and names of enumerated constants. The major changes are described

here in reference to VBA code, but not every detail is covered. In some cases when code created for

earlier versions does not compile in version 8, one may need to review the new interface to identify a

new way of accomplishing the same objective. Usually it will be possible to identify a similarly named

method or property that accomplishes the same task; or in some cases changes to code will be forced by

a modified list of method parameters in version 8. However, every effort was made to not change the

interface unless necessary, and over 90% of the interface is the same as in previous versions.

Updating Library References

If you have @RISK automation code written for @RISK 6.x or 7.x, you'll need to change the references as

described before in this guide for that code to work with @RISK 8.x.

Changes to the Object Model

• The Risk.Simulation.Results.Reports object has been added, reflecting improved reporting

functionality in version 8

• The Risk.ApplicationSettings object was replaced by the Risk.Preferences object, corresponding the

new method of handling user settings in version 8. Some properties may no longer be found in the

new object, while new ones have been added.

• The Risk.Library object is no longer available, corresponding to the changed form of this

functionality in version 8.

New Interface for Generating the Standard Reports

Version 8 improved the reporting functionality significantly, with new report types, the option of

generating reports in the PDF format, and flexibility in specifying which inputs/output to include in the

reports. Consequently, the single Risk.GenerateExcelReports method in version 7 was replaced by a

number of methods in the Risk.Simulation.Results.Reports object.

40

New Format of Enumerated Constant Names

There is a new format for names of enumerated constants in version 8, requiring some changes in VBA

code wherever an enumerated constant was used. It should be straightforward to identify the new

name of a constant, particularly that the names of the enumerations generally have not changed. For

example, "RiskAutomaticResultsDisplay.RiskNoAutomaticResults" in versions 6/7 became

"RiskAutomaticResultsDisplay.RiskAutomaticResultsDisplay_RiskNoAutomaticResults". In general, the

names of enumerations are included as prefixes in the names of the constants.

New Method of Returning Arrays

In version 8 arrays are returned differently to client code. For example, in version 7 to obtain all the

values an output had during a simulation, one called the GetSampleData method, with the array of