Fairness in Incomplete Information Bargaining:

Theory and Widespread Evidence from the Field

∗

Daniel Keniston, Bradley J. Larsen, Shengwu Li, J.J. Prescott,

Bernardo S. Silveira, and Chuan Yu

†

September 21, 2023

Abstract

This paper documents a robust pattern from diverse sequential bargaining settings:

agents favor offers that split the difference between the previous two offers. Our empirical

settings include used-cars, insurance claims, home sale, trade tariffs, a TV game show,

eBay, and auto-rickshaws. These even-split offers are more likely to be accepted, less

likely to spur exit by the opponent, and more likely to be followed by subsequent split-

the-difference offers if bargaining continues. We propose several theoretical frameworks

to explain this behavior, including an inference argument under which split-the-difference

offers can be viewed as an equal split of the potential surplus.

JEL Codes: C7, D8, D9

Keywords: Bargaining, negotiation, fairness, split-the-difference, incomplete informa-

tion, inference, alternating offers

∗

We thank Panle Jia Barwick, Kalyan Chatterjee, Peter Cramton, Jack Fanning, Emin Karagözoğlu, Ted

O’Donoghue, Marek Pycia, Al Roth, Caio Waisman, Alex Wolitzky, and seminar and conference participants

at LSU, UCLA, NYUAD, IACM, and BEET for helpful comments and suggestions. Wendy Yin provided

excellent research assistance. We thank an anonymous real estate brokerage, as well as I

˜n

igo Hernandez-Arenaz

and Nagore Iriberri, for providing data.

†

Washington University in St. Louis, Olin School of Business and NBER; [email protected]; Li: Harvard

School; jprescott@umich.edu; Silveira: UCLA Department of Economics; [email protected]; Yu: Stanford

1 Introduction

The role of fairness notions in bilateral bargaining has been widely accepted by practitioners

and explored in depth in laboratory experiments. A number of studies document such

influences, in particular demonstrating a bias toward an equal split of a known pie; see

Camerer (2011) for a review. Little is known, however, about how these norms play out in

the field, where assumptions of complete information common in laboratory experiments

are unlikely to hold. In this paper, we document a largely understudied fact: agents in

real-world sequential bargaining settings favor offers that split the difference between the

two most recent offers on the table.

The term split the difference appears in previous research (especially experimental work)

on bargaining with different meanings. Binmore et al. (1989), for example, use it to describe

bargaining outcomes in which the players divide a known surplus net of their respective

outside options. In the present paper, similar to Bochet et al. (2023) and Backus et al.

(2020), splitting the difference refers instead to a notion in a sequential-offer game where the

current bargaining offer lies at the midpoint between the two most recent offers (the most

recent offer of the proposer and the most recent offer of the counterparty). As an example,

suppose that in an alternating-offer game, at some point when it is the seller’s turn, the

seller proposes $100, then the buyer proposes $50, and then it is the seller’s turn again. We

refer to the $100 and $50 offers as the two most recent offers, and, if the seller next proposes

$75, we refer to this as a split-the-difference offer.

Our empirical evidence comes from novel, detailed data on sequential offers from several

vastly different bargaining contexts: business-to-business negotiations for used cars in

the U.S., pre-trial settlement bargaining on insurance injury claims in the U.S., street

negotiations from a quirky TV game show in Spain, bargaining for auto rickshaw rides in

India, international trade tariff bargaining, online retail negotiations from eBay.com, and

bargaining over housing through a real estate dealer. In each setting, we find strong evidence

of split-the-difference offers—a clear mode at the 50-50 point between the two most recent

offers. To our knowledge, the widespread nature of this phenomenon—across very different

bargaining settings—was previously undocumented.

1

1

Our motivation for selecting these particular settings is simple: we use every dataset available to us in

which all back-and-forth offers are recorded, because only with such data can we examine split-the-difference

behavior. Only recently did researchers start using this type of detailed bargaining data. As such, split-

the-difference offers have been naturally understudied thus far, and several of the datasets we study are

1

We find that split-the-difference offers are more likely to be accepted: as an agent

concedes more to the opponent, the agent’s offer is generally more likely to be accepted; this

probability, however, jumps discontinuously at offers that lie halfway between the two most

recent offers, to the extent that a split-the-difference offer is even more likely to be accepted

than a slightly more generous offer that concedes more than half of the distance between

offers.

2

Similarly, offers that split the difference are less likely to result in the opponent

walking away, ending the negotiations.

In the same vein, we show that certain agents are more likely than others to make

split-the-difference offers, and that a seller is less likely to propose a 50-50 split if one of the

two most recent offers is an extremely low buyer offer—suggesting that the 50-50 norm is

constrained by the disparity between the two previous offers.

We also demonstrate that it is indeed the two most recent offers in a bargaining sequence

to which players gravitate: proposing an offer at a later stage of the game that splits

the difference between offers other than the previous two is far less common. Similarly,

split-the-difference offers are substantially more prevalent than offers based on anchor points

that are privately known to the proposer, such as the secret auto-accept and auto-decline

prices set by the seller in the eBay setting or the loss estimate set by the defendant in the

insurance settlement setting. That is, agents systematically split the difference between the

previous two offers, which are common knowledge, and thus engage in a behavior that is

subject to the scrutiny of all agents involved.

Having demonstrated that split-the-difference offers are ubiquitous, we ask what model

could explain this behavior. The prevalence of equal splits of a commonly known surplus has

been widely established in lab experiments. Researchers often attribute these patterns to

fairness-related norms.

3

But it is far from obvious that the patterns that we document are

new to the literature. The housing dataset is completely new. The used-car dataset is largely new; Larsen

(2021) uses some observations from this same setting, but here we take advantage of a larger dataset and

more information on alternating offers that Larsen (2021) does not use. The data on pre-trial settlement

negotiations is also largely new; Prescott et al. (2014) study a small subset of this data to examine high-low

contracts in litigation. Data on auto rickshaw rides comes from Keniston (2011), data on the Spanish TV

show comes from Hernandez-Arenaz and Iriberri (2018), international tariff negotiation data comes from

Bagwell et al. (2020), and the eBay data was first analyzed by Backus et al. (2020).

2

This finding bears a close resemblance to results from the experimental literature on ultimatum games

showing that (i) respondents are more prone to accept equal divisions of the pie than divisions that are more

favorable to the respondent (Bellemare et al., 2008); and (ii) respondents are discontinuously more likely to

accept 50-50 offers (Lin et al., 2020).

3

50-50 splits are a common outcome in relatively simple experiments, such as those involving the dictator

and ultimatum games, as well as in less structured bargaining studies allowing the subjects to freely negotiate

over the division of a pie. For excellent reviews of this vast literature, see Roth (1995) and Camerer (2011).

2

associated with fairness, as the surplus in our setting depends on agents’ private information.

In principle, split-the-difference offers are “fair” only in the sense that they lie halfway

between the possible range of likely subsequent offers given the current offer history; they

do not necessarily constitute an equitable split of the actual surplus available to the agents.

In fact, unless both parties have made offers that differ by exactly the same amount from

their true valuations, splitting the difference between offers cannot yield an equal split of

the surplus.

We introduce several theoretical results to explore this question in the context of a

bargaining game with alternating offers and two-sided private information. In this context,

we first show that a pattern of split-the-difference offers may arise in a perfect Bayesian

equilibrium even when the players have no preferences for “fair” outcomes. However, this

equilibrium is far from being unique. Thus, while split-the-difference offers are consistent

with “standard” game theory, they are by no means predicted by it.

We then propose an explanation for how agents may indeed view an equal split of the

two most recent offers as “fair.” Our argument relies on agents making inferences about the

support of their opponent’s valuation based on the fact that the opponent did not accept

the agent’s previous offer. Consider a case where a seller initially proposes a price of $100.

The buyer rejects this offer and counters at $50. What can the seller infer about the buyer’s

valuation from the fact that the buyer rejected $100? We show that, for all buyer types

(i.e., buyers with some valuation) below $100, rejecting the $100 offer is a sequential best

response (see Battigalli and Siniscalchi 2002) to every belief that the buyer may hold about

the seller’s type. And we show that, for all buyer types above $100, accepting is a sequential

best response to some belief a buyer could hold. In this sense, $100 is the highest buyer

type that the seller cannot rule out (1) based on the buyer’s rejection of $100, and (2)

under the assumption that the seller knows the buyer is behaving rationally according to

some belief. A similar argument applies to the buyer’s inference about the seller’s valuation

if the seller rejects the buyer’s counteroffer of $50. Together, these arguments offer an

explanation for how a buyer and a seller might jointly view the gap between the two most

recent offers—[50

,

100]—as the potential surplus; and hence an offer of $75, halfway between

the two most recent offers, can be viewed as “fair,” an equal split of the potential surplus.

We also discuss a number of other possible explanations for split-the-difference behavior.

3

Two existing studies within economics analyze a similar notion of splitting the difference.

4

Backus et al. (2020) provide descriptive evidence of several facets of eBay bargaining,

documenting the prevalence of split-the-difference offers being made and accepted on eBay.

We incorporate their data as one of our seven settings, and we adopt their framework as

a starting point for our analysis.

5

Bochet et al. (2023) design a lab experiment in which

agents with private information negotiate over multiple issues. The authors find that an

alternating-offer regime arises endogenously, with proposals frequently splitting the difference

between the two most recent offers whether agents negotiate over single items or bundles.

We complement the analyses of these two papers by establishing that split-the-difference

offers constitute a convention—not an ironclad convention, but a notable convention—among

bargainers in the field, and that this behavior is not unique to consumer interactions nor to

U.S. negotiation culture. Similarly, this is not a feature of small-stakes negotiations only; it

also appears in home sales, the largest lifetime purchase for many buyers. Moreover, our

paper establishes a possible grounding for why such behavior could be viewed as “fair” in

some sense—even though the two most recent offers are themselves endogenous equilibrium

objects and thus the halfway point does not actually correspond to an equal split of the

pie. But we stress that we do not view this model as the only possible explanation for the

behavior.

Outside economics, the negotiation literature broadly acknowledges the norm of “even-

split” offers, although it contains differing assessments of the effectiveness of the strategy.

Some authors (Babcock and Laschever, 2008) argue that “split the difference is a tactic that

often works extremely well” (p. 212), while others (Thompson, 2020) discourage even-split

offers, a perspective exemplified by the best-selling guide to negotiation titled Never Split the

Difference (Voss and Tahl, 2016). Nevertheless, the negotiation literature universally argues

that split-the-difference offers operate through an appeal to fairness that may increase the

4

Many experiments in the lab involve alternating-offer bargaining, but they do not address the questions

we study in this paper; see, for example, Binmore et al. (1985), Ochs and Roth (1989), and Binmore et al.

(1989). These experiments have investigated issues such as time discounting and the relevance of outside

offers in bargaining. Andreoni and Bernheim (2009) focus on bargaining with complete information and

offer a model and experimental results demonstrating how an equal split of a known pie can arise from a

preference to appear equitable (a concern for social image). Other related studies include Roth and Malouf

(1979) and Roth (1985).

5

Several other studies have also examined this same eBay bargaining data, such as Green and Plunkett

(2022), who analyze how well human agents perform relative to reinforcement learning bots coded to respond

optimally to observed actions in the data, and Freyberger and Larsen (2021), who estimate a structural

model bounding private valuation distributions and bargaining inefficiency.

4

probability of an offer being accepted by one’s bargaining partner.

6

Popular negotiation

advice echos this motivation: Kwame Christian, lawyer and founder/CEO of the American

Negotiation Institute, a consulting firm offering training and coaching in negotiation, argues

that the primary benefit of a split-the-difference offer is that “it can trigger reciprocity and

convey a sense of fairness.”

7

Overall, we view our primary contribution as documenting a stylized fact that may

discipline the bargaining literature in developing more reasonable models. Theoretical

bargaining models in economics make predictions about a range of things, such as the split

of surplus, delay, and the sequence of offers. Until recently, there have been few (or no)

real-world datasets containing back-and-forth offers with which a researcher could assess

the most important stylized facts regarding the path of play. Our paper documents one

particular set of patterns and demonstrates that they are ecologically robust, in the sense

that they emerge in many, very different situations. Given this breadth of applicability, and

given that canonical equilibrium models do not predict these patterns, we suggest that it

would be wise for bargaining theory to attempt to account for them. Likewise, most existing

structural estimation analyses of bargaining models omit systematic behavioral patterns

such as preferences for splitting the difference. This is the case of workhorse empirical

models that rely on various forms of Nash bargaining (e.g., Crawford and Yurukoglu, 2012,

and subsequent papers), as well as of the majority of studies that bring to the data models

of incomplete information bargaining (e.g., Keniston, 2011; Silveira, 2017; Larsen, 2021).

By accounting for the split-the-difference behavior that we document, future iterations of

these analyses could yield more realistic estimates and increase the accuracy and reliability

of policy takeaways.

Our study also relates to recent work by Camerer et al. (2019) and Huang et al. (2020),

which examine incomplete-information bargaining in an experimental setting. We elaborate

in Section 5.3 how our results shed light on their findings, offering insight as to how,

even in incomplete information settings, agents’ behavior is consistent with a notion of

6

Thompson (2020)’s negotiation textbook captures the tension between even-split offers and an even

division of surplus: “even-split between whatever two offers are currently on the negotiation table ... has an

appealing, almost altruistic flavor to it. So what is the problem with even splits? ... the pattern of offers up

until that point was not ‘equal.”’

7

https://www.forbes .com/sites/kwamechristian/2023/03/26/splitting-the-difference-in-neg

otiation-a-double-edged-sword/?sh=30ecfa152db5

. Like the academic literature, popular advice differs

when it comes to splitting the difference. Christian writes, “Although some may say never split the difference,

there may be situations where the maneuver has validity.”

5

fairness. Finally, our analysis contributes to a literature that studies behavioral phenomena

in bargaining using real-world data, such as Pope et al. (2015), studying focal points, or

Jiang (2022), studying left-digit bias.

The rest of the paper is organized as follows. Section 2 describes each of our data

settings, and Sections 3–4 contain our empirical results documenting the prevalence of

split-the-difference offers and related patterns. Section 5 explores several theoretical results

and Section 6 concludes.

2 Description of Field Settings

We now introduce the field settings from which we obtain our bargaining data. A benefit

of the question we study in this paper—how the current offer in a sequential bargaining

game relates to the two most recent offers—is that we can address the question in each of

these field settings even though the products or outcomes over which agents negotiate differ

drastically from setting to setting. In particular, in each setting, we observe data on many

bargaining sequences (which we also refer to as threads) and, for each sequence, we observe

the full set of sequential offers between negotiating parties. We consider an observation to

be an offer triple: the current offer and two preceding offers.

We drop from every dataset any bargaining sequences in which there are fewer than

three offers. We drop any threads that continue beyond the point where an agent makes

an offer exactly equal to the opponent’s previous offer (which logically should have ended

the game in agreement). We also drop any sequences in which an offer lies outside the two

most recent offers or cases in which a seller’s offer lies below a buyer’s offer.

8

We describe

additional cleaning steps in Appendix B.

2.1 Business-to-Business Used-Car Bargaining

The first dataset comes from the U.S. wholesale used-car industry. In this market, owners of

used-car dealerships buy vehicles from other dealerships as well as from large companies,

such as Hertz (rental cars), Wheels (a fleet company), Bank of America (selling off-lease

8

Such behavior likely corresponds to misrecorded data or to cases where some feature of the bargaining

environment changes prior to the current proposed offer, such as the arrival of additional information or a

new outside option for an agent. Dropping such threads eliminates fewer than 2% of observations in most

data settings, but as many as 24% in some data settings where the arrival of new information or misrecorded

offers may be more prevalent. We discuss this in Appendix B.

6

or repossessed vehicles), or Ford (selling lease buy-back cars). All negotiating agents are

professionals or businesses experienced in these negotiations. This $80 billion industry

underlies the supply side of the used-car market in the U.S., trading 15 million cars annually;

similar platforms exist internationally. For each car, an auction house runs a secret-reserve-

price ascending auction, followed by bilateral bargaining between the seller and the highest

bidder if the auction price falls short of the reserve price. The data we use in our analysis is

generated during this post-auction bargaining stage.

The dataset comes from six auction houses from January 2007 to March 2010. It records

each distinct attempt to sell the vehicle through the mechanism, and, for each attempt,

every alternating offer proposed by either the buyer or the seller, as well as the outcome

of the bargaining. This data overlaps in part with the data used in Larsen (2021), but

it also contains additional bargaining sequences that were dropped in that analysis. This

new inclusion highlights a major benefit of our empirical approach: the structural exercise

of Larsen (2021) required careful data cleaning and controlling for heterogeneity in the

items over which the parties negotiated, whereas our approach only requires looking at

split-the-difference patterns between offers in a given bargaining sequence, regardless of

heterogeneity across items.

Descriptive statistics for this dataset are shown in the first column of Table 1. This

dataset consists of 21,734 total bargaining sequences and 33,356 observations (offer triples).

Bargaining in this market begins if the auction price is below the reserve price, in which case

the auction price becomes the first offer in an alternating-offer bargaining game. The seller

can choose to accept the auction price, propose a counteroffer, or quit (ending the game).

The bargaining process is typically wrapped up within a day, with an average of several

hours between each offer. The average first offer (auction price) is $7,444, followed by an

average counteroffer from the seller of $8,918. The average number of offers in a sequence in

the used-car sample is 3.53 and the average last price offered is $8,072.

9

The negotiation

ends in agreement 59% of the time, at an average accepted price of $7,987. The

γ

t

objects

reported in Table 1 are defined and discussed in Section 3.

9

As highlighted at the beginning of Section 2, for every data setting, our analysis conditions on bargaining

sequences that include at least three offers.

7

Table 1: Descriptive Statistics of Bargaining Settings

Cars Settlement TV Show Rides Housing Trade eBay

# Threads 21,734 74,356 204 2,058 176 44,048 6,976,776

# Offer Triples 33,356 208,463 714 2,986 176 46,985 9,789,903

Rounds 3.53 4.80 5.50 4.32 3.00 3.07 3.40

Pr(Agree) 0.59 0.94 0.91 0.39 0.73 0.08 0.29

First Offer $7,444 $36,391 e19.50 |51.69 $460,849 0.00 $151.06

Second Offer $8,918 $64,042 e124.27 |36.73 $430,071 69.60 $88.71

Final Offer $8,072 $24,728 e56.67 |39.50 $451,248 38.30 $122.70

Accept Price $7,897 $21,838 e55.37 |42.54 $469,658 24.29 $91.40

γ

3

0.39 0.29 0.32 0.28 0.71 0.44 0.42

γ

4

0.18 0.43 0.31 0.24 0.26 0.38

γ

5

0.38 0.29 0.25 0.18 0.33 0.23

γ

6

0.14 0.39 0.28 0.16 0.31

γ

7

0.33 0.30 0.19 0.17 0.19

γ

8

0.12 0.38 0.34 0.27

γ

9

0.45 0.32 0.09

γ

10

0.00 0.38 0.38

Notes: Table shows the number of sequences/threads and number of offer triples in each data setting, as well as

averages for several variables in the data. For t ≥ 3, the variable γ

t

denotes the average concession weight in

bargaining round t, as defined in Section 3. The units for the average first, second, final, and accept prices are euros

for the TV Show and Indian rupees for the Rides setting. The trade setting combines offer sequences in which the

units are percentages and sequences where the units are a currency. Units are unimportant for our analysis, which

relies on the unit-less γ

t

weights.

2.2 Pre-trial Settlement Bargaining from Insurance Claims

The second dataset comes from pre-trial settlement bargaining over injury claims made

under U.S. auto and general liability insurance policies.

10

This dataset consists of extensive

proprietary information about all claims made to a large national auto and general liability

insurer that closed between January 1, 2004, and March 31, 2009. The data contains details

about the underlying accident, the alleged injury, the involved parties, the insurance contract,

and all attempts by the parties to resolve the associated dispute.

In these insurance cases, an injured person alleges that an injurer caused harm covered

by the insurer’s policies. If a claimant asserts damages within policy limits or declines to

pursue the insured individually for any excess—or if the insurer agrees to cover any damages

in excess of the insurance contract’s policy limit, which effectively it must do to act in “good

faith” if it turns down a demand by the claimant for the policy limit or less—the insurer

effectively replaces the injurer as the claimant’s counterparty in any dispute, which occurs

10

Prescott et al. (2014) study a small subset of this information, but the data we use in this paper—

particularly the bargaining threads—remains largely unexplored.

8

in virtually all cases. Under these circumstances, the claimant and the insurer bargain over

the amount that should be paid by the insurer to the claimant. This process can take many

months to reach a conclusion. If the two parties cannot reach an agreement, the claimant

will often pursue litigation, with the claimant (now plaintiff) filing a complaint in court

demanding damages against the insurer (now defendant). The parties may also negotiate

and settle the claim during the litigation stage. Importantly, the insurer records the amount

of each back-and-forth proposal made by either the insurer or the claimant and whether the

parties reach an agreement in these negotiations.

After cleaning, our sample contains 74,356 bargaining threads and 208,463 offer triples.

Table 1 shows that the average first offer is $36,391, followed by a counteroffer of $64,042

from the opposing party, and an average final offer of $24,728. The negotiations include 4.8

offers on average and end in agreement 94% of the time, at an average accepted price of

$21,838. This number is not between the average first and second offers because of a feature

of negotiations in this setting: the first offer may come from the claimant or the insurer,

and, in computing the average first and second offers, Table 1 pools over these two cases.

11

Appendix B discusses this point in more detail and describes how we clean the data to form

alternating-offer sequences.

2.3 Street Bargaining from a TV Game Show in Spain

The third dataset comes from a TV game show in Spain titled Negocia Como Puedas

(roughly, “Bargain However You Can”) analyzed in Hernandez-Arenaz and Iriberri (2018).

This data was generated in the streets of several major Spanish cities in summer 2013. In a

typical episode of the show, the host approaches individuals in the street and invites them

to participate in the game. Upon acceptance, an individual (the proposer) is endowed with

a potential pie of 100 euros and is asked an easy question. The proposer is not allowed

to answer the question herself. Instead, she must, within a three-minute limit, (i) find a

passer-by (the responder) able to provide an answer to the question that the proposer finds

satisfactory, and (ii) negotiate a price that the proposer will pay the responder to be able to

use that answer.

If the negotiations succeed and the responder’s answer to the original question is correct

11

Examining these two cases separately, the average accepted price is indeed between the average first and

second offers.

9

(as determined by the host), the proposer pays the responder the agreed amount. The

proposer then moves on to a new question, referred to as a new stage of the game, where

the process is repeated. In the new stage, the size of the pie increases (by 200 euros in the

second stage, 300 in the third, and 1,000 in the fourth). In any stage of the game, if the

proposer does not reach an agreement within the three-minute time limit, the game ends,

and the proposer gets nothing. Throughout the game, the size of the pie is only known to the

proposer, not the responder. In any given stage of the game, the bargaining is unstructured,

but the negotiations typically follow an alternating-offer structure, with the proposer making

the first offer. We only keep those threads in which offers clearly alternate between parties.

Additional details on the cleaning of the data are found in Appendix B.

In the data, we have 204 sequences and 714 offer triples. Table 1 shows that the average

first offer is 19.5 euros, followed by an average second offer of 124.3 euros and an average

final offer of 56.7 euros. The game ends in agreement most of the time (91%), after an

average of 5.5 rounds and at an average accepted price of 55.4 euros.

2.4 Auto Rickshaw Rides Bargaining in India

The fourth dataset comes from the local transportation market by auto rickshaw in Jaipur,

India. An auto rickshaw is a form of three-wheeled mini-taxi, officially capable of carrying

three passengers in a semi-enclosed back seat. Auto rickshaws are the primary means of

rented transportation in Jaipur. During the period in which Keniston (2011) collected the

data (January 2008 to January 2009), all prices were set by negotiation.

The data was collected by surveyors (whom we also refer to as buyers) who followed one

of two possible protocols. In real bargaining, buyers were assigned to travel by auto rickshaw

along fixed routes through the city, bargaining for the price of each ride. At the beginning of

each route, buyers were paid a lump sum slightly higher than the expected cost of the route

and were allowed to keep any money not spent on auto rickshaw fares. At the end of their

assigned trip, they were free to return to their homes or alternate employment. Thus, their

financial incentives and cost of time were similar to real trips taken for personal purposes. In

scripted bargaining, buyers negotiated with sellers according to a written bargaining script

(prepared by Keniston) consisting of a sequence of pre-determined counteroffers. Scripted

surveyors were instructed to act as if they were bargaining in a realistic manner so that

drivers (whom we also refer to as sellers) would respond as naturally as possible. After the

10

conclusion of the bargaining, surveyors wrote down the series of offers made by the drivers

and themselves. Drivers were not aware that they were part of a field experiment. The

average negotiation took 55 seconds to complete.

In our analysis, we exclude any offers or responses that come from scripted surveyors, as

they do not represent actual reactions. Additional details on data cleaning are in Appendix

B. Our main sample consists of 2,058 bargaining threads and 2,986 offer triples. Table 1

demonstrates that the average first offer is 52 rupees, followed by an average counteroffer

of 37 rupees and a final offer of 40 rupees. Negotiation concludes after an average of 4.32

offers, ending in agreement 39% of the time at an average accepted price of 43 rupees.

2.5 Bargaining in Residential Real Estate

The fifth dataset we use is new to the literature and comes from a growing residential

real estate brokerage company that offers discounted agency fees of 2–3% rather than the

traditional 6%. We collected this dataset in collaboration with the company, covering a

number of houses on the market from 2015 to 2019 in Colorado. This dataset differs from

the others we analyze in that we only observe offers placed by potential buyers, not by the

seller. The company informs us that seller counteroffers are indeed quite rare in this market.

Rather, the typical negotiation proceeds with a seller list price (which we treat as the first

offer) followed by sequential offers from the buyer. For a given home, we observe the seller’s

list price and each offer placed by potential buyers. The time on the market for a given

home can be several weeks or several months. In this setting, we consider split-the-difference

behavior to be cases in which a buyer makes an offer and then, if that offer is rejected,

subsequently makes an offer that splits the difference between the list price and the buyer’s

initial offer.

Table 1 shows that our sample has 176 threads and the same number of offer triples.

This feature is by construction: our main object introduced in Section 3 cannot be defined in

cases where one party makes three consecutive offers; thus, we only keep the seller’s list price

and the first two offers from the buyer, i.e., one offer triple for each bargaining sequence.

These bargaining sequences end in agreement 73% of the time. Bargaining begins with an

average list price of $460,849, followed by an average second offer of $430,071, and a final

offer of $450,248. When parties agree, they end at an average price of $469,658. Additional

details on data cleaning are found in Appendix B.

11

2.6 International Trade Tariff Bargaining

The sixth dataset contains detailed information on international trade negotiations recently

declassified by the World Trade Organization (WTO). In these negotiations, countries

bargain over commitments on their respective import tariffs. Despite the multilateral nature

of both the WTO and its predecessor, the General Agreement on Tariffs and Trade (GATT),

the negotiations are mostly bilateral, with individual country pairs making requests and

offers over the tariff for a specific tariff-line (a product code).

We use the dataset of Bagwell et al. (2020), which comprises the Torquay Round (1950–

1951). This data includes 298 bilateral bargaining pairs from 37 countries, negotiating

tariffs over thousands of tariff-line products. A bargaining thread is defined as two countries

(proposer and target) negotiating a tariff over a tariff-line product. In each thread, we observe

all requests from the proposer and offers from the target. As documented in Bagwell et al.

(2020), relatively few back-and-forth offers and counteroffers take place in any given thread.

For our analysis below, we consider whether a proposer requests a tariff that splits the

difference between a zero tariff and the existing tariff (the status quo before the negotiations).

To map the possibilities of a zero tariff and existing tariff into the same framework as the

other data settings, Table 1 considers a zero tariff as the de facto initial request from the

proposer (and, indeed, a zero tariff is frequently an actual request made in this setting).

Similarly, Table 1 considers the existing tariff as the initial offer from the target (the row

of “second offer”). We discuss this point further in Section D. All subsequent requests and

offers are also recorded in the data.

Table 1 shows that the sample consists of 44,048 bargaining sequences and 46,985 offer

triple observations. The game proceeds for 3.07 offers on average, ending in agreement 8%

of the time. Note that here we combine sequences in which the units are percentages and

sequences in which the units are a currency; thus, we provide no units on these averages of

offers in Table 1 and their values are hard to interpret. However, units are unimportant for

our analysis, which relies on the unit-less

γ

t

weights (described in Section 3). Additional

details on data cleaning are found in Appendix B.

12

2.7 Bargaining on eBay’s Best Offer Platform

Our final field setting comes from eBay’s Best Offer negotiation platform. eBay is well known

as a platform for buying and selling via auctions or fixed prices. Less well known is the

bargaining mechanism on eBay, through which a buyer and seller negotiate via alternating

offers (limited to three offers by each party). The game begins with the seller posting a

list price. An interested buyer can pay this price or make an offer. Offers are sent through

the eBay platform, and the receiving party has 48 hours to respond by either accepting,

declining, or proposing a counteroffer. Our data comes from internal data collected by Larsen

and coauthors for a separate project (Backus et al. 2020), and it consists of all bargaining

sequences placed by buyers and sellers on eBay (regardless of the product) from June 2012

through May 2013.

The sample consists of 6,976,776 bargaining sequences, comprising 9,789,903 offer triple

observations. These sequences contain an average of 3.4 offers. The average list price is

$151, the average second offer is $89, and the average final offer is $123. When trade occurs

(which happens 29% of the time), the final agreed-upon price is $91.

3 Split-the-Difference Offers are Widespread

We now demonstrate a key empirical pattern: agents favor offers that split the difference

between the two most recent offers. To show this, we first introduce some useful notations.

For each data setting, we organize each sequential bargaining thread in the following way, as

in Backus et al. (2020). For each round

t

= 1

,

2

, ...

in the bargaining thread

j

, we observe

the proposed amount,

p

j,t

. This proposed amount is an offer made by the seller/buyer,

insurer/claimant, proposer/respondent, driver/surveyor, proposer/target, etc. If

p

j,t

comes

from one player,

p

j,t+1

must come from the opponent—with the exception of threads in the

housing dataset, as we note above and explain further later in this section.

We can write the proposed amount in round

t ≥

3 as a weighted average of the proposed

amount in the previous two rounds:

p

j,t

=

γ

j,t

p

j,t−1

+ (1

− γ

j,t

)

p

j,t−2

. Therefore,

γ

j,t

represents, for bargaining thread

j

, the weight that the player in round

t

places on the

opponent’s previous offer, and 1

− γ

j,t

represents the weight the player places on her own

previous offer. We can think of

γ

j,t

as how much a player concedes to her opponent when

13

she is making a counteroffer, or her concession weight. Rearranging to solve for γ

j,t

yields

γ

j,t

=

p

j,t

− p

j,t−2

p

j,t−1

− p

j,t−2

. (1)

In particular, a split-the-difference offer corresponds to γ

j,t

= 0.5.

As highlighted in Section 2.5, in the housing dataset, we observe a seller’s list price and

a given buyer’s offers, and in no bargaining thread does the number of offers from the same

buyer exceed two. In this setting, we only define the concession rate for the second buyer’s

offer. Specifically, we let

γ

j,3

=

p

j,3

− p

j,2

p

j,1

− p

j,2

, (2)

where

p

j,1

is the list price,

p

j,2

is the buyer’s first offer, and

p

j,3

is the buyer’s second offer.

Thus, in the housing dataset,

γ

j,3

represents the weight a buyer places on the list price, and

1 − γ

j,3

represents the weight she places on her own initial offer.

The advantage of focusing on concession weights is that they are unit-less and do not

require considering any heterogeneity across negotiation threads. Table 1 shows the average

γ

j,t

for each round of the game, beginning with

t

= 3. We observe as many as ten

γ

j,t

’s in

some settings,

12

and, as highlighted above, only the round-3

γ

j,t

in the housing setting. The

average

γ

j,t

in each round is below 0.5 (other than for housing, where it is 0.71), suggesting

that most agents make offers closer to their own previous offers than to their opponent’s. In

the settlement data, the average

γ

j,t

is roughly 0.3–0.4 in every round of the game, whereas

in the cars setting,

γ

j,t

tends to be much smaller in even rounds, which correspond to the

seller’s turns, suggesting that sellers generally concede less than buyers in this context.

The main pattern we wish to examine is whether agents in each of these settings exhibit

a tendency to make offers that lie halfway between the two most recent offers on the table

(i.e.,

γ

j,t

close to 0.5). Figure 1 plots a histogram of these concession weights, with each

panel corresponding to one data setting. We pool together

γ

j,t

for all

t ≥

3; our results are

similar if we analyze

γ

j,t

from each round

t

separately.

13

An interesting pattern stands out

in all datasets: there is a mass point at 0.5—counteroffers that are halfway between the

12

Some settings have bargaining threads exceeding ten rounds, and we truncate them to the first ten

rounds in Table 1.

13

For the eBay setting, Figure 1.G is not new to the literature, capturing a result that is illustrated in

several panels in Figure 8 of Backus et al. (2020), but here the result is pooled across rounds. Similarly, our

Figure A4.D and column 6 of Table 2 capture the same information as Figure 9 and Table 8 of Backus et al.

(2020). All other results in this study are new.

14

previous two offers, or split-the-difference offers.

14

There are a number of differences across our data settings. The trade tariff setting, for

example, likely involves agents bargaining over multiple issues simultaneously, unlike, say,

the rides setting. In practice, agents in a multi-issue setting might be expected to fully

concede on one issue in return for the other party’s concession on a separate issue. These

possibility makes it all the more striking that split-the-difference offers within a given thread

appear even in the trade setting.

The various settings certainly differ in the relative prevalence of split-the-difference

behavior. Figure 1 shows that housing and settlement appear to have lower frequencies of

split offers relative to non-split offers.

15

We note that both settings often involve principals

and agents on each side, with the agent formally bargaining with the counterparty’s agent

while the principals, in theory, make decisions about what to offer and when to accept on the

basis of communications from their agents. This insulated arrangement may dampen some

effects of principals’ preferences, such as a preference for fairness. Also, parties bargaining

over the resolution of an insurance claim may anticipate bargaining over more rounds on

average. Early offers and counter-offers may serve some other purpose, whereas split-the-

difference offers may represent a genuine attempt to resolve the dispute without (or with

very few) further rounds. There are other candidate explanations for this variation as well.

In the housing setting, for instance, the split-the-difference bargaining may be less likely

when sellers have a particularly strong position in the market (with few sellers and many

buyers), such that a split-the-difference offer corresponds to too much concession from the

seller’s standpoint.

Despite the drastic differences in the environments, products, outcomes, or agents, the

presence of a split-the-difference pattern is clear in all seven settings. To our knowledge,

the widespread nature of this split-the-difference pattern in negotiations in the field has not

previously been documented. Unlike laboratory experiments, where prior research shows

that players split a commonly known pie, in our settings, no player knows the true valuation

of her opponent. A challenge is then to explain why, in real-world negotiations with private

information, players propose offers that split the difference between endogenous offers.

14

Another common mass point in these histograms is at zero, representing cases where a player does not

budge at all. In the housing dataset, a mass point at 1 is also common, representing that an agent fully

concedes to the seller’s list price.

15

This can also be seen in the “split rate” row in Table 2, discussed in the following section.

15

Figure 1: Distribution of Concession Weights γ

j,t

Panel A: Used Car Bargaining Panel B: Pre-trial Settlement Bargaining

0

.1

.2

.3

0 .25 .5 .75 1

γ

j,t

33,356 observations

0

.02

.04

.06

.08

0 .25 .5 .75 1

γ

j,t

208,463 observations

Panel C: Street Bargaining in a TV Show Panel D: Auto Rickshaw Rides Bargaining

0

.1

.2

.3

0 .25 .5 .75 1

γ

j,t

714 observations

0

.05

.1

.15

.2

.25

0 .25 .5 .75 1

γ

j,t

2,986 observations

Panel E: Bargaining Over Housing Panel F: Trade Tariff Bargaining

0

.1

.2

.3

.4

0 .25 .5 .75 1

γ

j,t

176 observations

0

.05

.1

.15

.2

0 .25 .5 .75 1

γ

j,t

46,985 observations

Panel G: eBay Best Offer Bargaining

0

.05

.1

.15

0 .25 .5 .75 1

γ

j,t

9,789,903 observations

Notes: Each panel shows a histogram of γ

j,t

in a given data setting, as defined in Section 3.

16

4 Split-the-Difference Offers as a Norm

We now present evidence that the split-the-difference pattern that we document in our

empirical settings constitutes a social norm. Following Fehr and Gächter (2000), we define

a social norm as a behavioral pattern that (i) relies on a socially shared belief about

what constitutes appropriate behavior; and (ii) triggers the enforcement of the prescribed

behavior by informal social sanctions. This characterization of split-the-difference as a social

norm is echoed by veteran business and hostage negotiator Chris Voss, who writes, “The

traditional negotiating logic that’s drilled into us from an early age, the kind that exalts

compromise, says ‘Let’s just split the difference...Then everybody’s happy”’ (Voss and Tahl,

2016, p.115). Below we show results suggesting that agents that make split-the-difference

offers are systematically rewarded by the opposing party (or, conversely, that the failure

to make a split-the-difference offer does not yield this reward), confirming the view that

these offers, as part of a social norm, are enforced by informal rewards. These rewards

come in the form of higher probabilities of acceptance and higher probability of subsequent

split-the-difference offers within the same bargaining sequence. Buyers who do not comply

with the norm experience a higher probability of their opponent exiting the negotiations,

which could impose financial or time costs, depending on the setting.

We also show that the two most recent offers are special: offers that split the difference

between other anchor points as less prevalent. These other anchor points include earlier

offers in the game other than the two most recent offers or privately known reference points

(observable only to one bargaining party and not the other), which we observe in some of

our settings. This latter results suggests that agents gravitate to a behavior that is easily

verifiable by all parties, consistent with the idea that split-the-difference offers are subject

to social enforcement. Additionally, we show that an agent’s offer is more likely to split the

difference if either the previous offer by the opponent or that agent’s own previous offer

was a split offer. Split-the-difference offers are also more likely to occur if the opponent’s

previous offer was arguably reasonable. For example, a seller is more likely to propose a

split-the-difference offer at the third round of the game if the buyer’s offer at round 2 was

not well below the seller’s initial offer (i.e., the buyer was not low-balling the seller).

17

4.1

Split-the-Difference Offers Are More Likely to be Accepted, Less

Likely to Cause Exit

In this section, we explore how agents respond when they receive split-the-difference offers

compared to when they do not. We show that split offers are discontinuously more likely

to be accepted than non-split offers, suggesting that splitting the difference is not merely

a heuristic used by the offering party, but rather that it is viewed as preferable (arguably

fair) behavior by both the offerer and the receiver. Consistent with this interpretation,

after agents make split offers, their opponents are less likely to abandon negotiations. This

suggests that the choice to exit a bargaining interaction may be motivated not just by the

lack of expected surplus, but also by the perception that the opponent is not being “fair.”

Specifically, we examine how a player’s choice of offer, as measured by the concession

weight,

γ

j,t

, relates to the probability that the offer is accepted or leads to a breakdown

of negotiations. We create a measure for whether the offer is a “split” offer by creating

an indicator

Split

j,t

that is equal to one if

γ

j,t

is equal to 0.5 (after being rounded to the

nearest hundredth, or

γ

j,t

∈

[0

.

495

,

0

.

505]) for each

t ≥

3. We then estimate the following

linear probability regressions:

Accept

j,t

= βSplit

j,t

+ f (γ

j,t

) + τ

t

+ ϵ

j,t

(3)

Exit

j,t

= βSplit

j,t

+ f (γ

j,t

) + τ

t

+ ϵ

j,t

, (4)

where

Accept

j,t

is an indicator for whether the offer is accepted,

Exit

j,t

is an indicator that

the opponent exits before period

t

+ 1,

τ

t

is a round fixed effect, and

f

(

γ

j,t

) is a flexible

function of

γ

j,t

. We specify

f

(

γ

j,t

) as a third-order polynomial of

γ

j,t

.

16

The results are

reported in Table 2, where each column corresponds to one dataset. We also report the

frequency of acceptance, exit, and split offers. The acceptance rate varies across settings

from 7% to 73%, the exit rates are between 3% and 86%, and the fraction of split offers

ranges from 4% to 19%.

In Panel A, we see a positive coefficient before the “split” offer indicator in all of our

datasets, and this is statistically significant in all columns except the cases of auto rickshaw

rides and housing (columns 4 and 5). This means that an offer in bargaining is more likely to

16

The results are not sensitive to this choice; we find similar results with second-, fourth-, or fifth-order

polynomial approximations. We also find similar results defining “split” offers using other bandwidths,

including 0.01 (i.e., γ

j,t

∈ [0.49, 0.51]) and 0.05 (i.e., γ

j,t

∈ [0.45, 0.55]).

18

Table 2: Acceptance and Exit Following Split Offers

(1) (2) (3) (4) (5) (6) (7)

Cars Settlement TV Show Rides Housing Trade eBay

Panel A: Acceptance

Split 0.120

∗∗∗

0.219

∗∗∗

0.151

∗∗

0.0569 0.158 0.0676

∗∗∗

0.0849

∗∗∗

(0.00830) (0.00555) (0.0615) (0.0354) (0.119) (0.00341) (0.000484)

Panel B: Opponent Exit

Split -0.0402

∗∗∗

-0.00977 -0.103

∗∗∗

-0.0511

∗∗∗

-0.0198

∗∗∗

(0.00577) (0.0122) (0.0392) (0.00453) (0.000504)

N 33356 208463 714 3010 176 46985 9789903

Order of γ

j,t

3 3 3 3 3 3 3

Round FE Yes Yes Yes Yes Yes Yes Yes

Accept rate 0.38 0.34 0.26 0.20 0.73 0.07 0.20

Exit rate 0.27 0.03 0.41 0.86 0.51

Split rate 0.18 0.04 0.14 0.19 0.08 0.17 0.12

R

2

0.146 0.462 0.0295 0.160 0.0336 0.110 0.113

Notes: Table shows the estimated coefficient on the split indicator from the regressions described by equations (3) and

(4). Each column corresponds to a separate data setting. The accept and exit rates are the means of the dependent

variables, and the split rate is the mean of the split indicator. Standard errors are shown in parentheses. The number

of observations for the rides setting differs from that in Table 1 because some scripted bargaining acceptance must be

dropped and some scripted bargaining offers can be included here. The number of observations for the settlement

setting differs from that in Table 1 because some sequences end at round 10, and we have no data on whether round

10 offers were accepted. See Appendix B for details. ∗ : p < 0.10, **: p < 0.05, and ***: p < 0.01

be accepted if it is a split offer than if it is not. This effect is surprisingly large in magnitude,

varying from 5.7% to 21.9%. Conversely, in Panel B, “split” offers are negatively associated

with the opponent exiting the bargaining interaction. While sizes of the effect on exit are

usually smaller than those on acceptance, they are significant in all cases except for the

TV show, where exit is rare. The structure of the data on legal settlements and housing

(columns 2 and 5) do not allow us to examine exit as an outcome in these contexts.

Our result in the housing setting is likely insignificant due to the small sample size (176

offer triples). One possible explanation for the lack of a significant effect on acceptance in

the setting of auto rickshaw rides is, this specification compares the acceptance rate of a

split offer with nearby offers and, as shown Figure 1, the nearby offers in this dataset are

quite sparse. This is also reflected in the high rate of split offers in the fourth column (19%).

Therefore, we likely lack the power to detect a significant effect in this dataset. This dataset,

however, has a unique subset—the scripted bargaining offers that Keniston (2011) randomly

assigned—in which we can obtain estimates that are closer to a causal effect of split offers

on acceptance rates. As highlighted in Section 2.4, buyers in these scripted sequences make

offers that are assigned by the experiment designer rather than arising endogenously. When

19

we estimate equation (3) in this subset of the data, shown in columns 4–5 of Appendix

Table A2, we find positive point estimates, and a particularly large, positive effect in those

sequences that begin with a buyer offer. Appendix Table A3 presents the results of a similar

subsample analysis for equation (4).

In Figure 2, we offer an even more flexible approach to this question, plotting a weighted

local linear fit of acceptance and

γ

j,t

, using observations where

γ

j,t

is not a split offer. We

also plot in Figure 2 the average acceptance probability for observations that are split

offers, along with the 95% confidence bound around this mean. We find that the underlying

relationship between the acceptance and

γ

j,t

is monotonic in most regions, and split offers

are substantially more likely to be accepted than nearby offers with similar

γ

j,t

in all datasets

except the settings of auto rickshaw rides (where we again lack power locally around 0.5)

and housing (where the number of observations is small). In the latter two datasets, the

point estimates are still higher at split offers.

The striking implication overall is that, even across these widely varying field settings,

split-the-difference offers are more likely to be accepted than even a slightly more favorable

offer. This suggests that a preference toward splitting the difference between the two most

recent offers is a norm followed not only by the proposer of these offers but also by the

receiver. These results are reminiscent of findings in a wide range of laboratory ultimatum

games (e.g., Roth et al. 1991), which show receivers frequently rejecting offers of less than

half of the surplus, but accepting “fair” offers of a 50-50 split of the surplus nearly 100% of

the time.

4.2 Split Offers Are Frequently Followed by Split Offers

In this section, we address two empirical questions. First, do split offers in period

t

by one

party tend to be followed by the opponent proposing a split offer in period

t

+ 1? Second, do

split offers in period

t

tend to be followed by split offers by the same party in period

t

+ 2?

Both of these points speak to the question of whether splitting the difference between the

two most recent offers is a norm that is perhaps followed more consistently by some agents

than others and that, when invoked by one agent, tends to be adopted by the opponent.

To examine this question, we analyze the following linear probability model:

Split

j,t

= βSplit

j,t−1

+ ϵ

j,t

, (5)

20

Figure 2: Probability of an Offer Being Accepted

Panel A: Used Car Bargaining Panel B: Pre-trial Settlement Bargaining

0

.2

.4

.6

.8

1

Acceptance Probability

0 .25 .5 .75 1

γ

j,t

0

.2

.4

.6

.8

1

Acceptance Probability

0 .25 .5 .75 1

γ

j,t

Panel C: Street Bargaining in a TV Show Panel D: Auto Rickshaw Rides Bargaining

0

.2

.4

.6

.8

1

Acceptance Probability

0 .25 .5 .75 1

γ

j,t

0

.2

.4

.6

.8

1

Acceptance Probability

0 .25 .5 .75 1

γ

j,t

Panel E: Bargaining Over Housing Panel F: Trade Tariff Bargaining

0

.2

.4

.6

.8

1

Acceptance Probability

0 .25 .5 .75 1

γ

j,t

0

.2

.4

.6

.8

1

Acceptance Probability

0 .25 .5 .75 1

γ

j,t

Panel G: eBay Best Offer Bargaining

0

.2

.4

.6

.8

1

Acceptance Probability

0 .25 .5 .75 1

γ

j,t

Notes: Each panel shows a local linear fit of the acceptance probability as a function of

γ

j,t

along with the acceptance

probability of split offers (plus the 95% confidence interval around this point). The fitted values are estimated using

locally weighted least squares with a tricube weighting function. To facilitate computation of the local linear estimator

in the eBay setting, we use a random sample of 100,000 threads.

21

where we regress the indicator of whether, in period

t

, an agent proposes a split offer,

Split

j,t

,

on the indicator of whether the most recent offer,

Split

j,t−1

(which naturally comes from

the opponent), also corresponds to a split offer. Panel A in Table 3 shows the results.

17

We

observe positive point estimates in each setting, and these estimates are significant in most

columns, suggesting that agents are more likely to propose a split offer when the opponent

has just done the same.

In panel B, we consider a version of equation (5) in which we use

t −

2 actions on

the right-hand side rather than

t −

1, allowing us to examine whether agents who make

split-the-difference offers earlier in the game are more likely to do so again. We find evidence

of this effect for the case of settlement and eBay negotiations and a marginally significant

effect in the case of auto rickshaw rides.

Table 3: Repeat Split-the-Difference Behavior

(1) (2) (3) (4) (5) (6)

Cars Settlement TV Show Rides Trade eBay

A: Effect of Opponent’s Split Offer

Split

j,t−1

0.00304 0.144

∗∗∗

0.117

∗∗

0.00358 0.0928

∗∗∗

0.125

∗∗∗

(0.00763) (0.00672) (0.0591) (0.0193) (0.0188) (0.000840)

N 11622 134107 510 2714 2937 2813127

B: Effect of Agent’s Own Split Offer

Split

j,t−2

0.0440 0.0807

∗∗∗

0.0203 0.0708

∗

-0.000644 0.0699

∗∗∗

(0.0276) (0.00991) (0.0724) (0.0382) (0.0519) (0.00137)

N 2155 83296 343 1121 250 1100490

Notes: Panel A shows the estimated coefficient on the one-period-lagged split indicator from the regression described

by equation (5). Panel B shows results instead using the two-period-lagged split indicator. Each column corresponds

to a separate data setting. The housing data setting is omitted because no sequence contains more than three offers.

∗ : p < 0.10, **: p < 0.05, and ***: p < 0.01

We examine this latter effect further by exploring whether splitting the difference is a

norm followed by certain agents more than by others. To do so, we take advantage of agent

identifiers, which we observe in the used car, trade, and eBay bargaining settings.

18

In a

given dataset, we sort agents by the fraction of split offers among all offers they make. We

then plot, on the horizontal axis in each panel of Figure 3, the cumulative share of offers

made by agents. The solid line corresponds to the cumulative share of offers by these agents

17

We cannot examine this question in the housing dataset as we only observe a single offer triple in each

sequence in that setting.

18

In our other data settings, we have no consistent means of tracking an agent across different bargaining

sequences.

22

that are split offers. If the propensity to propose split offers is roughly equal across all

agents, and if each agent makes a large number of offers, the solid line should be close to the

45-degree line (the dotted one). This comparison can thus be considered a modified Lorenz

curve that measures the “inequality” of split offers among agents.

Figure 3: Some Agents More Likely to Make Split Offers

Panel A: Used Car Bargaining Panel B: Trade Tariff Bargaining

0 .2 .4 .6 .8 1

Cumulative Share of Split Offers

0 .2 .4 .6 .8 1

Cumulative Share of Offers

0 .2 .4 .6 .8 1

Cumulative Share of Split Offers

0 .2 .4 .6 .8 1

Cumulative Share of Offers

Panel C: eBay Best Offer Bargaining

0 .2 .4 .6 .8 1

Cumulative Share of Split Offers

0 .2 .4 .6 .8 1

Cumulative Share of Offers

Notes: Each panel ranks agents by the fraction of split offers among all offers they make and plots their cumulative

share of total offers on the

x

-axis and the cumulative share split offers on the

y

-axis. The solid lines use the real data.

The dashed lines use simulated split indicators assuming every agent has the same propensity to propose split offers.

The dotted line indicates the 45-degree line.

Figure 3 indeed shows a gap between the solid and dotted lines in each panel. In reality,

however, we only observe a few offers made by a given agent, and hence a large part of the

area between the solid line and the 45-degree line is due to sampling noise.

19

To construct a

more meaningful benchmark, we consider a case where each agent has the same probability

to propose a split offer, with this probability given by the split rate reported in Table 2.

19

For example, suppose every agent has the same propensity

q

to propose a split offer, but each agent only

ever proposes one offer in the data. We would observe roughly a fraction of

q

players proposing one split

offer and a fraction of 1

− q

players proposing no split offers, and the curve will be far off the 45-degree line.

23

Using this split rate, we simulate a fake split indicator for each observation following a

Bernoulli distribution. We plot our cumulative share of split offers based on these fake

indicators using the dashed line in Figure 3, which should lie between the 45-degree line and

the curve plotted using the real data.

Comparing the dashed and solid lines in Figure 3, we find evidence that some agents

have a stronger proclivity toward split-the-difference than others. This is particularly the

case in the eBay and trade settings, where the dashed line is farther from the solid line. In

the used-car setting, the solid and dashed lines are close, indicating that the propensity to

make split-the-difference offers is roughly uniform across agents.

4.3 The Two Most Recent Offers Are Special

Our analysis in Section 3 demonstrates robust evidence across a wide spectrum of settings

that a modal strategy in real-world bargaining is to make offers that split the difference

between the two most recent offers. Here, we explore whether it is indeed the two most

recent offers that serve as the most prominent anchor points that players tend to split in

half, or whether other anchor points are equally common. For example, it is possible that

offers splitting the difference between earlier offers in the game (prior to the two most recent

offers) are also common. For example, in a sequence

{

100

,

50

,

90

,

70

}

, a subsequent offer

splitting the difference between the two most recent offers would be 80, but it may be that

75 (which splits the difference between the first two offers) is also a focal point for players in

this game.

To examine this possibility, we define placebo concession by treating the proposed amount

in round

t

as a convex combination of offers from earlier rounds of the game. For example,

for

t

= 4, we can treat the proposed amount as a convex combination of offers from the first

and second rounds, which we define as

γ

3

j,4

=

p

j,4

− p

j,1

p

j,2

− p

j,1

. In general, for

t ≥

4 and

s < t

, the

placebo concession is defined as follows:

γ

s

j,t

=

p

j,t

− p

j,s−2

p

j,s−1

− p

j,s−2

, t ≥ 4, 3 ≤ s < t, (6)

where

t

is the round in which the current offer is evaluated, and

s < t

is the round in which

offers from rounds

s −

1 and

s −

2 actually were the two most recent offers. If negotiating

agents care most about fairness as defined by an equal split of the two most recent offers, we

24

expect less mass at 0.5 for the placebo concession than in our main results from Section 3.

For this analysis, we focus on the three datasets for which we have the longest sequences,

as they allow us to construct the placebo concession metric: used car bargaining, pre-

trial settlement bargaining, and eBay bargaining. Figure 4 plots the distribution of true

concession and placebo concession in these three datasets. In the left column, we replicate

the histograms of true concession weights from Figure 1. In the middle column, we plot

histograms of the placebo concession weights based on bargaining offers in earlier rounds,

γ

s

j,t

, t ≥ 4, 3 ≤ s < t, as defined in equation (6).

Figure 4: Distribution of True Concession and Placebo Concession

True Placebo Placebo, Restricted

Panel A: Used Car Bargaining

0

.1

.2

.3

.4

.5

0 .25 .5 .75 1

γ

j,t

0

.1

.2

.3

.4

.5

0 .25 .5 .75 1

γ

j,t

s

0

.1

.2

.3

.4

.5

0 .25 .5 .75 1

γ

j,t

s

Panel B: Pre-trial Settlement Bargaining

0

.03

.06

.09

0 .25 .5 .75 1

γ

j,t

0

.03

.06

.09

0 .25 .5 .75 1

γ

j,t

s

0

.03

.06

.09

0 .25 .5 .75 1

γ

j,t

s

Panel C: eBay Best Offer Bargaining

0

.05

.1

.15

0 .25 .5 .75 1

γ

j,t

0

.05

.1

.15

0 .25 .5 .75 1

γ

j,t

s

0

.05

.1

.15

0 .25 .5 .75 1

γ

j,t

s

Notes: Figure shows, in left plots, histograms of true concession weights (γ

j,t

) as in Figure 1 for the cars (panel A),

settlement (panel B), and eBay (panel C) settings. In the middle plots, we show histograms of the placebo concession

weights. In the right plots, we show histograms of the placebo concession weights restricting the sample to exclude

observations that are mechanically equal to 0.5.

In the third column of Figure 4, we focus on a restricted sample in which we drop cases

25

that can mechanically lead to mass points at 0.5 even in the placebo concession weights. As

an example, consider an offer sequence with the first four offers being

{

100

,

60

,

90

,

70

}

. A

split-the-difference offer at the fifth round would be 80, but this offer would also represent

splitting the difference between the earlier offers of 100 and 60. Our restricted sample

excludes placebo concession weights that are exactly equal to the true concession weights

for a given round.

Panels A and C of Figure 4 demonstrate that counteroffers occur halfway between earlier

offers of the game (the middle and right columns) less frequently than between the two

most recent offers (the left column). In panel B, the pre-trial settlement bargaining, placebo

split-the-difference offers are also frequent. However, in both the middle and right figures in

panel B, the mass is more uniformly distributed across concession weights in the placebo

cases than in the left column, suggesting that the relative likelihood of split-the-difference

offers is the highest when considering the two most recent offers.

To formally test whether the masses at 0.5 are different in the true vs. placebo concession

weights, we calculate the fraction of split-the-difference offers (as in Section 4.1) for the true

concession weights, placebo concession weights, and their differences, as well as standard

errors on each of these.

20

We also compute the fraction of split offers among placebo

concession weights in the restricted sample. Table 4 presents the results. In each dataset,

we detect a (statistically significantly) larger fraction of split offers using the true concession

weights than the placebo concession weights, suggesting that players indeed rely more

strongly on the two most recent offers than on earlier offers in determining a 50-50 split.

4.4 Splitting Based on Private Information

We also analyze whether agents tend to propose offers that split the difference between a

publicly known threshold (a previous offer) and a privately known quantity that relates to

agents’ values. For this analysis, we exploit a number of privately known variables specific

to several of our settings, including the secret reserve price known only to the seller in the

used-car setting; the reserve/loss estimate known only to the “buyer” (the insurer) in the

settlement negotiation setting; and the auto-accept or auto-decline prices that are known

only to the seller in the eBay setting. The importance of these variables is that they are

20

Standard errors on the difference are constructed from 100 nonparametric bootstrap-sample estimates of

the true and placebo rates, sampling at the thread level.

26

Table 4: Fraction of Split Offers in True vs. Placebo Concession Weights

True Placebo Difference Placebo Difference

Restricted

Panel A: Used Car Bargaining

Split 0.1823 0.0503 0.1319 0.0614 0.1208

(0.0019) (0.0020) (0.0023) (0.0033) (0.0034)

N 33,356 14,721 6,674

Panel B: Pre-trial Settlement Bargaining

Split 0.0435 0.0218 0.0217 0.0190 0.0245

(0.0004) (0.0003) (0.0005) (0.0003) (0.0005)

N 208,463 313,216 292,470

Panel C: eBay Best Offer Bargaining

Split 0.1176 0.0437 0.0739 0.0424 0.0753

(0.0001) (0.0001) (0.0001) (0.0001) (0.0001)

N 9,789,903 4,353,489 3,880,706

Notes: Table shows the fraction of split offers among the true concession weights (first column) vs. the placebo

concession weights (second column), as well as the difference of these means (third column). The fourth column shows

the fraction of split offers among the placebo concession weights in the restricted sample, and the fifth column shows

the difference between this mean and the true concession weight fraction. Standard errors are shown in parentheses.

Panel A shows this analysis for the cars sample, panel B for the pre-trial settlement sample, and panel C for the eBay

sample.

each privately known to only one side; thus, these variables allow us to examine whether

agents’ behavior is more consistent with equally splitting some quantity that is based on the

public information contained in agents’ previous offers or whether instead agents appear to

offer prices that constitute an equal split relative to their own private information.

For this analysis, we follow our construction of placebo concession weights from Section

4.3, replacing some offer information with these privately known quantities. We describe

this analysis and results in detail in Appendix C. The bulk of the evidence from this exercise

suggests that split-the-difference behavior is less related to such privately known values and

more related to the two most recent offers.

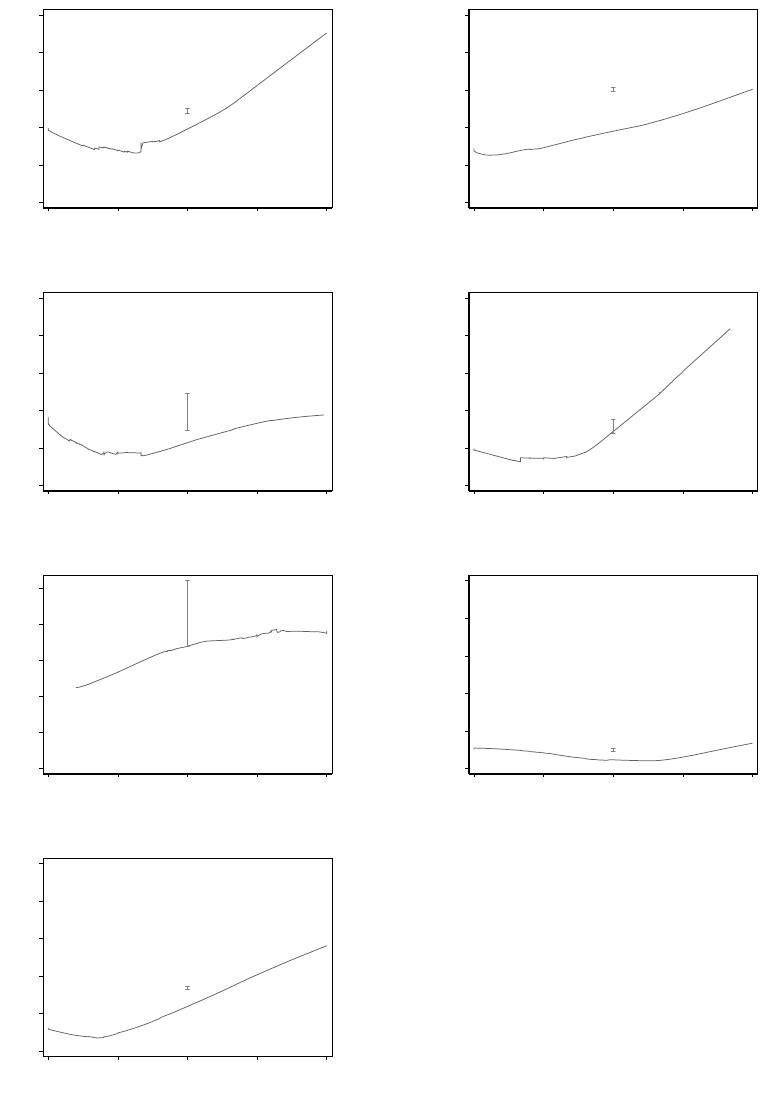

4.5 When are Split-the-Difference Offers Made?

It is possible that the set of cases in which split-the-difference offers might occur is constrained,

either because the mid-point between the two previous offers might be lower than the seller’s

true willingness to sell or higher than the buyer’s willingness to pay, or because a very

27

demanding offer from the opponent might be seen as “unfair” (a buyer low-balling the seller,

for example) and thus not deserving of a “good faith” split-the-difference counteroffer. Both

of these arguments suggest that when a buyer’s offer is only a small fraction of the seller’s

initial offer, we are unlikely to observe a subsequent split-the-difference offer, with the same

being true for relatively high seller offers. Conversely, when the difference between previous

offers is very small—for instance, within a few percentage points—the size of potential

surplus may be small, and fairness concerns might be less relevant.

Figure 5 examines these patterns, showing the probability that an agent makes a split

offer in round

t

= 3 as a function of the ratio of the first two offers. Regardless of the order

of the moves (that is, whether the seller or the buyer make the first offer in the thread), this

is the ratio of the buyer’s first offer to the seller’s first offer; thus, the ratio is always between