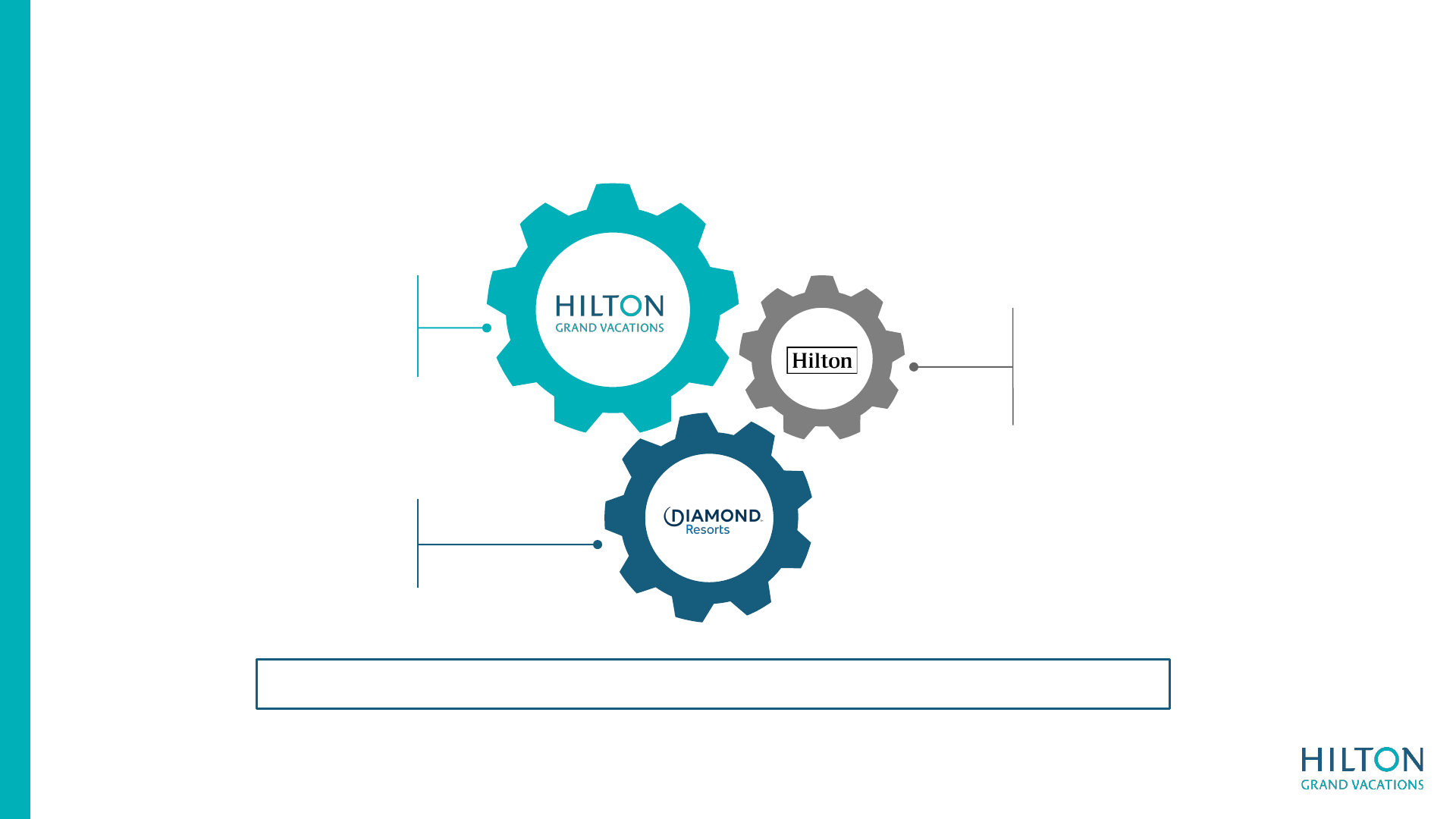

Hilton Grand

Vacations to Acquire

Diamond Resorts

March 10, 2021

Forward-Looking Statements

This communication contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended and Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements convey management’s

expectations as to our future, and are based on management’s beliefs, expectations, assumptions and such plans, estimates, projections and other information available to management at the time we make such statements. Forward-looking statements include all

statements that are not historical facts, including those related to our revenues, earnings, cash flow and operations, and may be identified by terminology such as the words “outlook,” “believe,” “expect,” “potential,” “goal,” “continues,” “may,” “will,” “should,” “could,”

“seeks,” “approximately,” “projects,” predicts,” “intends,” “plans,” “estimates,” “anticipates” “future,” “guidance,” “target,” or the negative version of these words or other comparable words.

We caution you that our forward-looking statements involve known and unknown risks, uncertainties and other factors, including those that are beyond our control, that may cause our actual results, performance or achievements to be materially different from the

future results. Factors that could cause our actual results to differ materially from those contemplated by our forward-looking statements include: the occurrence of any event, change or other circumstances that could give rise to the termination of the merger

agreement; the inability to complete the proposed merger due to the failure to obtain stockholder approval for the proposed merger or the failure to satisfy other conditions to completion of the proposed merger, including that a governmental entity may prohibit, delay

or refuse to grant approval for the consummation of the transaction; risks related to disruption of management’s attention from HGV’s ongoing business operations due to the transaction; the effect of the announcement of the proposed merger on HGV’s

relationships, operating results and business generally; the risk that the proposed merger will not be consummated in a timely manner; exceeding the expected costs of the merger; the material impact of the COVID-19 pandemic on our business, operating results,

and financial condition; the extent and duration of the impact of the COVID-19 pandemic on global economic conditions; our ability to meet our liquidity needs; risks related to our indebtedness; inherent business risks, market trends and competition within the

timeshare and hospitality industries; our ability to successfully source inventory and market, sell and finance VOIs; default rates on our financing receivables; the reputation of and our ability to access Hilton brands and programs, including the risk of a breach or

termination of our license agreement with Hilton; compliance with and changes to United States and global laws and regulations, including those related to anti-corruption and privacy; risks related to our acquisitions, joint ventures, and other partnerships; our

dependence on third-party development activities to secure just-in-time inventory; the performance of our information technology systems and our ability to maintain data security; regulatory proceedings or litigation; adequacy of our workforce to meet our business

and operation needs; our ability to attract and retain key executives and employees with skills and capacity to meet our needs; and natural disasters or adverse geo-political conditions. Any one or more of the foregoing factors could adversely impact our operations,

revenue, operating margins, financial condition and/or credit rating.

For a more detailed discussion of these factors, see the information under the captions “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in HGV’s most recent Annual Report on Form 10-K filed with the

Securities and Exchange Commission on March 1, 2021, as such information may be updated from time to time in our annual reports, quarterly reports, current reports and other filings we make with the Securities and Exchange Commission.

HGV’s forward-looking statements speak only as of the date of this communication or as of the date they are made. HGV disclaims any intent or obligation to update any “forward looking statement” made in this communication to reflect changed assumptions, the

occurrence of unanticipated events or changes to future operating results over time.

Additional Information and Where to Find It

This filing may be deemed solicitation material in respect of the proposed acquisition of Diamond Resorts by HGV. In connection with the proposed merger transaction, HGV will file with the SEC and furnish to HGV’s stockholders a proxy statement and other

relevant documents. This filing does not constitute a solicitation of any vote or approval. Stockholders are urged to read the proxy statement when it becomes available and any other documents to be filed with the SEC in connection with the proposed merger or

incorporated by reference in the proxy statement because they will contain important information about the proposed merger.

Investors will be able to obtain free of charge the proxy statement and other documents filed with the SEC at the SEC’s website at https://www.sec.gov. In addition, the proxy statement and HGV’s annual reports on Form 10-K, quarterly reports on Form 10-Q,

current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 are available free of charge through HGV’s website at https://investors.hgv.com. as soon as reasonably

practicable after they are electronically filed with, or furnished to, the SEC.

The directors, executive officers and certain other members of management and employees of HGV may be deemed “participants” in the solicitation of proxies from stockholders of HGV in favor of the proposed merger. Information regarding the persons who may,

under the rules of the SEC, be considered participants in the solicitation of the stockholders of HGV in connection with the proposed merger will be set forth in the proxy statement and the other relevant documents to be filed with the SEC. You can find information

about the Company’s executive officers and directors in its Annual Report on Form 10-K for the fiscal year ended December 31, 2020 and in its definitive proxy statement filed with the SEC on Schedule 14A on March 26, 2020.

Non-GAAP Financial Measures

This presentation includes discussions of terms that are not recognized terms under U.S Generally Accepted Accounting Principles (“GAAP”), and financial measures that are not calculated in accordance with GAAP, such as Adjusted EBITDA. We derived any non-

GAAP financial measures from our audited consolidated financial statements, and Dakota Holdings, Inc.’s financial statements. We believe such non-GAAP measures provide useful information to our investors about us and our financial condition and results of

operations since these measures are used by our management to evaluate our operating performance and by securities analysts and investors as common financial measures for comparison purposes in our industry. See our most recent Annual Report on Form

10-K for a more detailed discussion of the meanings of these terms and our reasonings for providing non-GAAP financial measures and the Appendix to this presentation for full reconciliations of these measures to the most directly comparable GAAP financial

measure.

2

The acquisition of Diamond Resorts presents a transformational

opportunity

1

Significant value creation from scale

benefits of combining the largest independent

timeshare company with the strength of Hilton Grand

Vacations’ brand and culture

4

Diversifies HGV portfolio, adding additional

drive-to destinations and allowing HGV to leverage

the Hilton network to penetrate a broader customer

segment

3 6

2

Accelerates launch of HGV-branded trust

product offering by rebranding Diamond’s

properties over time to drive revenue growth in a new

customer segment

5

Increases recurring EBITDA streams and

drives overall cash flow, with adjusted free cash flow per

share accretion in year one

1

Ideal timing to capitalize on anticipated leisure travel recovery

Generates $125M+ in run-rate cost

synergies expected to be achieved in the first 24

months following close

Compelling valuation and deal structure

facilitates financial flexibility and deleveraging

1) Excluding one-time transaction related expenses

3

Transaction overview

• Total deal value of $3.0 billion with consideration paid by HGV at closing expected to be $1.4 billion

1

• Funded through the issuance of approximately 34.5 million shares of HGV common stock

• Purchase price is 7.0x Diamond Resorts International (“DRI”) Adjusted EBITDA

2

plus synergies

3

• Pro forma equity ownership approximately 72% existing HGV shareholders, 28% funds affiliated with Apollo

Global Management, Inc. (“Apollo”) and co-investors

• $2.8 billion of financing commitments in place from 3 banks

• Over $125 million in run-rate cost synergies achieved within the 24 months following close of the

transaction

• Significant future revenue synergy opportunities

Consideration

and Offer

Structure

Synergy

Potential

Timeline

Management,

Ownership,

Board

Leverage and

Cash Flow

• Mark Wang, Dan Mathewes, and Gordon Gurnik will remain CEO, CFO, and COO, respectively

• Board will be expanded by two seats to nine members, with Apollo having the right to designate two seats as

long as they retain equity ownership of HGV at or above 15%, and one seat while they retain equity ownership

at or above 10%

• FCF/share and EBITDA/share accretive in year one on an adjusted

4

basis

• 50-60% FCF conversion of Adjusted EBITDA

4

in steady state

• Pro forma leverage

4

6.5x, returning to below 3.0x within 24 months

• Target closing summer of 2021, subject to customary closing conditions

3

1) Assumes issuance of 34.5 million shares of HGV stock at $40.32 per share. Excludes one-time transaction adjustments and assumption of $657

million of securitized debt from DRI, which is non-recourse to the combined entity

2) 2019 DRI Adjusted EBITDA; see Reconciliations provided in Appendix

3) Includes identified cost synergies of $125 million

4) 2020; Adjusted to exclude the impact of net deferrals of revenue and direct expenses related to the Sales of VOIs under construction

4

A powerful combination…

• World-class hospitality with the strength of the

trusted Hilton brand

• 62 upper upscale and luxury properties in premier

resort destinations

• Proven track record of positive NOG

• Points-based deeded system enables flexible

inventory sourcing from owned or fee partners

• Best in class lead generation capabilities

and sales systems

• Industry-leading VPG and margins

• Over 325,000 owners

• Largest timeshare operator with no hotel

brand affiliation

• Extensive network of 92 leisure resorts across

the globe, with strong regional drive-to market presence,

and complementary upscale range

• Points-based trust structure enabling incremental

pricing segmentation

• 4 years of excess developed inventory available for sale

• Pioneered the innovative Events of a Lifetime®

experiential sales & marketing platform that drives strong

engagement at a significant VPG premium

• Nearly 400,000 owners

5

…creating the premier vacation ownership company

878K

731K

660K

405K

326K

220K

Wyndham

Destinations

HGV +

Diamond

Marriott

Vacations

Diamond HGV Bluegreen

Owners

230

150

110

91

59

45

Wyndham

Destinations

HGV +

Diamond

Marriott

Vacations

Diamond HGV Bluegreen

Resorts

945K

663K

448K

383K

280K

236K

Wyndham

Destinations

HGV +

Diamond

Marriott

Vacations

HGV Diamond Bluegreen

Tours

$2,355

$2,342

$1,524

$1,410

$932

$619

Wyndham

Destinations

HGV +

Diamond

Marriott

Vacations

HGV Diamond Bluegreen

Contract Sales

$3,518

$3,439

$3,403

$3,331

$2,642

$2,381

HGV HGV +

Diamond

Marriott

Vacations

Diamond Bluegreen Wyndham

Destinations

VPG

$991

$883

$758

$453

$305

$122

Wyndham

Destinations

HGV +

Diamond

Marriott

Vacations

HGV Diamond Bluegreen

Adjusted EBITDA

$ in millions

$ in millions

1

2

2

Source: 2019 company filings

1) Estimated

2) Adjusted for net deferrals of revenue and direct expenses related to the Sales of VOIs under construction; combined includes total identified run-rate cost synergies of $125 million; see

Reconciliations in Appendix

2

2019 operating metrics

6

Synergies are a significant EBITDA opportunity

More products

1

More places

2

More owners

3

Cost synergiesRevenue levers

• Branded trust product

• Expanded chain scale

• Broader price coverage

• Experiential offerings

• Expanded regional network

• Higher NOG

• Additional HGV owner sales

• Diamond owner base activated

by Hilton Grand Vacations brand

Diamond rental performance

HGV new buyer lift

Diamond new buyer lift

HGV owner lift

Diamond owner lift

Revenue synergies

General & administrative

efficiencies

Operational efficiencies

Financial efficiencies

Cost synergy run-rate achieved in the first 24 months following close

$125M+ identified

7

HGV will have the broadest chain scale offering in the industry

Midscale

Upper

Midscale

Upscale Upper Upscale Luxury

Hilton Vacation Club

Former Diamond Properties

Competitors

1

Enhances alignment with Hilton system and their 112 million Hilton Honors members

1) Illustrative chain scale positioning

8

Wider range of price points will broaden addressable market

List price per week for HGV vs. Diamond inventory…

…enhances value proposition for more

demographics, expanding our core market

Diamond's 75

th

percentile price point sits just below HGV's

lowest 25

th

percentile

1

# US householders age 25-74

2

+

=

HGV current

core market

Expansion

HGV new

core market

14M

41M

55M

Household income $75-100KHousehold income $100K +

>34%

increase

Combined

75

th

50

th

25

th

75

th

50

th

25

th

~$93K

~$60K

~$39K

~$34K

~$25K

~$18K

75

th

50

th

25

th

~$80K

~$47K

~$28K

1) Figures unweighted by room count

2) Selected Characteristics of Households by Total Money Income in 2019. US Census Bureau, Current Population Survey, 2020 ASEC Supplement

9

More properties in more places

Benefits of expanded

geographic portfolio

34

9

8

17

9

18

DRI

Beach

Desert &

Outdoors

Ski

Urban

18

Attractions

HGV

11

9

27

18

• Higher tour flow, with more locations

to access and offer

• Higher conversion, with broader appeal

to new customers

38

15

9

16

54

9

29

32

24

Drive-to

Destination

92

International

38

US + Canada Only

Global

HGV-only

market

Diamond-only

market

Common

market

HGV resorts Diamond resorts

Sales Centers

EUROPE (5+24)

MEXICO & CARIBBEAN (2+5)

JAPAN (2)

US +

Canada

Capistriano Beach

Virginia Beach

Panorama

South Lake Tahoe

Estes

Park

Santa Fe

Brian Head

San Luis Bay

Carlsbad

Ramona

Sedona

Cave Creek/Payson

Scottsdale

Pinetop

Tucson

Park City

Breckenridge

Las Vegas

Cabo

Chicago

South Bend

New York

Tremblant

Blue Mountain

D.C.

Williamsburg

Kitty Hawk

Sapphire

Myrtle Beach

Charleston

Hilton Head

Daytona/

Ormond Beach

Orlando

Miami

Naples/Marco Island

Captiva/Sanibel

Sandestin

Gatlinburg

Branson

Whistler/Vancouver

Kauai

Honolulu

Maui

Waikoloa

Palm Desert

Palm Springs

Sonora

51

Note: "Outdoors" is composed of Gatlinburg and Pigeon Forge, TN and Ucluelet, Canada. "Regional" is composed of

US excluding Hawaii and NYC. "Destination" is composed of Hawaii, NYC, and Canada. Mexico also includes Diamond

location in Zihuatanejo (not pictured on map)

48

10

New branded trust offers additional benefits

Advantages

for combined

entity

✓ Premium pricing for certainty of availability in high

demand real estate markets

✓ Inventory sourcing flexibility and efficiency allows us to

employ a fee-for-service model with multiple partners

✓ Ability to pre-sell new developments supports strong

project-level cash flow and returns

✓ Smoother sales and upgrades, with less specific

matching of buyer to property

✓ Lowers barrier to ownership and broadens ability

to buy into system with more flexible pricing options

✓ Reduces inventory delivery volatility and reliance

on new builds

✓ Facilitates inventory recycling, reducing new build needs

Deeded points Trust points

Advantages

for buyers

and owners

✓ Guaranteed availability to reserve purchased week

provides peace of mind

✓ Aspirational sense of true ownership

✓ Physical asset that can be passed down to

future generations

✓ Geographic flexibility to access network without

committing to home resort

✓ Timing flexibility, as not tied to a particular time

of year or duration

11

We’ll generate meaningful annuity revenue from recurring, capital-

efficient sources

Club

membership fees

New buyers and owner upgrades further grow

these fee streams and create a multiplier effect

NOG generates several high margin,

recurring fee streams:

Property

management fees

Financing

fees

~50%

of Segment

Adjusted EBITDA

from recurring

sources

1

~40%

of Segment

Adjusted EBITDA

from recurring

sources

1

1) Adjusted for net deferrals of revenue and direct expenses related to the Sales of VOIs under construction

12

Focus on efficiency to drive free cash flow conversion

Tap significant developed inventory

pipeline to reduce near-term spending needs

Reduce long-term inventory spending

with increased rate of inventory recapture

Maintain industry-leading margins

First year Steady state

Double-digit adjusted FCF/share accretive

1

50-60% adjusted FCF conversion

2

Operating efficiency Working capital efficiency

Realize incremental $20-25M of

annualized HGV standalone cost

reductions identified in 2020

Realize $125M+ of run-rate cost synergies

1) Excluding one-time transaction costs

2) Conversion of Adjusted EBITDA excluding the impact of net deferrals of revenue and direct expenses related to the Sales of VOIs under construction

13

We will maintain our financial flexibility

Pro-forma liquidity of $1.0 billion at year-end 2020

Nearly $300 million of receivables eligible for securitization or

warehouse borrowing

Capital market efficiencies from increased scale of combined ABS

platform

Cash flow generation will drive rapid deleverage

Pro forma leverage

1

6.5x, returning to below 3.0x within 24 months

Diamond Ocean Beach Club

Virginia Beach, Virginia

Diamond Embarc Whistler

Whistler, Canada

1) Using 2020 Adjusted EBITDA excluding the impact of net deferrals of revenue and direct expenses related to the Sales of VOIs under

construction

14

We have the unique capabilities and brand to deliver this deal's value

Premier branded

timeshare operator with

29 years of NOG and

industry leading margins

Powerful trust-based

network built by years

of acquisitions

Proven brand integration into our

marketing engine, now applied

across a broader owner,

demographic, and property base

Ideal timing to capitalize on anticipated leisure travel recovery

Appendix

16

Sources

Equity Issued to

DRI

1

$1,392

Cash on Hand

304

New Debt Issued

2,323

Debt

Assumed

2

598

Total Sources

$4,617

Uses

Purchase of

DRI

$1,392

Debt

Assumed

2

598

Debt Repaid

2,503

Transaction Fees & Other

125

Total Uses

$4,617

Transaction sources and uses

Note: Totals may not foot due to rounding

1) 34.5 million HGV common shares issued at $40.32

2) Excludes non-recourse, securitized timeshare debt of $657 million

17

2019 Net income to Adjusted EBITDA reconciliation

1) 2019 results derived from HGV’s 2020 Annual Report on Form 10-K

2) Derived from Dakota Holdings, Inc (“Diamond Resorts”) 2019 financial statements, further adjusted to conform to HGV’s definition of Adjusted EBITDA

3) For Diamond Resorts, other adjustment items includes costs primarily associated with acquisition and integration costs, restructuring, consulting and other one-time charges

4) Represents the deferred revenues and related direct expenses from the sales of VOIs under construction

5) Represents estimated annualized cost synergies

6) Represents Adjusted EBITDA as defined, further adjusted for deferred revenues and related direct expenses from the sales of VOIs under construction

($ in millions) HGV

1

Diamond

Resorts

2

Pro Forma

Combined

Net income (loss) $216 $(43) $173

Interest expense 43 166 209

Income tax expense 57 4 61

Depreciation and amortization 44 118 162

Interest expense, depreciation and amortization included

in equity in earnings from unconsolidated affiliates

3 3

EBITDA 363 245 608

Amortization of portfolio premium 13 13

Other loss (gain), net 3 (1) 2

Share-based compensation expense 22 3 25

Other adjustment items

3

20 45 65

Adjusted EBITDA $408 $305 $713

Adjustments:

Net deferrals (recognitions)

4

45 45

Annualized run-rate cost savings

5

125

Adjusted EBITDA

6

$453 $305 $883