NREL is a national laboratory of the U.S. Department of Energy

Office of Energy Efficiency & Renewable Energy

Operated by the Alliance for Sustainable Energy, LLC

This report is available at no cost from the National Renewable Energy

Laboratory (NREL) at www.nrel.gov/publications.

Contract No. DE-AC36-08GO28308

Technical Report

NREL/TP-6A40-85879

March 2024

Achieving an 80% Renewable Portfolio

in Alaska’s Railbelt: Cost Analysis

Paul Denholm

, Marty Schwarz, and Lauren Streitmatter

National Renewable Energy Laboratory

NREL is a national laboratory of the U.S. Department of Energy

Office of Energy Efficiency & Renewable Energy

Operated by the Alliance for Sustainable Energy, LLC

This report is available at no cost from the National Renewable Energy

Laboratory (NREL) at www.nrel.gov/publications.

Contract No. DE-AC36-08GO28308

National Renewable Energy Laboratory

15013 Denver West Parkway

Golden, CO 80401

303-275-3000 • www.nrel.gov

Technical Report

NREL/TP-6a40-85879

March 2024

Achieving an 80% Renewable Portfolio

in Alaska’s Railbelt: Cost Analysis

Paul Denholm

, Marty Schwarz, and Lauren Streitmatter

National Renewable Energy Laboratory

Suggested Citation

Denholm

, Paul, Marty Schwarz, and Lauren Streitmatter. 2024. Achieving an 80%

Renewable Portfolio in Alaska’s Railbelt: Cost Analysis

. Golden, CO: National Renewable

Energy Laboratory. NREL/

TP-6A40-85879. https://www.nrel.gov/docs/fy24osti/85879.pdf.

NOTICE

This work was authored by the National Renewable Energy Laboratory, operated by Alliance for Sustainable

Energy, LLC, for the U.S. Department of Energy under Contract No. DE-AC36-08GO28308. Funding provided by

the U.S. Department of Energy Office of Energy Efficiency and Renewable Energy’s Strategic Analysis team and

Renewable Energy Grid Integration program. The views expressed in the article do not necessarily represent the

views of the DOE or the U.S. Government. The U.S. Government retains a nonexclusive, paid-up, irrevocable,

worldwide license to publish or reproduce the published form of this work, or allow others to do so, for U.S.

Government purposes.

This report is available at no cost from the National Renewable

Energy Laboratory (NREL) at www.nrel.gov/publications

.

U.S. Department of Energy (DOE) reports produced after 1991

and a growing number of pre-1991 documents are available

free via www.OSTI.gov

.

Cover Photos by Dennis Schroeder: (clockwise, left to right) NREL 51934, NREL 45897, NREL 42160, NREL 45891, NREL 48097,

NREL 46526.

NREL prints on paper that contains recycled content.

iv

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

Acknowledgments

This work would not have been possible without the very helpful collaboration, input, and data

provided by numerous stakeholders across Alaska, including (alphabetized):

• Alaska Center for Energy and Power: Phylicia Cicilio, Jeremy VanderMeer

• Alaska Energy Authority: Bryan Carey, Conner Erikson, Ryan McLaughlin

• Alaska Renewables, LLC: Andrew McDonnell, Matt Perkins

• Analysis North: Alan Mitchell

• Chugach Electric Association: John Bell, Mark Henspeter, Dustin Highers, Arthur Miller,

Allan Rudeck, Sean Skaling, Russell Thornton

• Cyrq Energy: Nick Goodman

• DOE’s Arctic Energy Office: Erin Whitney

• Golden Valley Electric Association: Dan Bishop, John Burns, Naomi Knight, Keith Palchikoff

• Homer Electric Association: Larry Jorgensen, Mike Salzetti, Mike Tracy

• Matanuska Electric Association: Nathan Greene, Edward Jenkin, Jon Sinclair

• Polarconsult Alaska, Inc.: Joel Groves

• Renewable Energy Alaska Project: Chris Rose, Antony Scott

The authors would also like to thank the following individuals from the National Renewable

Energy Laboratory for their contributions. Helpful review and comments were provided by Ian

Baring-Gould, Jaquelin Cochran, Elise DeGeorge, Levi Kilcher, David Palchak, Mark Ruth,

Meyer Seligman, Gian Porro, and Nathan Wiltse. Maps were generated by Billy Roberts. Editing

was provided by Liz Breazeale and Emily Horvath.

This work was authored by the National Renewable Energy Laboratory, operated by Alliance for

Sustainable Energy, LLC, for the U.S. Department of Energy under Contract No. DE-AC36-

08GO28308. Funding provided by the U.S. Department of Energy Office of Energy Efficiency

and Renewable Energy’s Strategic Analysis team and Renewable Energy Grid Integration

program. The views expressed in the article do not necessarily represent the views of the DOE or

the U.S. Government. The U.S. Government retains a nonexclusive, paid-up, irrevocable,

worldwide license to publish or reproduce the published form of this work, or allow others to do

so, for U.S. Government purposes.

v

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

List of Acronyms

AC alternating current

ACEP Alaska Center for Energy and Power

AEA Alaska Energy Authority

AEO Annual Energy Outlook

ATB Annual Technology Baseline

CC combined cycle

CEM capacity expansion model

CHP combined heat and power

CT combustion turbine

DC direct current

DPV distributed PV

EIA U.S. Energy Information Administration

EV electric vehicle

GVEA Golden Valley Electric Association

GWh gigawatt-hours

HEA Homer Electric Association

HVDC high-voltage direct current

IRA Inflation Reduction Act

IBR inverter-based resources

ICE internal combustion engine

ITC investment tax credit

LCOE levelized cost of energy

LNG liquified natural gas

MEA Matanuska Electric Association

MMBtu million British thermal units

MW megawatts

MWh megawatt-hours

NPV net present value

NREL National Renewable Energy Laboratory

O&M operations and maintenance

PCM production cost model

PM particulate matter

PPA power purchase agreement

PV photovoltaics

REC renewable energy certificate

RIRP Regional Integrated Resource Plan

RPS renewable portfolio standard

T&D transmission and distribution

TWh terawatt-hours

vi

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

Executive Summary

The Alaska Railbelt utilities face growing challenges because of the declining supply of natural

gas from the Cook Inlet and substantial projected price increases. Renewable energy in the form

of wind and solar is a potentially cost-competitive option to reduce reliance on natural gas, which

in 2022 provided nearly two-thirds of the Railbelt electricity demand.

This study examines the system-level costs and benefits of increased renewable energy

deployment in the Railbelt grid,

1

in the context of a proposed 80% renewable portfolio standard

(RPS). This work studies the period from 2024 to 2040 and uses a model that simulates the

planning, evolution, and operation of the power system to identify the mix of resources that

maintains system reliability at the lowest electricity system cost over the period of analysis. The

model tracks several reliability metrics, including the ability to serve demand during all hours of

the year, even when normal power system failures occur. The model includes several measures

(and associated costs) to address the variable output of renewable resources, including additional

operating reserves, fuel storage, cycling of fossil plants, and additional equipment needed to

maintain system stability.

We evaluated three scenarios for comparison. The first scenario (referred to as No New RE) does

not allow for any new renewable capacity. The second (Reference) is a scenario without an RPS

requirement and represents the least-cost mix of resources. The third (RPS) enforces the RPS

trajectory where at least 80% of generation in the entire Railbelt must be derived from renewable

resources by 2040.

We assume that the following technologies (both existing and new) are eligible to meet RPS

requirements: wind, solar, geothermal, tidal, hydropower, biomass, and landfill gas—and we

include both existing and new deployments. Apart from retiring one relatively small power plant,

the model includes and maintains all existing hydropower and fossil generation resources that

continue to provide important reliability services. We also include the option to add new fossil

fuel generators and energy storage. We capture the impact of existing federal tax credits,

including the 40% investment tax for energy communities detailed in the main report, but

assume no other changes to state or federal policies. We assume load growth resulting from

population increases and electric vehicle (EV) adoption, with EV demand driving most of this

growth (we assume that 20% of all vehicles in the Railbelt are electrified by 2040.)

The primary goal of this current study is to examine differences in total electricity system costs

associated with deploying various amounts of renewable energy. In all scenarios, there will be

many common costs, including maintenance of existing transmission and distribution assets,

existing debt on generation assets, existing power purchase agreements, and many administrative

costs. These are shown at the bottom of Figure ES-1. Because the goal of this study is to

compare differences in system costs resulting from different generation mixes, we do not

estimate these common costs. Instead, we focus on factors that may vary across the different

scenarios, including investments in new fossil and renewable generators, and all fuel and other

1 The Railbelt power system extends from Fairbanks through Anchorage to the Kenai Peninsula and consists of five

utilities: the Golden Valley Electric Association, Chugach Electric Association, the Matanuska Energy Association,

City of Seward, and Homer Electric Association.

vii

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

variable costs from both new and existing resources. The system cost includes measures needed

to address the variability and uncertainty of renewable energy, sometimes referred to as

“integration costs.” Throughout this report, all results are presented in $2023.

Figure ES-1. Types of energy system costs considered in the analysis, depicted for two of the

three scenarios assessed (Reference and RPS). Because the overall study objective is to estimate

the difference in costs among the three scenarios, common costs are not considered in the

analysis.

The study presents six key findings.

Finding #1: The Least-Cost (Reference) Scenario Results in Substantial Deployment of

Renewable Energy and Cost Savings

The primary driver for economic deployment of new renewables is their ability to reduce the

quantity of fuel used in the existing fossil generators that serve the majority of Railbelt demand.

The cost of gas generation is expected to increase substantially because of the expected need for

imported liquified natural gas (LNG) at costs of at least $12.6 per million cubic feet ($2023)

starting in 2028.

2

This results in fuel-related costs of the most-efficient (lowest-cost) gas-

powered plants in the Railbelt increasing to more than $90/MWh in the late 2020s. Because of

continued technology improvements and the assumed eligibility of wind and solar for the 40%

investment tax credit (ITC), the cost of acquiring new solar and wind resources is expected to be

substantially less than the cost of fuel for existing natural-gas-powered generators. Cost and

performance of renewable technologies is based on the mid-case projections from the National

Renewable Energy Laboratory’s (NREL’s) 2023 Annual Technology Baseline, and an Alaska-

specific multiplier was applied to reflect higher capital and operating costs in Alaska. This result

2

$12.2 per million CF in $2023.

New Fossil Fixed and

Variable Costs

Existing Fossil Generator

Fuel and Variable Costs

Reference Case

RPS Case

New Fossil Fixed and

Variable Costs

Existing Fossil Generator

Fuel and Variable Costs

Existing Debt and PPA Obligations

Distribution System Costs

New Renewable and

Storage Costs

Common New Capital and Fixed Costs (Generation,

Transmission, and Storage)

Costs

not

considered

in this study

Costs

considered

in this study

$

Renewable Costs Include:

• Capital

• Operations and Maintenance

• Interconnection

• Transmission spur line

• Additional natural gas storage

• Grid-forming inverters

• Additional operating reserves

• Scheduling, forecasting, and

communication

• Curtailed energy

New Renewable and

Storage Costs

Fossil Generator Costs Include:

• Reduction in efficiency from

operating at

part load

• Additional stops and starts

viii

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

in levelized costs that are expected to be below $80/MWh for solar and below $70/MWh for

wind in the coming years. These costs are before consideration of the additional need for new

wind transmission interconnections, natural gas fuel storage, and impacts of addressing

renewable variability, which are included in the full cost accounting and discussed in more detail

in Finding #6.

After the impact of the need to address variability and uncertainty of the wind and solar is

included, these resources achieve “breakeven” conditions with variable costs of the most

efficient gas plants operating on imported LNG. As a result of this growing cost differential, the

model chooses to build large amounts of wind and some solar to reduce overall system costs, and

the Reference scenario reaches a 76% contribution from renewables by 2040 (Figure ES-2). (We

discuss potential trends that may occur after 2040 in Section 7.7.4.)

Figure ES-2. Contribution of renewable energy to the Alaska Railbelt grid in the Reference and No

New RE scenarios

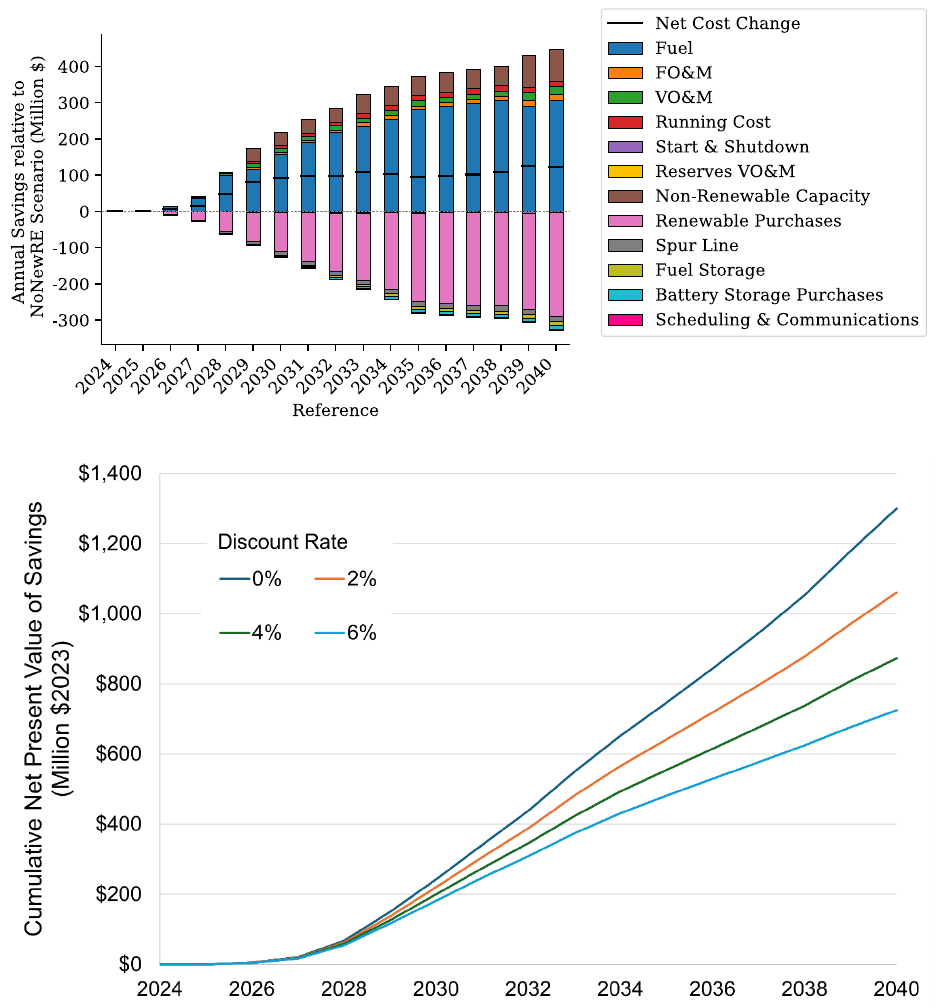

Figure ES-3 compares the evaluated costs in these scenarios, meaning the total of all system

costs that may vary across the different scenarios (fixed costs for new generators and variable

costs for all existing and new generators). Costs that do not vary across scenarios (e.g., servicing

existing debt, transmission, and distribution costs) are not included in these comparisons. Figure

ES-3 (top) shows the annual cost difference between the No New RE and Reference scenarios,

with savings shown as a positive value and costs shown as negative. The increased cost of

renewable energy purchases is more than offset by the decrease in fuel-related costs, which

produces a net savings (black line) which averages about $105 million/year from 2030 to 2040.

The Reference scenario avoids about $4.2 billion in fuel and other costs from 2024 to 2040. This

avoided cost requires renewable purchases and other costs of about $2.9 billion, resulting in a

cumulative (non-discounted) savings from 2024 to 2040 in the Reference scenario of about $1.3

ix

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

billion. Figure ES-3 (bottom) summarizes the difference in cumulative net present value (NPV)

of evaluated costs over the evaluation period (2024–2040), across a range of discount rates.

Figure ES-3. Total annual savings ($2023) associated with the Reference scenario compared to the

No New RE scenario (top) shows annual savings of about $100 million per year in the early 2030s.

The cumulative (non-discounted) savings from 2024 to 2040 (bottom) reaches $1.3 billion. The net

present value of those cumulative savings is less, depending on discount rate used.

x

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

Finding #2: The Least-Cost (Reference) Scenario Relies on a Mix of Renewable Energy

Resources and Locations

The Reference scenario deploys a mix of wind and solar resources, with wind providing most of

the new capacity, growing to about 51% of annual generation in 2040. Figure ES-4 shows the

capacity mix (top) and generation mix (bottom) between 2024 and 2040 for the No New RE and

Reference scenarios.

a) Capacity by type

b) Generation by type

Figure ES-4. Capacity (top) and generation mix (bottom) over time in the No New RE and

Reference scenarios

Finding #3: The 80% RPS Has Limited Impact on System Costs, With Much Greater

Uncertainty Driven by Future Costs of Renewables and Other Resources

Adding the RPS requirement has a small impact on the overall savings associated with

deployment of renewable energy compared to the Reference scenario. The Reference (least-cost)

scenario achieves a 76% contribution from renewable resources in 2040. Above this level of

renewable generation, additional renewables have a slightly higher cost than operating existing

gas plants based on the increasing curtailment (unusable generation) of wind and solar during

periods when the supply of renewables exceeds electricity demand. We assume that all

renewable energy must be paid for regardless of whether it is used.

xi

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

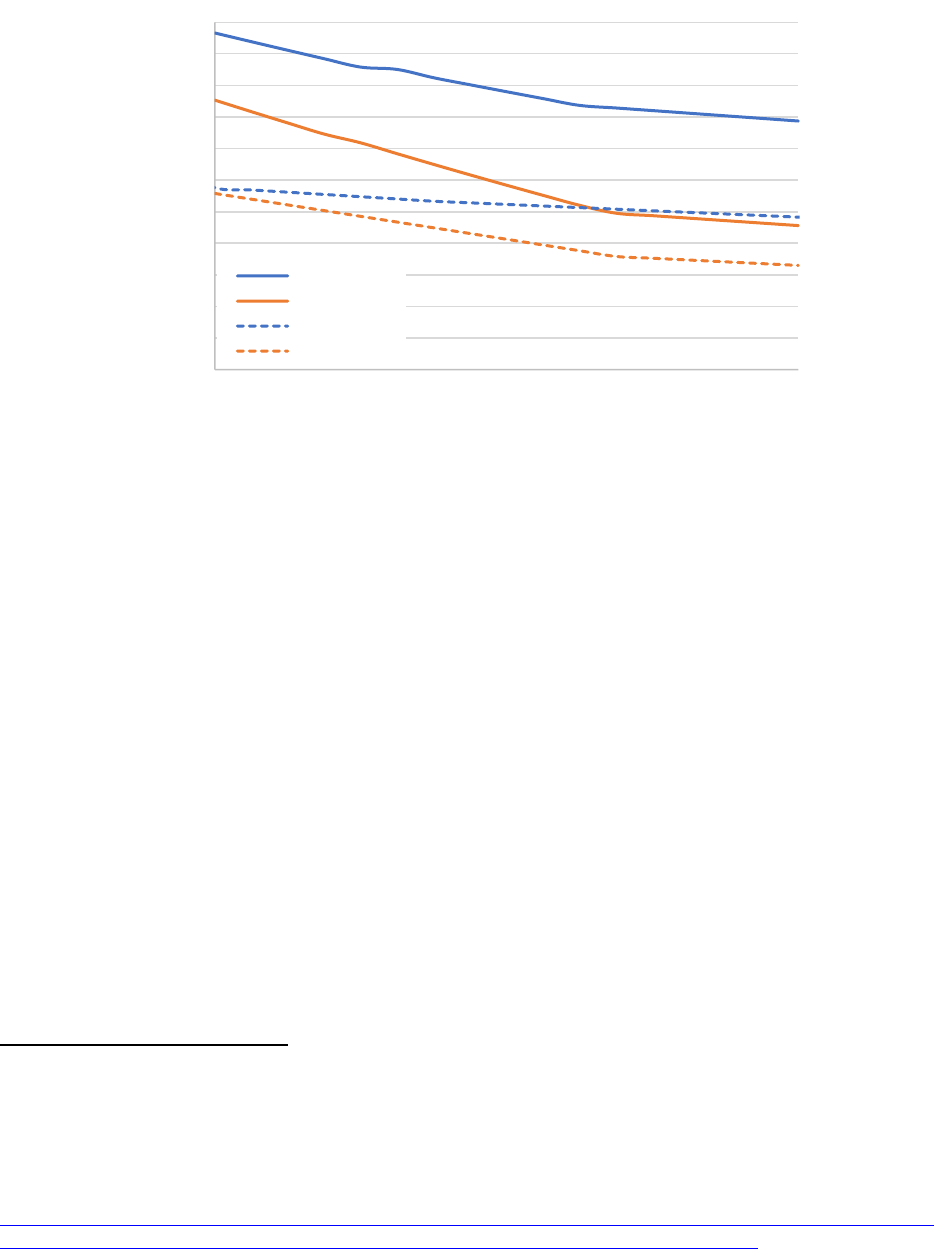

Figure ES-5 shows the annual savings associated with the Reference and RPS scenarios

compared to the No New RE scenario. The Reference (blue) line is the annual savings shown

previously in ES-3 (top). The RPS line shows the reduction in savings associated with the RPS

scenario resulting in about a $19 million cost (or $19 million reduction in benefits compared to

the Reference scenario) in 2040. This is less than a 2% decrease in cumulative savings. Because

the additional cost occurs almost entirely in 2040 and given the significant uncertainty in future

costs of renewables, fossil fuels, load growth, and other factors, there is essentially no

meaningful difference between the Reference scenario and the 80% RPS scenario. For

comparison, Figure ES-5 also shows how changes in the cost of renewables would have a greater

impact on the overall benefits of deploying renewable resources. A 10% reduction in the cost of

renewables (blue line) would increase the cumulative (non-discounted) savings by about $220M

from 2024 to 2040 (to nearly $1.6 billion). Increasing the cost of renewables by 20% (purple

line) reduces the cumulative benefits by about $470 M (to about $900 million).

Figure ES-5. Requiring an 80% RPS reduces net savings associated by deploying renewable

energy by about $19 million in 2040, which is less than a 2% change in cumulative savings.

Overall, these differences are very small given the large uncertainty in future costs of fuels and

renewable generation demonstrated by the much larger impact of a change in the assumed cost

of renewable energy shown in the high- and low-cost renewable energy sensitivities.

These results suggest that any increase in system costs associated with an 80% RPS (compared

to the Reference scenario) are likely to occur well past 2030, when there will be greater

technological certainty and adjustments to RPS targets could be made to ensure least-cost

deployments.

xii

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

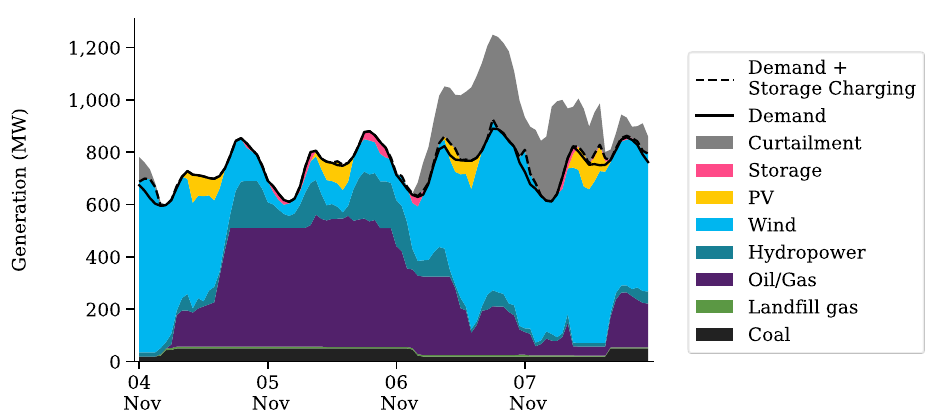

Finding #4: Demand Is Met in All Scenarios, Relying Heavily on Use of Existing Hydro and

Fossil-Fueled Generators During Periods of Low Renewable Output

Wind and solar resources provide significant cost savings by avoiding fuel use in existing

generators, but maintaining reliable operation in these scenarios depends significantly on

continued use of existing hydropower and fossil generators. There are many periods of low wind

and solar output, and these periods can last for many hours. This demonstrates a fundamental

change in how electricity generation is planned, where renewables may provide the majority of

the energy requirements on an annual basis, but with fossil resources providing a larger fraction

of the capacity requirements.

Finding #5: High-RE Systems Will Require Substantial Changes to How the System Is

Operated

The use of highly variable resources will require changes to how the system will maintain

supply-and-demand balance. These changes include increased variation in output from existing

fossil and hydropower plants and variation in transmission flows along the interties. We assume

that planning and operating are performed in a coordinated manner to minimize cost and ensure

resource adequacy and operational reliability across the entire Railbelt system, but that each

utility can operate independently. This kind of operation, including Railbelt-wide joint dispatch,

may require changes to contractual agreements or other practices to minimize the costs of

operating the system.

The system will need to rely increasingly on dispatching wind and solar generators by curtailing

their output (but still paying for the lost energy production at full price). The output from wind

power plants can be controlled over the available output range in less than 1 minute, while the

output from solar can be controlled over its output range in a few seconds. This will be needed to

maintain supply/demand balance but also for the provision of operating reserves from renewable

resources. Although the majority of operating reserves are derived from storage and existing

fossil and hydropower plants, wind and solar may play an increasing role in providing operating

reserves.

Finding #6: Cost Impacts of Addressing Variability and Uncertainty Are Modest Relative

to Savings but With Remaining Uncertainties

All results presented in this analysis include the impact of several factors associated with

integrating renewables and addressing variability and uncertainty, which increases the cost or

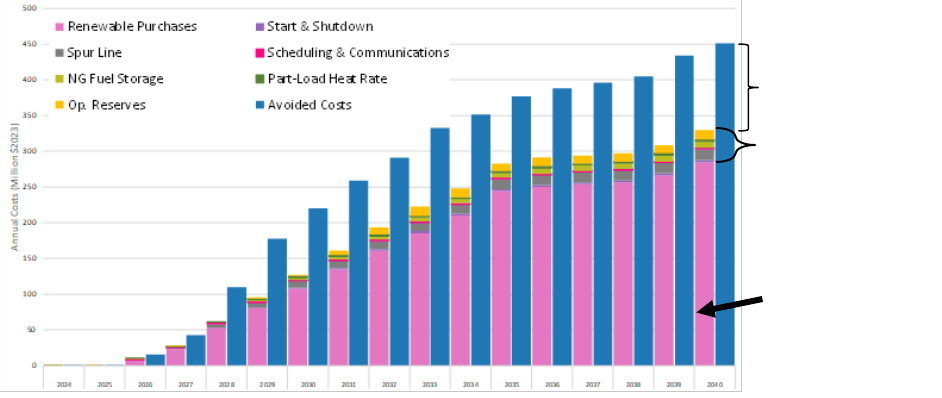

reduces the net value of renewable energy. To clarify these changes in costs, Figure ES-6

illustrates how addressing renewable variability and uncertainty impacts the net overall value of

renewable energy seen in the Reference scenario.

The left set of bars shows the total costs of renewable energy purchases and integration. The

bottom (pink) bar is the cost of renewable purchases, which captures all the annual fixed and

variable costs from the wind and solar power plants. By 2040, these direct project costs are about

$285M/year. Additional direct costs assumed for both wind and solar include spur line cost and

substation upgrades, natural gas storage and scheduling, communication, and forecasting, adding

about $27M/year by 2040. Additional factors include the costs associated with additional starts

and stops of power plants, the reduction in avoided natural gas associated with responding to

xiii

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

variability and uncertainty, and additional operating reserves. These are “embedded” in the

results seen previously, but additional analysis was performed to isolate these costs—which are

estimated at about $18M/year by 2040. Combined, integration-related factors add about

$45M/year in 2040 to the cost of purchasing solar and wind energy.

The right set of bars shows the value of the fuel and variable costs avoided by this generation.

The difference in the total renewables cost (left bars) and avoided costs (right) produce the net

value, which averages about $105 million per year beginning in 2030 as shown in Finding #1.

Figure ES-6. Annual costs of renewable energy, including integrating and addressing resource

variability, are shown in the left set of bars. These costs are included in all scenarios but are

broken out here for clarity. These increase renewable costs by about 16% compared to only the

cost of the renewable generator and interconnection. The right bars show the value of avoided

variable costs, with the difference being the net savings associated with renewable deployment.

These impacts are important not only to accurately assess the value of variable and uncertain

resources but also to consider when allocating system costs across multiple utilities. There is still

considerable uncertainty about some of these factors, particularly natural gas fuel storage.

Additional issues related to maintaining system stability with high levels of inverter-based

resources must also be addressed and may incur additional costs, which can be compared to the

annual savings.

Conclusions and Caveats

The high projected prices for natural gas in the Railbelt region make the addition of renewable

resources potentially cost-competitive despite challenges including development costs, moderate

resource quality, and the small system size, which increase the relative impact of variability and

uncertainty. Based on the assumptions used in this analysis, achieving more than a 75%

contribution of renewables toward Railbelt electricity by 2040 appears to be the least-cost option.

Moving to an 80% RPS slightly decreases the cumulative cost savings that result from

0

50

100

150

200

250

300

350

400

450

500

2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038 2039 2040

Annual Costs (Million $2023)

Renewable Purchases Start & Shutdown

Spur Line Scheduling & Communications

NG Fuel Storage

Part-Load Heat Rate

Op. Reserves

Avoided Costs

xiv

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

renewables deployment (by about 1%) because the mismatch of renewable supply and electricity

demand limits the ability of renewables to displace the remaining fossil generation without

further cost reductions or use of new technologies such as seasonal storage.

There are several significant uncertainties around the scenarios evaluated in this work. Among

them are the potential load growth driven by EVs and the future price of natural gas.

This analysis was conducted based on the information available within timing constraints. It is a

starting point for additional research and consideration of investment or policy options. Other

factors that can inform decision making are not considered here. The analysis results are not

intended to be the sole basis of investment, policy, or regulatory decisions but are rather intended

to improve the understanding of the cost impacts of an 80% RPS. Only direct costs are

measured; other potential benefits of renewable energy such as energy security and reduced

exposure to fuel price volatility are not considered. We also do not consider potential benefits

associated with improved local air quality, which is a concern in several areas of Alaska’s

Railbelt that are at, or nearing, nonattainment status for fine particulate matter (PM

2.5

).

Additional modeling will be required to further validate the findings of this work, including

changes and associated additional costs that are likely needed to ensure stable operation when

nearly all the grid’s electricity is being derived from inverter-based wind, solar, and storage.

xv

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

Table of Contents

Acknowledgments ..................................................................................................................................... iv

List of Acronyms ......................................................................................................................................... v

Executive Summary ................................................................................................................................... vi

Table of Contents ...................................................................................................................................... xv

List of Figures ......................................................................................................................................... xvii

List of Tables ............................................................................................................................................ xix

1 Introduction ........................................................................................................................................... 1

1.1 Study Goals ................................................................................................................................... 1

1.2 General Approach ......................................................................................................................... 3

1.3 Caveats 3

2 Overview of the Alaska Railbelt System ............................................................................................ 4

3 Modeling Methods and Assumptions ................................................................................................. 7

3.1 Modeling Approach ....................................................................................................................... 7

3.1.1 Capacity Expansion Modeling ......................................................................................... 7

3.1.2 Production Cost Modeling ............................................................................................... 8

3.2 Reliability- and Resource-Adequacy-Related Assumptions ......................................................... 8

3.2.1 Planning and Operation .................................................................................................... 8

3.2.2 Resource Adequacy (Planning Reserve Margin) Assumptions ........................................ 9

3.2.3 Operational Reliability Assumptions ............................................................................... 9

3.3 Addressing Wind and Solar Variability and Uncertainty .............................................................. 9

3.3.1 Increased Cycling and Part-Load Operation of Thermal Plants ..................................... 10

3.3.2 Increased Operating Reserves ........................................................................................ 10

3.3.3 Natural Gas Fuel Storage ............................................................................................... 12

3.3.4 Renewable Curtailment .................................................................................................. 13

3.3.5 Renewable Scheduling and Forecasting ......................................................................... 13

3.3.6 Accommodating Inverter-Based Resources ................................................................... 13

4 Scenarios Evaluated .......................................................................................................................... 13

4.1 Scenario Overview ...................................................................................................................... 13

4.2 RPS Target .................................................................................................................................. 14

4.3 Eligible Technologies .................................................................................................................. 14

4.4 Other Policies .............................................................................................................................. 15

5 Reference Assumptions .................................................................................................................... 16

5.1 Load 16

5.1.1 Load Shape ..................................................................................................................... 16

5.1.2 Prescribed Load Growth, Including Electric Vehicles ................................................... 18

5.2 Generation Resources .................................................................................................................. 19

5.2.1 Existing Generation Resources ...................................................................................... 19

5.2.2 Assumed Base Scenario Retirements and Additions ..................................................... 20

5.3 Transmission ............................................................................................................................... 20

5.4 Fuel Prices ................................................................................................................................... 21

6 New Generator Availability, Cost, and Performance Assumptions .............................................. 24

6.1 Technologies Evaluated .............................................................................................................. 24

6.1.1 Completion Dates ........................................................................................................... 25

6.1.2 Treatment of Customer-Sited Resources ........................................................................ 26

6.2 Cost Assumptions ........................................................................................................................ 26

6.3 Resource Availability and Performance ...................................................................................... 29

6.4 Financing Assumptions ............................................................................................................... 29

6.4.1 Treatment of Tax Credits in the Inflation Reduction Act............................................... 29

6.5 Levelized Cost/PPA Price Summary ........................................................................................... 30

7 Key Findings ....................................................................................................................................... 33

xvi

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

7.1 Finding #1: The Least-Cost (Reference) Scenario Results in Substantial Deployment of

Renewable Energy and Cost Savings .......................................................................................... 33

7.2 Finding #2: The Least-Cost (Reference) Scenario Relies on a Mix of Renewable Energy

Resources and Locations ............................................................................................................. 36

7.3 Finding #3: The 80% RPS Has Limited Impact on Costs Compared to the Reference (Least-

Cost) Scenario ............................................................................................................................. 40

7.4 Finding #4: Demand Is Met in All Scenarios, Relying Heavily on Existing Hydro and Fossil-

Fueled Generators During Periods of Low Renewable Output ................................................... 41

7.5 Finding #5: Large Contributions of Renewable Generation Will Require Substantial Changes to

How the System Is Operated ....................................................................................................... 43

7.5.1 Increased Ramping and Part-Load Operation of Thermal Plants ................................... 44

7.5.2 Changes in Hydropower Plant Operation ....................................................................... 47

7.5.3 Changes to Intertie Flow ................................................................................................ 48

7.5.4 Renewables Dispatch for Balancing Load and for Reserve Provision ........................... 51

7.6 Finding #6: Cost Impacts of Addressing Variability and Uncertainty Are Modest Relative to

Savings but With Remaining Uncertainties ................................................................................ 53

7.7 Additional Findings ..................................................................................................................... 56

7.7.1 Potential Distributed PV Adoption Must Be Evaluated in the Context of Incentives and

Rate Structure Changes .................................................................................................. 56

7.7.2 The Small Increase in Costs Associated With an 80% RPS Are Largely Because of

Renewable Curtailment .................................................................................................. 59

7.7.3 There May Be Additional Costs or Operational Requirements To Address the Reduced

Role of Synchronous Generation and Increased Contribution of Inverter-Based

Resources ....................................................................................................................... 62

7.7.4 Replacing Retiring Renewables Beyond 2040 Should Be Less Expensive Than

Additional Natural Gas Generation ................................................................................ 63

8 Conclusions ........................................................................................................................................ 64

Appendix A. Capacity- and Energy-Related Terms ........................................................................ 65

Appendix B. Base Modeling Assumptions ...................................................................................... 66

B.1 Utility-Owned Fossil Generators ................................................................................................. 66

B.2 Heat Rate and Start Cost Modeling ............................................................................................. 67

B.3 Treatment of CHP Plants and Other Nonutility-Owned Generators ........................................... 68

B.4 Hydropower ................................................................................................................................. 68

B.5 Other Existing Resources ............................................................................................................ 69

B.6 Electric Vehicle Adoption ........................................................................................................... 70

B.7 Operating Reserves ..................................................................................................................... 71

Appendix C. Generator Cost and Performance Assumptions for New Resources ..................... 73

C.1 Land-Based Wind ........................................................................................................................ 73

C.2 Offshore Wind ............................................................................................................................. 78

C.3 Solar (PV) .................................................................................................................................... 79

C.4 Rooftop and Distributed Solar ..................................................................................................... 79

C.5 Geothermal .................................................................................................................................. 80

C.6 Hydropower ................................................................................................................................. 83

C.7 Biomass and Landfill Gas ........................................................................................................... 85

C.8 Energy Storage ............................................................................................................................ 85

C.9 Summary Cost and Financial Parameters for Renewable Generators and Storage ..................... 87

C.10 New Fossil ................................................................................................................................... 90

xvii

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

List of Figures

Figure ES-1. Types of energy system costs considered in the analysis, depicted for two of the three

scenarios assessed (Reference and RPS). Because the overall study objective is to estimate

the difference in costs among the three scenarios, common costs are not considered in the

analysis. .................................................................................................................................. vii

Figure ES-2. Contribution of renewable energy to the Alaska Railbelt grid in the Reference and No New

RE scenarios .......................................................................................................................... viii

Figure ES-3. Total annual savings ($2023) associated with the Reference scenario compared to the No

New RE scenario (top) shows annual savings of about $100 million per year in the early

2030s. The cumulative (non-discounted) savings from 2024 to 2040 (bottom) reaches $1.3

billion. The net present value of those cumulative savings is less, depending on discount rate

used. ........................................................................................................................................ ix

Figure ES-4. Capacity (top) and generation mix (bottom) over time in the No New RE and Reference

scenarios ................................................................................................................................... x

Figure ES-5. Requiring an 80% RPS reduces net savings associated by deploying renewable energy by

about $19 million in 2040, which is less than a 2% change in cumulative savings. Overall,

these differences are very small given the large uncertainty in future costs of fuels and

renewable generation demonstrated by the much larger impact of a change in the assumed

cost of renewable energy shown in the high- and low-cost renewable energy sensitivities. .. xi

Figure ES-6. Annual costs of renewable energy, including integrating and addressing resource variability,

are shown in the left set of bars. These costs are included in all scenarios but are broken out

here for clarity. These increase renewable costs by about 16% compared to only the cost of

the renewable generator and interconnection. The right bars show the value of avoided

variable costs, with the difference being the net savings associated with renewable

deployment. ........................................................................................................................... xiii

Figure 1. Types of energy system costs considered in the analysis, depicted for two of the three scenarios

assessed (Reference and RPS). Because the overall study objective is to estimate the

difference in costs among the three scenarios, common costs are not considered in the

analysis. .................................................................................................................................... 2

Figure 2. Map of Alaska’s Railbelt power system ........................................................................................ 6

Figure 3. Summary of study modeling flow ................................................................................................. 7

Figure 4. Daily and seasonal generation profiles for 2018 ......................................................................... 17

Figure 5. Assumed fuel price projection ..................................................................................................... 22

Figure 6. Fuel cost projection for existing fossil-fueled plants using 2022 reported heat rate values ........ 23

Figure 7. Assumed Alaska cost multipliers added to all capital costs and O&M costs for renewable

generators and batteries .......................................................................................................... 27

Figure 8. Assumed overnight capital cost for utility-scale PV and land-based wind. Costs do not include

fuel storage or spur line costs, which are calculated separately. ............................................ 28

Figure 9. Example of assumed cost trajectories for wind and solar assuming a 37% capacity factor for

wind and a 17% capacity factor for solar. Costs (in $2023) are fixed for a 25-year period

from the date of completion and include the 40% ITC. This example represents a small

subset of the complete set of resources and locations available and does not include

additional costs associated with interconnection and addressing resource variability. .......... 30

Figure 10. The assumed PPA price trajectory for wind for a location with a 37% capacity factor. The

black line is the initial cost in constant $2023. The solid lines are the contract costs for

projects constructed in 2026 and 2030 in $2023. The dotted lines are the cost in actual

(nominal) dollars assuming a 2.5% escalator. ........................................................................ 31

Figure 11. Wind LCOE supply curve for 2026 and 2030, including spur line cost and variation in capacity

factor. Costs (in $2023) are fixed for a 25-year period from the date of completion and

include a 40% ITC for both the wind plant and spur line. ..................................................... 32

xviii

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

Figure 12. Contribution of renewable energy increases to about 76% in the Reference scenario .............. 33

Figure 13. Total annual costs ($2023) in the No New RE and Reference scenarios (top) and the net

savings (bottom) resulting from deployment of renewable energy. This includes only

evaluated costs and not costs common to all scenarios. Color key applies to both figures. Net

savings average about $105 million/year from 2030 to 2040. ............................................... 35

Figure 14. The cumulative (non-discounted) savings from 2024 to 2040 reach $1.3 billion. The net

present value of those cumulative savings is less, depending on discount rate used. NPV of

net savings does not include costs and savings that occur past 2040. .................................... 36

Figure 15. Capacity (top) and generation mix (bottom) over time in the No New RE and Reference

scenarios ................................................................................................................................. 37

Figure 16. Location of wind and solar power plants deployed in the Reference scenario. Wind plants

indicated by location and size. Solar is indicated by the amount deployed in each zone but

not located in any specific location. ....................................................................................... 39

Figure 17. Requiring an 80% RPS reduces the net savings from deploying renewable energy by about $19

million in 2040, which is less than a 2% change in cumulative savings. Overall, these

differences are very small given the large uncertainty in future costs of fuels and renewable

generation demonstrated by the much larger impact of a change in the assumed cost of

renewable energy shown in the high- and low-cost RE sensitivities. .................................... 41

Figure 18. System dispatch during the period of peak demand (a), a period of peak fossil plant output (b),

and a period of minimum wind renewable output (c) demonstrating the reliance on existing

hydropower and fossil generators to provide resource adequacy........................................... 42

Figure 19. Fraction of load met by wind and solar shows dramatic variability on an hourly and daily basis

................................................................................................................................................ 43

Figure 20. An example period in the 2040 Reference scenario with a rapid change in renewable output

and response from hydropower and fossil generators ............................................................ 44

Figure 21. Response of Railbelt fossil fuel generators (orange) to a large reduction in wind and solar

output (gray) on November 4, 2040, in the Reference scenario ............................................. 45

Figure 22. Transition of the Southcentral combined-cycle plant from base load to load-following and

peaking operation ................................................................................................................... 46

Figure 23. Declining capacity factor of Central region combined-cycle plants .......................................... 47

Figure 24. Operation of the Bradley Lake hydropower plant during periods of highly variable renewable

output ..................................................................................................................................... 48

Figure 25. Flow on the Alaska Intertie (black) in 2040 in the Reference scenario depends largely on the

supply of wind (orange) in the GVEA region. Positive numbers represent a flow from GVEA

to the Central region. .............................................................................................................. 49

Figure 26. Regional transmission flows, where positive values represent flows from north to Central (AK

Intertie) and south to Central (Kenai Intertie) ........................................................................ 50

Figure 27. Total annual operating (upward) reserves provision by generator type (top) in the No New RE

and Reference scenarios. Total requirement is the black bar. Reserves requirement by type

for the Reference scenario is shown in the bottom. The same legend applies to all plots. .... 52

Figure 28. Annual fossil plant start costs are about $3 million greater per year by the early 2030s in the

Reference scenario compared to the No New RE scenario .................................................... 53

Figure 29. Annual costs ($2023) of renewable energy, including integration and addressing resource

variability, are shown in the left set of bars. These costs are included in all scenarios but are

broken out here for clarity. These increase renewable costs by about 16% compared to the

cost of only the renewable generator and interconnection. The right (blue) bars show the

value of avoided variable costs, with the difference being the net savings associated with

renewable deployment. .......................................................................................................... 55

Figure 30. Daily natural gas fuel consumption in 2040 .............................................................................. 56

Figure 31. Changes in generation mix between the Reference scenario and DPV sensitivity .................... 57

xix

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

Figure 32. Changes in annual costs, with the DPV sensitivity (top) showing reduction in required utility

expenditures. The avoided cost associated with the DPV sensitivity (bottom) shows the costs

utilities would have to pay for electricity to replace the DPV. .............................................. 58

Figure 33. Curtailment occurring on a 5-day period in 2030 with annual renewable contribution of 54%

(top) and 2032 (bottom) when the annual contribution of renewables has increased to 64% 60

Figure 34. Annual wind and solar curtailment rate shows a dramatic increase when renewable

contribution exceeds 50%-60% .............................................................................................. 61

Figure 35. Example simplified heat rate curve for the Southcentral combined-cycle generator ................ 68

Figure 36. EV adoptions (top) and Reference scenario charging profiles in 2040 (bottom) ...................... 71

Figure 37. Railbelt wind resource and location of wind site evaluated ...................................................... 74

Figure 38. Assumed LCOE/PPA price projections for utility-scale wind operating with an average) (not

including transmission). The PPA price is fixed (in real $2023) for 25 years from the year of

installation, which corresponds to an escalation at the rate of inflation in nominal dollars. .. 77

Figure 39. CapEx projections for offshore wind (top) and LCOE/PPA price projections assuming a 51%

capacity factor (bottom). Cost assumes underwater transmission line connecting to the HEA

system near Homer. The PPA price is fixed for 25 years from the year of installation. ........ 78

Figure 40. Assumed distributed/rooftop PV adoption in the DPV sensitivity ............................................ 80

Figure 41. Assumed geothermal capital cost (top) and LCOE (bottom) .................................................... 81

Figure 42. Potential locations for geothermal resources in Alaska ............................................................. 82

Figure 43. Location of existing and potential new hydropower resources ................................................. 84

Figure 44. Assumed output profile (fraction of installed capacity) for new run-of-river hydropower ....... 85

Figure 45. Assumed battery cost trajectory ($2023 with a 15 year life) ..................................................... 86

List of Tables

Table 1. Characteristics of Alaska’s Railbelt Utilities .................................................................................. 4

Table 2. 2022 Railbelt Utility Generation Mix ............................................................................................. 4

Table 3. Assumed Railbelt RPS Requirement Based on Proposed Senate Bill 101 ................................... 14

Table 4. Assumed Load Growth Based on Population (before addition of electric vehicles) .................... 18

Table 5. Initial (2024) Generation Resource Mix for the Utilities in Alaska’s Railbelt ............................. 19

Table 6. Supply-Side Technologies Considered ......................................................................................... 25

Table 7. Capacity and Generation by Type in 2040 .................................................................................... 38

Table B-1. Existing Railbelt Fossil Fuel Generators (data as reported to EIA) .......................................... 66

Table B-2. Average Heat Rate for Major Fossil Fuel Generators (producing at least 70 GWh in 2022) ... 67

Table B-3. Existing Railbelt Hydropower Plants ........................................................................................ 69

Table B-4. Monthly Water Budget for Existing Railbelt Hydropower Plants ............................................ 69

Table B-5. Existing Railbelt Renewable Generators .................................................................................. 70

Table B-6. Summary of Operating Reserve Modeling ............................................................................... 72

Table C-1. Location and Performance of Available Wind Sites Evaluated ................................................ 76

Table C-2. Overnight Capital Costs (2023$/kW) ....................................................................................... 87

Table C-3. Fixed Charge Rates, Including the Impact of the ITC .............................................................. 88

Table C-4. PTC Value (2023$/MWh): Applied If the Model Chooses To Take the PTC With the Higher

Fixed Charge Rate .................................................................................................................. 89

Tab

le C-5. Fixed O&M Value (2023$/kW-year) ........................................................................................ 90

Table C-6. CT and CCGT Power Plant Cost Estimates .............................................................................. 91

Table C-7. Capital Cost and Fixed Charge Rate for CT, CC, and Coal Plants ........................................... 92

1

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

1 Introduction

The Alaska Railbelt utilities face growing challenges associated with the declining supply of

natural gas from the Cook Inlet, with substantial price increases projected. Because of this,

renewable energy in the form of wind and solar is a potentially cost-competitive option to reduce

reliance on natural gas, which in 2022 provided nearly two-thirds of the Railbelt electricity

demand.

This study performs an analysis of the system costs and benefits of adding renewable energy to

the Alaska Railbelt grid. The study is motivated in part by a proposed 80% renewable portfolio

standard (RPS).

3

1.1 Study Goals

The primary goal of this current study is to examine differences in total system costs associated

with deploying various amounts of renewable energy. We examine three main scenarios: 1) a

scenario where no additional renewable energy is added, 2) a reference scenario that develops

the least-cost mix of resources, and 3) an 80% RPS scenario.

The cost framework is conceptually illustrated in Figure 1. In all scenarios, there are many

common costs, shown at the bottom of Figure 1. Because the goal of this study is to compare

differences in costs resulting from different generation mixes, we do not estimate these common

costs.

4

This study examines the elements shown at the top of Figure 1, including all factors that

may vary under different portfolios and listed next.

3

Described in proposed Senate Bill No. 101 33-LS0365\R at https://www.akleg.gov/PDF/33/Bills/SB0101A.PDF.

4

Estimating total costs will be required to determine total revenue requirements and establishing rates and rate

structures across various customer classes.

2

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

Figure 1. Types of energy system costs considered in the analysis, depicted for two of the three

scenarios assessed (Reference and RPS). Because the overall study objective is to estimate the

difference in costs among the three scenarios, common costs are not considered in the analysis.

Cost considered in the study include the following:

• Capital costs and fixed operations and maintenance (O&M) for all new renewable and

fossil generators. For renewables, this could be obtained via a power purchase agreement

(PPA).

• Cost premiums for siting and operating in Alaska.

• Variable costs associated with all existing plants and new plants, including fuel and

O&M. This includes changes to fossil plant operation because of increased variability

from:

o Impacts of part-load heat rate because of increased cycling and load following

o Additional startup costs of fossil plants.

• Costs associated with integrating new renewable resources, including:

o Additional operating reserves

o Grid-forming inverters

o Additional natural gas fuel storage

o Curtailment

o Scheduling, communication, and forecasting costs

o New transmission spur lines and substation upgrades.

Costs not included are those that are not expected to change across the various scenarios:

• Debt on existing assets and existing PPAs

• Fixed O&M on existing assets

Reference Case

RPS Case

Existing Fossil Generator

Fuel and Variable Costs

Costs that do not vary across scenarios

Costs not

considered

in this study

Costs

considered

in this study

$

New Generator and

Storage Costs

Existing Fossil Generator

Fuel and Variable Costs

New Generator and

Storage Costs

3

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

• Administrative and billing costs

• 86 MW of energy storage currently proposed or under development

• Distribution system costs

• Maintenance and upgrades of the existing transmission network not associated with new

renewable generators

• Upgrades to the Kenai Intertie associated with the Railbelt Innovative Resiliency Project

• Infrastructure associated with electric vehicles (EVs).

1.2 General Approach

The study follows the traditional principles of least-cost resource planning, sometimes referred to

as integrated resource planning. The study uses a standard commercially available model that

simulates the evolution and operation of the power system to identify the mix of resources that

maintains system reliability at the lowest life cycle cost. It begins with the existing generation

mix and adds new resources it identifies as providing electricity with the lowest overall cost,

considering all fixed and variable costs. The model tracks several reliability metrics, including

the ability to serve demand during all hours of the year, and maintains adequate reserves to

address generator failures. Across the various scenarios, we report differences in generation mix

and costs on both an annualized basis and net present value (NPV).

1.3 Caveats

This analysis was conducted based on the information available within timing constraints. It is a

starting point for additional research and consideration of investment or policy options. Other

factors that can inform decision making are not considered here. The analysis results are not

intended to be the sole basis of investment, policy, or regulatory decisions but are rather intended

to understand the cost impacts of increased renewable deployment, including impacts of an 80%

RPS. Only direct system costs are measured—other potential benefits of renewable energy such

as energy security and reduced exposure to fuel price volatility are not considered. We also do

not consider potential benefits associated with improved local air quality, which is a concern in

several areas of Alaska’s Railbelt that are at, or nearing, nonattainment status for fine particulate

matter (PM

2.5

).

5

5

State of Alaska Department of Transportation & Public Facilities, 2020–2023 Statewide Transportation

Improvement Program (STIP). Approved November 23, 2021, Amendment 3 and Incorporated Administrative

Modifications (State of Alaska Department of Transportation and Public Facilities, 2021).

https://dot.alaska.gov/stwdplng/cip/stip/assets/STIP.pdf

.

4

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

2 Overview of the Alaska Railbelt System

This analysis applies to Alaska’s Railbelt power system, which extends from Fairbanks through

Anchorage to the Kenai Peninsula and consists of four electric cooperatives and one municipally

owned (not-for-profit) utility that serve about 75% of Alaska’s electricity (Table 1).

6

Table 1. Characteristics of Alaska’s Railbelt Utilities

Data are for 2022 and from U.S. Energy Information Administration (EIA) Form 861.

a

Utility

Annual Sales

(GWh)

Customer

Accounts

(thousands)

Fraction of Railbelt

Annual Demand (%)

Chugach Electric Association

1,903 113

43

Golden Valley Electric Association

1,244 48

28

Matanuska Electric Association

766 69

17

Homer Electric Association

453 33

10

City of Seward Electric Department 53 3 1

Total

b

4,404 266 100

a

“Annual Electric Power Industry Report, Form EIA-861 detailed data files.” EIA,

https://www.eia.gov/electricity/data/eia861/.

b

This does not include about 254 GWh of electricity lost in transmission and distribution plus electricity

consumed by the utility. The total net generation requirement in 2022 was about 4,698 GWh.

Overall, the system obtains the majority of its electricity from fossil resources, summarized in

Table 2.

7

Table 2. 2022 Railbelt Utility Generation Mix

8

Technology

Capacity

(MW)

Energy

(GWh)

Generation

Fraction

Natural gas

1,332.6

3,052

64%

Coal

117.5

545

11%

Oil

268.9

444

9%

Hydropower

189.8

578

12%

Wind

44.5

107

2%

Landfill gas

11.5

41

1%

Total

1,965

4,766

100%

6

This table does not include some of the electricity consumed by large users that supply a portion of their own

demand, including the University of Alaska Fairbanks or military bases.

7

Data do not include the contribution from solar or small hydropower.

8

Totals may not add up to 100% because of rounding. Data from EIA Form 860 and Form 923 for the year 2022.

Only large generators are listed, and this does not include distributed resources. List includes Aurora but not CHP

5

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

Figure 2 illustrates Alaska’s Railbelt region. Fairbanks is served by the Golden Valley Electric

Association (GVEA). For the purposes of modeling, we combined the Chugach Electric

Association (serving Anchorage), the Matanuska Energy Association (MEA), and the City of

Seward Electric Department into a single zone we refer to as “Central” throughout this study.

The Homer Electric Association (HEA) serves the Kenai Peninsula.

plants at UAF, industrial, or military sites. https://www.eia.gov/electricity/data/eia860/;

https://www.eia.gov/electricity/data/eia923/.

6

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

Figure 2. Map of Alaska’s Railbelt power system

9

9

Data from Alaska Energy Data Gateway, Electric Service Areas. Alaska Energy Authority, 2020.

https://gis.data.alaska.gov/datasets/DCCED::electric-se

rvice-areas/explore?location=61.907409%2C-

147.863943%2C6.00.

7

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

3 Modeling Methods and Assumptions

This work studies the period from 2024 to 2040 and follows a standard least-cost planning

approach using models and general assumptions described in this section.

3.1 Modeling Approach

The study uses a modeling approach illustrated conceptually in Figure 3 and described in detail

next.

Figure 3. Summary of study modeling flow

10

3.1.1 Capacity Expansion Modeling

Capacity expansion analysis is the central modeling element of the study because it produces the

generation mix and estimates the total system costs associated with each scenario. Within the

capacity expansion modeling step, the study identifies future generation and transmission

portfolios to achieve renewable energy targets at least cost.

Modeling the expansion of the bulk power system, including utility-scale (noncustomer-sited)

generators and transmission, is performed with the PLEXOS Long-Term Model.

11

The capacity

expansion model (CEM) considers capital costs, fixed and variable O&M costs, and fuel costs,

moving forward in time in 1-year increments over the study period (2024–2040). Investment

decisions for the type, amount, and location of new capacity are determined with a least-cost

optimization that ensures the provision of power system resources required to meet load reliably

in all hours and meets all other constraints and policies.

10

Brinkman, Gregory, Dominique Bain, Grant Buster, Caroline Draxl, Paritosh Das, Jonathan Ho, and Eduardo

Ibanez et al. 2021. The North American Renewable Integration Study: A U.S. Perspective—Executive Summary.

Golden, CO: National Renewable Energy Laboratory. NREL/TP-6A20-79224-ES.

https://www.nrel.gov/docs/fy21osti/79224-ES.pdf

.

11

https://www.energyexemplar.com/plexos.

8

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

3.1.2 Production Cost Modeling

The production cost model (PCM) is used to simulate the hourly operations of the future systems

identified by the CEM and to validate the ability of those systems to balance generation and

load.

12

We use the PLEXOS Medium-Term/Short-Term model, a commercially available PCM

(sometimes referred to as a unit commitment and dispatch model). This is the same model used

in a previous NREL report that analyzed several aspects of how Alaska’s Railbelt grid might be

operated in 2040 when providing 80% of electricity generation from renewable energy

resources.

13

The system details generated by the CEM (types, capacities, and locations of transmission,

renewable generation, and conventional generation), are passed to the PCM, along with hourly

load and variable generation data and hourly operating reserve requirements.

14

The PCM

calculates operational costs and ensures that adequate reserves are maintained under the given set

of weather and load conditions.

15

This type of simulation is an iterative process. The PCM provides necessary feedback to the

CEM to determine more definitively if the built system can operate feasibly. If PLEXOS

identifies unserved energy (i.e., load that the system is unable to serve) or other constraint

violations (e.g., reserves shortages or hydro violations), the CEM can be refined to incorporate

additional constraints or requirements, which directly impacts the resulting build decisions.

3.2 Reliability- and Resource-Adequacy-Related Assumptions

3.2.1 Planning and Operation

We assume that planning is performed in a coordinated manner to minimize cost and ensure

resource adequacy and operational reliability across the entire Railbelt system. Practically

speaking, this does not require a single entity to plan the system but does require coordination

across the utilities—including likely joint planning of assets, particularly those generation assets

that provide energy to multiple utilities. This process could include joint ownership of plants,

shared PPAs, or any other policy mechanism that maximizes planning efficiency.

Likewise, we assume coordinated system operation (joint dispatch), meaning that the generators

and transmission assets are operated in a manner to produce the overall least systemwide cost,

while maintaining independent reliability in each of the utility zones. We do not include the costs

associated with full system coordination but do include an additional cost in the Reference and

RPS scenarios associated with scheduling and forecasting additional renewable resources (see

12

This model was used in the previous Railbelt study.

13

Denholm, P.; M. Schwarz, E. DeGeorge, S. Stout, and N. Wiltse. 2022. Renewable Portfolio Standard Assessment

for Alaska’s Railbelt. Golden, CO: National Renewable Energy Laboratory. NREL/TP-5700-81698.

14

Operating reserves represent generator capacity available to address variability and uncertainty in generation

supply and demand and include contingency, flexibility, and regulating reserves. Reserves can be held by partially

loaded generators (or offline generators, depending on the type of reserve) with sufficient ramp to respond in a given

time frame.

15

NREL often evaluates subhourly variability, but insufficient data were available to consider the impact of

increased subhourly variability in this study; instead, we used estimates for operating reserve requirements needed to

address ramp rate requirements within the hour.

9

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

Section 3.3.5). This study did not assume any specific regulatory approach that might achieve

this type of operation, and this does not require utilities to merge or otherwise lose independence

to ensure local reliability and rate setting.

We assume that each utility zone can be islanded and operated in isolation and maintain

resource adequacy. During islanded operation, the 80% RPS requirement is not enforced.

3.2.2 Resource Adequacy (Planning Reserve Margin) Assumptions

We require sufficient capacity to reliably serve load during all hours of the year, including times

of system stress, which are often peak-load or peak-net-load

16

conditions—of which the

magnitude and timing are uncertain. The total firm capacity requirement is typically defined as

expected peak load in each year plus a predetermined generation capacity margin (the planning

reserve margin) for reliability. Based on previous Railbelt utility studies, we maintain a 30%

planning reserve margin in each zone, meaning that installed dependable capacity must be at

least 30% higher than the expected peak demand in each year.

17

The capacity must be located

within the zone, so imports on the interties do not count toward the planning reserve margin.

Firm capacity differs from total nominal or nameplate capacity—it is the portion of nominal

capacity that is reliably available during times of system stress. We assume that all existing

thermal and hydropower plants are eligible to contribute to the planning reserve margin. The

ability of wind and solar resources to serve peak demand (capacity credit; see Appendix A) is

substantially lower than those of hydropower and thermal assets and described in the technology

discussions in Appendix C.

3.2.3 Operational Reliability Assumptions

We require operating reserve to ensure that there is sufficient capacity that can quickly vary

output to 1) address unexpected generator or transmission line outages; 2) respond to short-term

random variation in load, wind, and solar output; and 3) balance out longer-term (up to 1 hour)

uncertainty and forecast errors in net load, including ramping.

18

We require contingency

spinning reserves to address rapid failures of large plants or transmission lines (80 MW) and

regulating reserves (2% of load in Central and HEA and 5% in GVEA) to address rapid and

unpredictable variations in load. We also include additional operating reserves to address the

variability of wind and solar (see Section 3.3.2). Further description is provided in Appendix

B.7.

3.3 Addressing Wind and Solar Variability and Uncertainty

The variability and uncertainty of wind and solar can create changes in how the system is

planned and operated. These changes are sometimes considered in terms of an “integration cost,”

16

The concept of “net load” is commonly used in systems with large amounts of renewable resources and refers to

the normal load minus the contribution of wind and solar. This is important because it determines the amount of

hydropower, fossil, or other resources needed to ensure reliability.

17

See section 8.1 in the 2010 Alaska Railbelt Regional Integrated Resource Plan (RIRP) 2010.

https://www.akenergyauthority.org/Portals/0/Publications%20and%20Resources/2010.02.01%20Alaska%20Railbelt

%20Integrated%20Resource%20Plan%20(RIRP)%20Study.pdf?ver=2022-03-22-115635-150.

18

See Table B-6 for further discussion of treatment of operating reserves.

10

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.