ALASKA’S RENEWABLE

ENERGY FUTURE:

New Jobs, Aordable Energy

Developed for Regenerative Economies Working Group – Alaska Climate Alliance

FULL REPORT

[1]

Alaska’s Renewable Energy Future: New Jobs, Aordable Energy

ALASKA’S RENEWABLE ENERGY FUTURE:

New Jobs, Aordable Energy

KEY TAKEAWAYS:x

■ Alaska has a vast endowment of renewable energy resources

■ Renewable energy technology costs continue to decline, while local and global fossil fuel

costs continue to escalate

■ Renewable energy technologies are on track to aordably replace legacy fossil fuel energy

systems in the 2030-to-2050 time horizon

■ The development of Alaska’s vast renewable energy potential has the potential to generate

more than 103,554 jobs across Alaska – more than replacing the jobs lost as fossil fuels

become obsolete

■ With continued federal support, renewable hydrogen-based fuels have the potential to

replace fossil fuels in the marine and aviation sectors and form the basis of a new export

economy

Developed for: Alaska Climate Alliance – Regenerative Economies Working Group

Primary Authors

• Kay Brown, Pacific Environment

• Carly Wier, Native Movement

Prepared in collaboration with:

• Ben Boettger, Alaska Public Interest Research Group

• JackieArnaciarBoyer, Native Peoples Action

• Mark Foster, Mark A. Foster and Associates (MAFA)

• The Cadmus Group

Design

• Marianne Michalakis, designMind

Land Acknowledgement:

The authors and contributors (and readers, we hope!) of this report humbly and respectfully acknowledge that the land and

resources we are describing and analyzing are the ancestral and unceded territory of the Indigenous Peoples of Alaska.

We write this with deep gratitude to the Indigenous Peoples of Alaska for their continued care and stewardship of the

land on which we live, work and play. We acknowledge this not only in thanks to the Indigenous communities who have

held relationship with this land for generations but also in recognition of the historical and ongoing legacy of colonialism.

Additionally, we acknowledge this as a point of reflection for us all as we work towards dismantling colonial practices.

RELEASE DATE: March 21, 2022

[2]

Alaska’s Renewable Energy Future: New Jobs, Aordable Energy

Table of Contents

Executive Summary ...................................................................................................................................................4

Introduction ..................................................................................................................................................................7

Benefits of Accelerating the Transition to a Renewable Energy Future in Alaska by 2050 ............. 7

Alaska’s Energy Context ..........................................................................................................................................9

Introduction ...............................................................................................................................................................9

Alaska’s Energy Consumption .......................................................................................................................... 10

Renewables in Electricity Supply ...................................................................................................................... 12

Historic Context and Emerging Trends ........................................................................................................... 12

Declining Oil Industry ..................................................................................................................................... 12

Turnaround in Fossil Fuel Price Outlook in Alaska (2008) .................................................................. 14

Electric Power Sector ............................................................................................................................... 14

Alaska’s Unique Energy Infrastructure ...................................................................................................... 15

Employment by Major Energy Technology Application ....................................................................... 16

Employment in Electric Power Sector ........................................................................................................17

Alaska’s Shift Toward a Renewable Energy Future ..................................................................................... 18

State Renewable Energy Fund .................................................................................................................... 18

Federal $1.2 trillion Infrastructure Investment and Jobs Act ............................................................... 18

Utility Goals ....................................................................................................................................................... 18

Major Railbelt Utility Initiatives in Support of Renewable Development ......................................... 19

Utility Renewable / Energy Eciency / Building Electrification Initiatives ....................................... 19

Vast Alaska Renewable Energy Resource Opportunity .............................................................................20

Renewable Energy Technology Trends ........................................................................................................... 22

History – Rapid Reduction in Costs ................................................................................................................ 22

Onshore Wind Cost Trends .........................................................................................................................22

Oshore Wind Cost Trends ......................................................................................................................... 23

Battery Storage Cost Trends ....................................................................................................................... 24

Section summary .................................................................................................................................................. 24

Rising Cost of Fossil Fuels ................................................................................................................................... 25

Transportation Sector ......................................................................................................................................... 27

Section Summary ................................................................................................................................................. 27

Potential Paths for Renewables to Replace Fossil Fuels ........................................................................... 28

Emerging Opportunities for Decarbonization of Building and Transportation Sectors ................... 30

Building Electrification .................................................................................................................................. 30

Transportation Electrification ...................................................................................................................... 30

Green Hydrogen-Based Fuels .................................................................................................................... 31

Strategies to Accelerate the Transition to Clean Renewable Energy .................................................... 36

Conclusion ................................................................................................................................................................. 44

Endnotes .................................................................................................................................................................... 45

[3]

Alaska’s Renewable Energy Future: New Jobs, Aordable Energy

Table of Figures

Figure 1. Electric Utility Residential Rates (Ratio of selected Alaska Regions to US Weighted

Average), 2002-2020 ................................................................................................................................. 9

Figure 2. Alaska Energy Consumption Estimates by Energy Source (EIA, 2019) .....................................10

Figure 3. 2050 100% Renewable Energy Sankey Diagram ..............................................................................11

Figure 4. Alaska Energy Production & Alaska’s End-Use Energy Consumption

Comparisons, 1973-2020 .........................................................................................................................12

Figure 5. Alaska Oil & Gas Sector Average Monthly Employment (2014-2021) ........................................13

Figure 6. EIA Electric Power Sector Fossil Fuel Prices (Alaska/U.S. Price Ratio, 1970-2019) ................14

Figure 7. Alaska Electric Light & Power Residential Electric Rate Comparison –

selected Alaska Utilities (2020) ..............................................................................................................15

Figure 8. Alaska Energy Regions Map .................................................................................................................... 15

Figure 9. Alaska’s Employment by Major Energy Technology Application (2019 - 2020) .....................16

Figure 10. Alaska’s Electric Power Generation Employment (2019 – 2020) ................................................ 17

Figure 11. Alaska Renewable Energy Resource Map Compilation (2021) ....................................................21

Figure 12. Land based wind cost trajectories (NREL, 2020) ........................................................................... 22

Figure 13. Fixed bottom oshore wind cost trajectories (NREL, 2020) ........................................................23

Figure 14. Electric Power Sector Fossil Fuel Prices, Alaska to U.S. Price Ratio, 1970-2019 .................. 25

Figure 15. Cook Inlet Natural Gas Breakeven Costs for Incremental Supply ............................................ 26

Figure 16. Alaska Cook Inlet Natural Gas Prevailing Price of Utility Purchases:

History + Outlook with LNG Import Competition in 2031 & beyond ......................................... 26

Figure 17. Transportation Sector Fossil Fuels: Alaska to U.S. Price Ratio, 1970-2019 .............................. 37

Figure 18. Overall fuel-related cost components of hydrogen, ammonia and methanol .......................33

Figure 19. Geographies with combined zero-carbon resources of high capacity and low cost ..........34

Figure 20. Hydrogen demand and refueling infrastructure needed for transpacific

container ships under the full deployment scenario ......................................................................35

Figure 21. 80% Renewable Portfolio Standard (RPS) for Alaska Railbelt Electric Utilities

compared to Total Alaska Energy Consumption by Market Segment (2019 data) ...............39

[4]

Alaska’s Renewable Energy Future: New Jobs, Aordable Energy

Executive Summary

Alaska has a vast endowment of renewable energy resources that can be tapped in its transition

to a renewable energy future. Benefits of accelerating the energy transition in Alaska include

more jobs, lower energy prices, higher energy security and the potential for renewable resources

to support zero carbon hydrogen-based fuels for the aviation and maritime industries.

The state has already begun to develop its renewable energy resources and continues to support

renewable technology development for Alaska’s challenging environment. The scale of Alaska’s

vast undeveloped renewable energy resource endowment remains more than 14 times the total

U.S. energy consumption.

1

Alaska’s historically high and volatile fossil fuel-based energy costs have been moderated

by the successful development of renewable energy resources across the state, including:

• Bradley Lake & Battle Creek Diversion, Solomon Gulch, Terror Lake, Swan Lake,

Tyee Lake, and other recent hydro projects in both the Southeast and Southwest

• Fire Island, Eva Creek, Kotzebue, Kodiak & AVEC Wind

• GVEA & HEA Battery Energy Storage Systems

• GVEA Solar PV, MEA Solar PV by Independent Power Producers; with discussions

underway for a 20MW solar PV project in HEA territory

• Village scale solar PV projects in remote rural communities, e.g., Eagle, Hughes, Kaltag

• Juneau, Tok, Coman Cove, Craig, Gulkana, Elim, Thorne Bay, Haines, and Tanana

Biomass

• Chena Hot Springs Geothermal Heat and Electricity

Renewable energy technologies, including wind, solar, geothermal, and ocean and river

hydrokinetic, along with complementary energy storage technologies, are continuing to exhibit

declining costs which make them increasingly attractive as a primary energy source to substitute

for fossil fuels in the electric sector and to support the electrification of buildings and the

transformation of the transportation sector to electrification and renewable hydrogen-based fuels.

As local fossil fuel costs escalate across Alaska, from 2.5X higher in the Railbelt to as much as

4X higher in Rural Alaska (as compared to the U.S. average), renewable energy technologies are

increasingly attractive investments and are poised to aordably replace legacy fossil fuel energy

systems in the 2030-to-2050 time horizon while providing greater energy security, increased

energy resiliency especially in rural Alaska, and broad environmental, economic and health

benefits.

2

Independent studies have confirmed that the development of Alaska’s renewable energy

potential will generate thousands of jobs – at least comparable in magnitude to the fossil fuel jobs

that may be displaced by the transition to a clean renewable energy sector.

3

[5]

Alaska’s Renewable Energy Future: New Jobs, Aordable Energy

Based on adjusting a sample of independent studies for Alaska cost dierentials for renewable

resource, energy storage and zero carbon hydrogen/clean fuels infrastructure, we estimate that

by 2050, the transition to a 100% clean renewable energy future for Alaska would generate a

net increase of 67,216 jobs (103,554 additional renewable jobs minus 36,338 fossil fuel energy

related jobs lost).

4

In addition to developing renewable energy resources on the supply side, the electric sector has

opportunities to rebuild flagging electricity sales through building electrification and transformation

of the transportation sector to electric and green hydrogen-based fuels. The acceleration of the

transformation of the building heating and transportation sectors to clean renewable energy

will require a sustained federal, public, and private investment in science, technology, including

systems integrations.

Renewable hydrogen-based fuels have the potential to replace fossil fuels in the marine and

aviation sectors as renewable energy, renewable hydrogen production, storage, and hydrogen

fuel cell technologies continue to develop [see Potential Pathways for Renewables to Replace

Fossil Fuels, subsection Green Hydrogen-Based Fuels below].

Collaborative consultations with key stakeholders, including local communities, Tribes, residential

energy consumers, public and private sector energy consumers and producers (including

Alaska Native Corporations), and local utilities will be essential to ensuring long term support for

successful development of local renewable energy resources.

Key strategies for the state of Alaska to accelerate the transition to a clean, renewable energy

future include:

■ Undertake a comprehensive statewide strategic policy and planning eort, including

an explicit goal of transitioning to 100% clean renewable energy by 2050, to help focus

emerging integrated planning eorts. One potential planning mechanism is an Integrated

Resource Plan required by recent legislation establishing an Electric Reliability Organization

in the Alaskan Railbelt.

■ Enact legislation to require electric utilities to achieve 100% clean renewable energy by

2050 and to regularly measure and report progress toward that goal, including adoption of

reasonable Renewable Portfolio Standards, e.g., 80% by 2040.

5

■ Develop plans that ensure equity and aordability in clean energy, making energy transition

costs aordable for people across income scales, with programs like community solar and

on-bill financing.

■ Provide a vital round of seed funding and financing commensurate with the need to

accelerate the transition to 100% clean renewable energy by 2050.

6

o Extend the Alaska Renewable Energy Fund beyond its current sunset of 2023 and

fund it with a fresh round of $3.2 billion in “clean renewable energy” seed capital.

7

■ Encourage and support private and public sector entities that seek to develop and disclose

their environmental impacts under a credible, independent global environmental disclosure

system, e.g. CDP, formerly known as “Climate Disclosure Project.”

■ Seek Alaska Permanent Fund support for publication of environmental disclosures of its

investments to ensure portfolio investments are assessing and addressing climate risks.

8

[6]

Alaska’s Renewable Energy Future: New Jobs, Aordable Energy

■ Raise the net metering cap so utilities can enable electric customers who produce their own

electricity to receive a credit for the excess energy they transfer back to the utility and/or

change the net metering regulation so that credits generated during peak months can be

utilized in o-peak months, shifting to annual accounting of credits instead of monthly.

■ Require Regional Integrated Resource Plans include:

o Substantive opportunities for local collaboration/consultation;

o Consideration of future cost escalation associated with fossil fuel resources from

both direct and indirect costs, e.g. CO

2

equivalent emissions costs and other

environmental externalities;

9

o Explicitly require regional energy plans to include the overarching policy goal of

reaching 100% clean renewable energy for all energy needs by 2050 and include a

pathway to achieve it within their options for consideration.

■ Workforce Development:

o Incentivize industry-led training curriculum for the construction and operations of

renewable energy technologies.

o Incorporate renewable energy training curriculum into a state-certified

apprenticeship program.

o Encourage engagement of K-12 and University students in renewable energy

technology education.

To understand the history, current state, and future potential of a transition to a 100% clean,

renewable, and equitable energy future in Alaska by 2050, the authors and supporting

organizations engaged the Cadmus Group for a literature review and quantitative analysis of

existing resources and data to supplement the research and analysis developed by the working

group and its collaborators.

This report illustrates a vision for a clean renewable energy future in Alaska and the potential

benefits this increasingly urgent transition to an equitable new energy system could provide.

[7]

Alaska’s Renewable Energy Future: New Jobs, Aordable Energy

Introduction

This study looks at the potential for 100% clean renewable energy to replace fossil fuel

energy in Alaska by 2050 and its attendant benefits including more jobs, lower energy

prices, higher energy security and the potential for renewable resources to support the

equitable transition to hydrogen-based fuels for the aviation and maritime industries.

Benefits of Accelerating the Transition to a Renewable Energy

Future in Alaska by 2050

The benefits of transitioning to 100% clean renewables for all energy purposes (including

electric, building heating and transportation fuels) by 2050 include:

10

1. Creation of 67,500 more long-term, full time jobs in Alaska than lost

2. Eliminates 43 million tonnes CO

2equiv

per year in 2050 in Alaska

3. Reduces 2050 all-purpose, end-use energy requirements by roughly half

4. Reduces total annual energy, health and climate costs by 25%; from $23.2 billion to $17.3

billion per year

5. The substantial up-front investment costs, on the order of $128 billion over 30 years, can

be mitigated by federal and state co-investment.

a. Aggregate public co-investment on the order of 25% should be sucient to more

than buy down the net price of energy to be less than the superficial cash price of

the business as usual fossil fuel projection

b. The 25% public co-investment, which could be split between state and federal

consistent with the historic approach to federal highway funds, 1:9, would amount

to $3.2 billion for the State of Alaska

6. The net increase in annual investment and expenditure costs in a 100% clean renewable

energy transition by 2050 may be on the order of 0.91% of Alaska’s GDP in 2050.

11

7. Requires 0.14% of Alaska’s land for the renewable resource development

a. Including wind farms, solar arrays, geothermal power plants, electric and heat

storage infrastructure, transmission lines and substations

b. Amounts to roughly 600,000 acres which is roughly equal to the current total area

of wind farms in TX and OK

12

This report seeks to raise public awareness of positive clean renewable energy potential and

its many associated benefits so Alaskans can work together to accelerate the development of

robust renewable energy capacity, energy storage, and transmission systems that will build the

foundation for a reliable renewable energy grid system which can support:

■ Reliable electric service for local microgrid and grid interconnected communities,

■ Electrification of the building and transportation sectors, and

■ Development of clean renewable hydrogen-based transportation fuels to help sustain and

grow critical Alaska industries, including:

o Fisheries fleet and processing activities,

[8]

Alaska’s Renewable Energy Future: New Jobs, Aordable Energy

o Marine transportation, including refueling and transshipment, and

o Anchorage International Airport World Class Cargo Hub.

The Regenerative Economies Working Group of the Alaska Climate Alliance is working with a

broad coalition of entities and individuals with the goal of articulating and advancing an economic

vision for a prosperous, clean energy future for Alaska. The Alaska Climate Alliance is a group of

50+ organizations and more than 120 participants united by our desire to align Alaska’s climate

action community with Just Transition principles, addressing the climate crisis head-on at all levels

of society and shifting our state towards a joyful, interdependent and Indigenous-led future.

This report, Alaska’s Renewable Energy Future: New Jobs, Aordable Energy, showcases specific

renewable energy technologies that are ripe for development as well as the potential scale of

the renewable energy sector jobs, and recommends strategies to support Alaska’s transition to a

clean energy future.

The report is structured into the following sections:

Alaska’s Energy Context: This section details Alaska’s historic energy context, including

insights into how much energy the state consumes, how that energy has been generated,

and the jobs the energy industry has supported in the past.

Alaska’s Vast Renewable Energy Resource Endowment: Due to its unique geography,

Alaska has a vast endowment of diverse natural resources that can support a vibrant

renewable energy sector capable of scaling up to meet the state’s energy demand. The

renewable energy resources covered in this report are onshore and oshore wind, solar,

ocean and river hydrokinetic, geothermal, hydropower, biomass, and green hydrogen-

based fuels.

Renewable Energy Technology Trends: This section highlights the history and outlook for

declining costs of renewable energy and energy storage technologies that will enable an

aordable transition to a renewable energy future.

Rising Cost of Fossil Fuels: This section highlights the history and outlook for the rising

cost of fossil fuels that can be avoided by accelerating the transition to a renewable energy

future.

Potential Path for Renewables to Replace Fossil Fuels: This section highlights recent

research into potential pathways to 100% clean, renewable power across Alaska by 2050

and the benefits that can be achieved by accelerating the development of renewable

energy resources to replace fossil fuels.

Strategies to Accelerate the Renewable Energy Transition: This section describes

policy, planning, funding and financing, and workforce development initiatives aimed at

accelerating the transition to a renewable energy future.

Conclusion: This section describes the key takeaways and calls for action from the report.

[9]

Alaska’s Renewable Energy Future: New Jobs, Aordable Energy

Alaska’s Energy Context

Introduction

Alaska’s unique geography of widely dispersed remote communities and variable local energy

resources have contributed to a long history of high energy costs across the state, exemplified by

rural electricity residential rates as high as 7X the U.S. average in remote rural locations.

13

Over the decades, a wide variety of eorts to help mitigate the high cost of energy have been

undertaken across the state.

Beginning in the 1950s, the federal Alaska Power Administration built and operated hydroelectric

projects in Alaska in part to mitigate the high cost of energy in Alaska. These assets were

divested to local utilities over 1989-1991.

14

In the 1980s, the State of Alaska began to invest in hydro resource development, including Bradley

Lake (Railbelt) and the Four Dam Pool (Tyee Lake, Swam Lake, Solomon Gulch, Terror Lake).

In the 2008 oil price spike era, the State of Alaska enacted and funded a renewable energy fund

administered by the Alaska Energy Authority to help mitigate the high cost of fossil fuels.

15

More

than 95 operating projects have been built, collectively saving more than 30 million gallons of

diesel each year.

The net results of those investments have helped reduce residential electric rates across Alaska

over the past 20 years – especially across rural and Southeast communities [see Electric Utility

Residential Rates Figure 1].

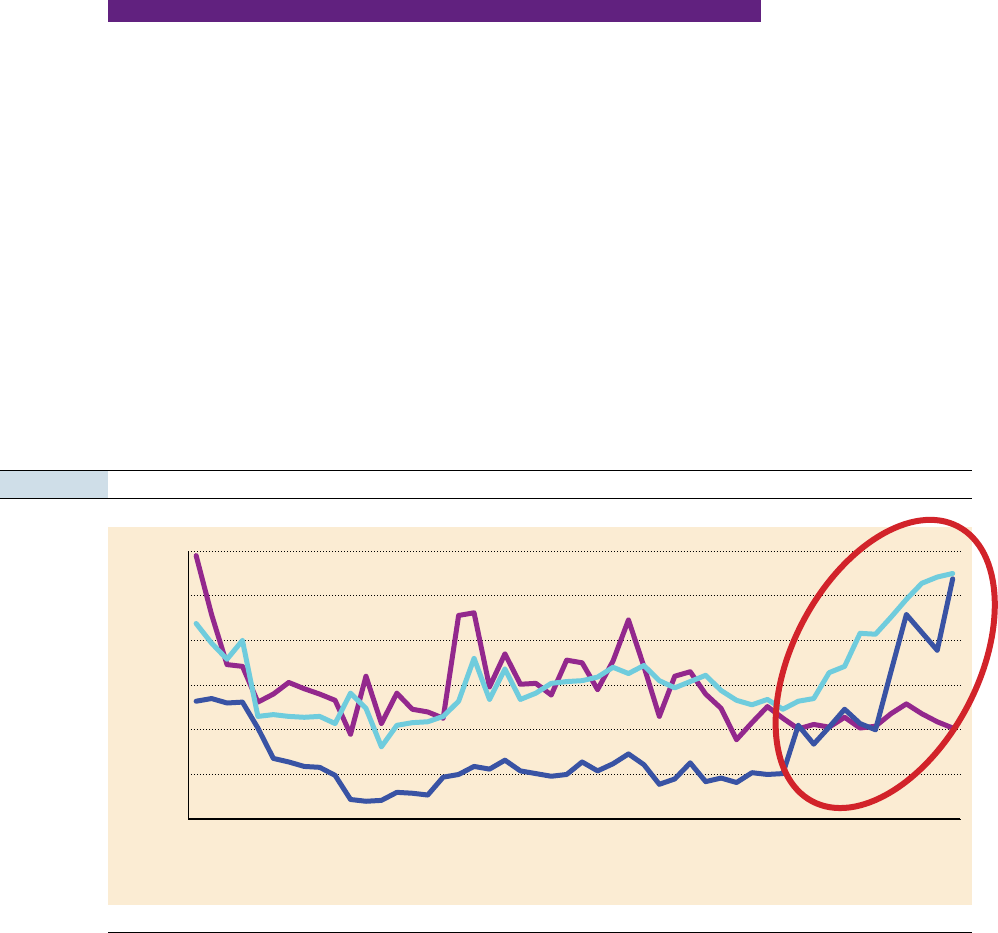

Electric Utility Residential Rates (Ratio of selected Alaska Regions to US Weighted Average), 2002-2020

However, residential electric rates

across most of Alaska remain extremely

expensive compared to the U.S. and the

upward trend in residential electric rates

in the Railbelt continues to present a

challenge to household budgets. The

renewable investments in the Railbelt,

e.g., Bradley Lake Hydro, Fire Island &

Eva Creek Wind, and State of Alaska

direct subsidized support of natural gas

exploration and development in the Cook

Inlet have not been enough to mitigate

the rise in residential electric rates driven

by the increase in natural gas supply

prices in the Cook Inlet [see Electric

Utility Residential Rates Figure 1].

FIGURE 1

0

1

2

3

4

5

6

2020

2002

Electric Utility Residential Rates

[Alaska Utility-Region :: US Wtd Avg Ratio]

■ Rural Diesel => Diesel + Wind

■ Railbelt => NG

■ Kodiak => Hydro+Wind

■ Southeast => Hydro

Source: EIA Electric sales, revenue and average price, October 7, 2021, 2020, data

tables, Table 6, with previous editions available in pdf at: https://www.eia.gov/electricity/

sales_revenue_price

[10]

Alaska’s Renewable Energy Future: New Jobs, Aordable Energy

The balance of this section on Alaska’s Energy Context provides an overview of:

■ Consumption

■ Production - Oil & Gas

o Oil Production Employment

■ Fossil Fuel Price Outlook

o Electric Power Sector

■ Alaska’s Unique Dispersed Geography & Associated Energy Infrastructure Adaptations

o Energy Infrastructure Employment

■ Renewable history & outlook

o 1980s

o 2008 Oil Price Surge

o Federal Infrastructure Act Opportunities

■ Utility Renewables Goals & Activities

Alaska’s Energy Consumption

Alaska Energy Consumption Estimates by Energy Source (EIA, 2019)

Source: EIA State Energy Data System, Alaska Energy Consumption, 2019

In 2019, Alaska consumed an estimated 616 trillion btus of energy. Roughly 57% of that total

consumption was supplied by natural gas. Renewable energy resources generated an estimated

24 trillion btus or 4% of the total state energy supply.

Alaska North Slope and Cook Inlet Oil & Gas exploration, development and processing use almost

80% of the natural gas consumed in Alaska for those industrial processes.

FIGURE 2

050 100 150 200 250300 350 400

Other Renewables

Biomass

Hydroelectric Power

Nuclear Electric Power

Other Petroleum

Residual Fuel

HGL

Jet Fuel

Distillate Fuel Oil

Motor Gasoline excl. Ethanol

Natural Gas

Coal

Trillion btus

■ Domestic Energy Market

■ Fossil Fuel Industrial Processing + International Air Cargo Hub

[11]

Alaska’s Renewable Energy Future: New Jobs, Aordable Energy

In a 100% clean, renewable energy future, oil & gas exploration and development is expected

to essentially fade away, leaving behind a very modest residual for non-energy end-use, e.g.,

asphalt, and be replaced by a robust mix of renewable energy resources with a markedly

diminished energy footprint for their exploration, development, processing and production of end-

use energy for electricity, heating/cooling and green hydrogen-based fuels.

16

Thus, before taking into consideration population growth and other changes in the energy mix

and production processes between now and 2050, we expect Alaska Energy Consumption to be

roughly 280 trillion btus lower in a 100% clean renewable energy future.

The next largest energy resource consumed in Alaska after natural gas is jet fuel.

The Anchorage International Airport moved from the sixth to the fourth largest air cargo hub in

the world in 2021. In 2019 (most recent EIA State Data), jet fuel consumption at the Anchorage

International Airport was on the order of 17.5 million barrels of jet fuel in 2019. Jet fuel at the

Anchorage International Airport is a substantial fossil fuel energy demand center in Alaska that

merits special attention given its prominence in the Alaska energy picture; 90 trillion btus are

associated with the international passenger and air cargo flights.

17

Distillate fuel oil, the third largest energy resource consumed in Alaska, is widely used in truck,

rail, and marine transport, and rural Alaska electric generation.

In the synthesis of the reports describing costs and benefits from 100% clean renewables in 2050,

MAFA included the estimated cost of transitioning to 100% renewables and renewable hydrogen

production and further downstream processing into liquid fuels for the transport sector, including

aviation jet fuels, marine fuels. For an illustrative example of the energy flows under a 100%

renewable scenario, please see the figure below from the Williams (2020), supplemental materials.

2050 100% Renewable Energy Sankey Diagram (Exajoules)

Source: J.H. Williams et al, Carbon-Neutral Pathways for the United States, AGU Advances Research Article, 10.1029/2020AV000284, Supplemental Materials,

Figure S4. Sankey diagram by scenario, p. 12

FIGURE 3

[12]

Alaska’s Renewable Energy Future: New Jobs, Aordable Energy

Renewables in Electricity Supply

Alaska’s historically high and volatile fossil fuel-based energy costs have been moderated by

utility and independent power producer investments in renewable energy resources across the

state. Renewables have grown to supply 30% of the total electrical demand in Alaska. Renewable

energy projects include:

• Bradley Lake & Brattle Creek, Four Dam Pool & other Southeast Hydro

• Fire Island, Eva Creek, Kotzebue, Kodiak & Alaska Village Electric Cooperative (AVEC) Wind

• GVEA Battery Energy Storage System (BESS)

• MEA Solar PV

• Juneau, Tok, Coman Cove, Craig, Gulkana, Elim, Thorne Bay, Haines & Tanana Biomass

• Chena Hot Springs Geothermal

• Hydrokinetic power in Igiugig

Historic Context and Emerging Trends

To understand emerging trends and opportunities in the context of a thirty-year outlook, it may be

useful to look back at the history that brought us to this point, including a quick look back to the

1970s, before the construction and completion of the Trans Alaska Pipeline System (TAPS), to see

the impact of that development on the energy sector across Alaska and discern the long-term

decline of the oil and gas sector.

DECLINING OIL INDUSTRYx

Alaska Energy Production & Alaska’s End-Use Energy Consumption Comparisons, 1973-2020

Source: EIA Crude Oil Production, Natural Gas Marketed Production, Alaska, 1973-2020

FIGURE 4

0

500

1000

1500

2000

2500

3000

3500

4000

4500

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

2017

2019

–

–

–

–

–

–

–

–

–

–

–

–

–

–

–

–

–

–

–

–

–

–

–

–

Trillion BTUs per year

■ Natural Gas Marketed ■ Crude Oil Field Production ■ Total Alaska End-Use Consumption

[13]

Alaska’s Renewable Energy Future: New Jobs, Aordable Energy

Alaska’s energy production history took a quantum leap in 1977 with the completion and operation

of the Trans-Alaska Pipeline Systems (TAPS) which enabled Alaska North Slope crude oil production.

After peaking at slightly over 4200 trillion btus per year (2 million barrels of oil per day), crude oil

production has declined rapidly through 2010 (5.4% per year), with the decline rate moderating to

2.6% per year since 2010.

Natural gas marketed production (approx. 80% of which supplies energy for the oil & gas industry

exploration, development and production activities), has been declining at 2.4% per year.

Alaska Oil & Gas Sector Average Monthly Employment (2014-2021)

More recently, while the

rate of decline of oil & gas

production has moderated,

oil & gas sector employment

has been falling rapidly – the

average annual employment

decline has been 11% per

year since 2014. This includes

all those who receive

compensation as employees,

which typically include oil &

gas companies as well as the

oil & gas industry contractors

who employee people. It does

not include sole-proprietors.

18

FIGURE 5

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

202120202019201820172016201520142013201220112010

Source: Alaska Department of Labor Workforce Development, Research Analysis Section, Alaska

Employment & Wages, 2010-2021

[14]

Alaska’s Renewable Energy Future: New Jobs, Aordable Energy

TURNAROUND IN FOSSIL FUEL PRICE OUTLOOK IN ALASKA 2008x

The available Energy Information Administration (EIA) State Energy Data (1970-2019) allow us to view

the big changes in fossil fuel price regimes in Alaska and consider the potential for real continuing

escalation in the price of fossil fuels in the future. This report highlights observations from the electric

power, residential, and transportation sectors especially as they pertain to the trends and outlook for

fossil fuel prices in Alaska after 2008 and how those trends inform the energy outlook to 2050.

Electric Power Sector

Following the OPEC oil embargo in 1973 and concurrent with the preparation for and construction

of the Trans-Alaska Pipeline System (1974-1977), the price of fossil fuels (coal, natural gas, distillate

fuels) dropped from historic patterns with energy as high as 2 to 3 times national norms into a new

price regime marked by low natural gas prices from the Cook Inlet (around 50% of U.S. norms) and

coal and distillate fuels in the range of 20% to 50% above U.S. norms – with volatility in between

– for the 34-year period from 1974 to 2008. See Figure 6. EIA State Energy Data: Electric Power

Sector Fossil Fuel Prices (Alaska/U.S. Price Ratio, 1970-2019) below.

EIA Electric Power Sector Fossil Fuel Prices (Alaska/U.S. Price Ratio, 1970-2019)

Source: EIA State Energy Data

In the period of fossil fuel price escalation in 2002-2008, natural gas price ratios stayed flat while

coal and distillate fuels moved toward parity with the U.S., i.e., Alaska prices rose slower than U.S.

Following the oil price spike in 2008, a new price regime emerged where coal and natural gas

prices rose in Alaska while declining in the U.S. The Alaska Electric Power Sector was paying over

2.6X as much for coal and natural gas compared to the U.S. in 2019.

In a June 2021 presentation to the City and Borough of Juneau Assembly, Alaska Electric Light

& Power, whose baseload is served 100% by hydroelectric power, highlighted the benefits of

its long-standing strategic investments in hydroelectric power compared to the natural gas

dependent Railbelt utilities. AEL&P residential rates were 12.5c/kWh while Homer Electric

Association rates were 28.7c/kWh – a stark reflection of the rapid price escalation in natural gas

prices for the Railbelt electric utilities.

19

FIGURE 6

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Alaska / US Price Ratio

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

–

–

–

–

–

–

–

–

–

–

–

–

–

–

–

–

–

–

–

–

–

–

–

–

–

■ Natural Gas ■ Coal ■ Distillate Fuels

[15]

Alaska’s Renewable Energy Future: New Jobs, Aordable Energy

Alaska Electric Light & Power Residential Electric Rate Comparison – selected Alaska Utilities (2020)

ALASKA’S UNIQUE ENERGY INFRASTRUCTUREx

Alaska Energy Regions Map

Source: Alaska Energy Authority

FIGURE 7

0

5

10

15

20

25

30

AEL&PNational Avg.AnchorageWasillaFairbanksHomer

Cost in ¢/kWh

28.73

25.13

21.56

21.2

15.2

12.52

Source: AEL&P compilation from Table 5.3 of Electric Power Monthly with Data for December 2020 published

by the U.S. Energy Inforamtion Administration in February 2021

Note: AEL&P’s rates remain the lowest among

the large, regulated utilities in Alaska. Our

rates are also comparable to the national

average, which is due in large part to our

ability to sell surplus energy to interruptible

customers.

FIGURE 8

North Slope

Northwest

Arctic

Bering Straits

Yukon-Koyukuk Upper Tanana

Railbelt

Lower Yukon Kuskokwim

Copper River

Chugach

Bristol Bay

Southeast

Kodiak

Aleutians

[16]

Alaska’s Renewable Energy Future: New Jobs, Aordable Energy

It is also useful to note Alaska’s unique energy supply infrastructure which has evolved around the

state’s vast and diverse geography. The Railbelt, which is interconnected by transmission facilities,

stretches from the Interior down to the Kenai Peninsula and represents roughly 79% of the state’s

electric utility generation.

Alaska also has over 150 individual microgrids,

20

an estimated 12% of the planet’s microgrid

infrastructure. Found primarily in remote, rural Alaskan communities, microgrids can be more cost-

eective and often more ecient in integrating multiple power sources compared to traditional

large-scale energy grids.

21

Interestingly, key regional hub communities, including Kotzebue in the Northwest Arctic, Kodiak,

as well as several communities across Southeast Alaska have been leaders in developing their

local renewable resources. Many smaller rural community microgrids are powered by diesel

generators, which often create challenges in transporting diesel and contribute to high electricity

costs for remote communities.

22

Alaska’s microgrid infrastructure poses both an opportunity

and a challenge for the transition to renewable energy and remains a key consideration in the

development and implementation of the strategies and approaches detailed in this report.

EMPLOYMENT BY MAJOR ENERGY TECHNOLOGY APPLICATIONx

Alaska has a high concentration of workers employed in the energy sector, with 21,673 traditional

energy workers statewide as of 2019, equating to 6.4% of total state employment.

23

The number

of traditional energy workers statewide fell to 18,945 in 2020, led by a sharp downturn in the fuels

sector. However, given reductions in total employment in 2020, traditional energy workers in

Alaska still made up a higher proportion of the total state employment in 2020, at 8.3%.

24

Jobs figures for both 2019 and 2020 are presented in this section. The 2020 jobs numbers provide

the most up-to-date information, while 2019 jobs numbers are provided because that was the year for

which the most updated energy consumption and supply data were available. In addition, 2020 figures

may have been impacted by the COVID-19 pandemic. Examining both years allows for presentation

of a more complete picture. A breakdown of energy employment in the state is shown in Figure 9.

Alaska’s Employment by Major Energy Technology Application (2019 - 2020)

Source: U.S. Department of Energy. 2020. “Alaska Energy and Employment – 2020.”, Source: U.S. Department of Energy. 2021. Energy Employment by State: 2021.

FIGURE 9

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

Motor VehiclesEnergy EciencyTransmission,

Distribution and

Storage

FuelsElectric Power

Generation

1,450 1,373

14,052

11,474

6,172 6,098

4,701

3,974

2,303 2,084

Lorem ipsum

■ 2019 ■ 2020

[17]

Alaska’s Renewable Energy Future: New Jobs, Aordable Energy

As of the 2021 Energy and Employment Report, the fuels industry employs the largest proportion

of energy workers in Alaska, with petroleum (7,036), natural gas (3,682), and other fossil fuels (498)

making up the largest segments of employment. Of these jobs, 8,058 were related to mining and

extraction of these fossil fuel resources.

xEMPLOYMENT IN ELECTRIC POWER SECTORx

Of the 1,373 Alaskan workers employed by the electric power generation industry in 2020,

traditional fossil fuel generation makes up the largest segment of employment, with 582 jobs,

followed by traditional hydroelectric generation at 405 jobs,

25

as shown in Figure 10.

Alaska’s Electric Power Generation Employment (2019 – 2020)

Source: U.S. Department of Energy. 2020. “Alaska Energy and Employment – 2020.” Source: U.S. Department of Energy. 2021. Energy Employment by State: 2021.

FIGURE 10

0

100

200

300

400

500

Other

Generations

NuclearOil & Other

Fossil Fuels

CoalNatural GasTraditional

Hydro

WindSolar

92 83

61 63

439

405

368

339

128

113

139

130

213

231

99

■ 2019 ■ 2020

[18]

Alaska’s Renewable Energy Future: New Jobs, Aordable Energy

Alaska’s Shift Toward a Renewable Energy Future

Though Alaska’s energy sector has historically been dominated by fossil fuels, the state has been

transitioning toward a renewable energy future.

The most recent escalation in fossil fuel prices (2008-2019) combined with increased appreciation

for the need for a transition to a clean renewable energy future has sparked renewed eorts

among Alaska electric utilities.

State and federal legislation has been passed and funding allocated to advance Alaska’s renewable

energy sector.

STATE RENEWABLE ENERGY FUNDx

In 2008, the Alaska State Legislature established the Renewable Energy Fund, a grant program

administered by the Alaska Energy Authority (AEA).

26

Between 2008 and 2015, this program was

responsible for Alaska’s largest public investment into renewable energy and eciency projects,

with wind and hydroelectric receiving majority of the funding. It is estimated that the program saved

$74 million in diesel costs across the state.

27

As of December 2020, the program has $6.5 million

left and is scheduled to sunset in 2023.

28

In 2010, Alaska set a nonbinding goal of generating 50%

of the state’s electricity from renewable and alternative energy sources by 2025.

29

FEDERAL $1.2 TRILLION INFRASTRUCTURE INVESTMENT AND JOBS ACTx

At the federal level, a recently enacted $1.2 trillion Infrastructure Investment and Jobs Act has the

potential to benefit a variety of sectors in Alaska, including, but not limited to, grid reliability and

resiliency upgrades, smart grid matching grants, renewable energy demonstration projects, energy

eciency and weatherization, energy storage, hydrogen, hydroelectric production incentives,

hydropower, electric vehicle (EV) charging stations, and electric and hybrid school buses.

30,31,32

These funds have renewed interest in renewable energy projects across the state and sparked an

interest in leveraging the new federal resources to continue a shift toward renewable sources.

UTILITY GOALSx

Many utilities in Alaska have also set their own goals related to generating electricity from renewable

sources and carbon reduction. Key examples from the Railbelt include the following:

■ In January 2021, Homer Electric Association (HEA) set a goal of sourcing 50% of its energy

demand from renewable sources by 2025.

33

Since declaring that goal, HEA created a

Strategic Services division to lead renewable energy projects, environmental compliance,

and regulatory aairs.

34

■ Golden Valley Electric Association (GVEA) adopted a goal to reduce its carbon output

by 26% by 2030, and renewable energy was identified as one way for GVEA to achieve

this goal. In 2013, renewable energy was already supplying 20% of GVEA’s system peak

load through energy conservation, hydroelectric, customer small-scale renewable energy

projects, and the Eva Creek Wind Farm.

35

The GVEA Board of Directors faces a mandated

decision by December 2022 whether to decommission or refurbish the Healy 1 coal plant

[19]

Alaska’s Renewable Energy Future: New Jobs, Aordable Energy

that must be implemented by 2024. Fairbanks has some of the worst air pollution in the

nation, high emission rates of carbon dioxide and other greenhouse gasses, and lack of

integration of aordable, clean energy.

■ Chugach Electric Association released a request for proposals in October 2021 to source

renewable energy projects that will contribute to its goal of adding 100,000 megawatt hours

(MWh) per year of renewable energy by 2025.

36

■ In response to member support, in April 2021 Matanuska Electric Association (MEA) adopted

a carbon reduction goal of 28% from 2012 levels by 2030. To achieve this goal, MEA has

prioritized sourcing energy from renewable sources, such as hydropower and member-

generated solar, among other initiatives to reduce its carbon footprint.

37

MAJOR RAILBELT UTILITY INITIATIVES IN SUPPORT OF RENEWABLE DEVELOPMENT

In 2021, HEA installed a large 46.5 MW (up to 93 MWh) Battery Energy Storage System (BESS) in

preparation for developing alternatives to the high and escalating cost of natural gas, enabling the

integration of non-firm energy sources, e.g., 20MW solar project. The battery project is expected

to cost $40 million.

38

UTILITY RENEWABLE / ENERGY EFFICIENCY / BUILDING ELECTRIFICATION INITIATIVESx

A few utilities in Alaska have initiatives in place to incentivize electrification of building heating and

vehicles.

AEL&P in Juneau, which is served primarily by hydropower, has two options which allow

customers to charge their EV during o-peak hours at a reduced rate and oer charging

equipment for rent.

39

AP&T, whose service territory includes Prince of Wales Island in Southeast Alaska, which is served

primarily by hydropower, has incentive programs to encourage the installation of heat pumps for

building heat and the purchase of electric vehicles.

40

Kodiak Electric Association, which is served primarily by wind and hydro with two flywheels and

a battery energy storage system, has an incentive program to encourage customers to switch to

electric heating for both space heating and hot water heaters.

41

[20]

Alaska’s Renewable Energy Future: New Jobs, Aordable Energy

Vast Alaska Renewable Energy

Resource Opportunity

SEVERAL STUDIES OVER THE PAST DECADE HAVE DOCUMENTED ALASKA’S VAST

RENEWABLE ENERGY RESOURCE POTENTIAL.

Renewable Energy in Alaska, WH Pacific, Inc, National Renewable Energy Lab (NREL), March 2013,

found:

■ Alaska is uniquely endowed with a full range of renewable energy opportunities, including

extensive and diverse biomass, hydropower that ranges from run-of-river and low-impact

high-head to traditional massive dams; wind energy that ranges from micro, wind-hybrid

turbines in small coastal villages to large wind farms [coastal + mountain range funnels]; world

class tides; and huge geothermal potential on the northern edge of the Pacific Rim of Fire.

■ The Levelized Cost of Electricity (LCOE)

42

from many renewable energy projects in Alaska,

including energy eciency initiatives, were competitive with local diesel fuel alternatives in

the short term (2010-2020) and looked increasingly competitive with other fossil fuel

alternatives (coal and natural gas) in the longer term (2020-2030) as natural gas prices were

forecast to increase from below the U.S. market average to well above and increased

regulation of coal was expected to add both capital and operating costs.

More recent studies have continued to document a large renewable energy resource base in Alaska:

■ Onshore Wind = 37,753 TWh/yr (2.48 times Texas) and 6726 GW potential nameplate

capacity, 2.4 times Texas, the next largest onshore wind potential state

43

■ Oshore Wind = 12,087 TWh/year, more than 2000 times the statewide energy consumption

in Alaska and more than 3 times the total U.S. energy consumption, a net oshore wind

energy potential that is 68% higher than all other states combined

44

■ Onshore + Oshore Wind Potential = 49,840TWh/yr; more than 14 X the total U.S. energy

consumption (EIA US Energy Consumption, 2020)

■ Hydroelectric = 46.36 GW undeveloped potential of which 4.723 GW is feasible potential

45

■ Geothermal = 2.4 GW potential

46

■ Solar PV = the solar PV resource is comparable to Germany, which has a cumulative

installed solar PV capacity of >55 GW

47

■ Tidal Power = Technical Power Potential of U.S. Marine Resources in Alaska = 1,100 TWh/

year, 27% of the total U.S. electricity generation

48

, of which Cook Inlet East-West Foreland

Transect = 46MW, 400 GWh/year

49

[21]

Alaska’s Renewable Energy Future: New Jobs, Aordable Energy

Alaska Renewable Energy Resource Map Compilation (2021)

FIGURE 11

Wind Speed

Taiping Wang, Zhaoqing Yang, A Tidal Hydrodynamic Model for Cook Inlet, Alaska, to Support Tidal

Resource Characterization, Pacific Northwest National Laboratory, 4 April 2020, Journal of Marine

Science and Engineering, 2020, 8(4), 254, Figure 12 Tidal Power Distribution near the Foreland Region

Tidal Hydrodynamic Model for Cook Inlet

Alaska Hydropower Existing and Feasible NSD Sites

Wind Speed

Joe Batir, David D. Blackwell,

Geothermal Lab, Southern

Methodist University,

TX, Alaska Figure 5:

Geothermal Potential, Heat

Flow and temperature-depth

curves throughout Alaska:

finding regions for future

geothermal exploration,

June 2016

Geothermal Potential

Billy J. Roberts, NREL, Solar Resource Comparison of Alaska and Germany, Figure 1, Solar Energy

Prospecting in Remote Alaska, Paul Schwabe, NREL, February 2016

Solar Energy Prospecting

[22]

Alaska’s Renewable Energy Future: New Jobs, Aordable Energy

Renewable Energy Technology Trends

History – Rapid Reduction in Costs

xONSHORE WIND COST TRENDSx

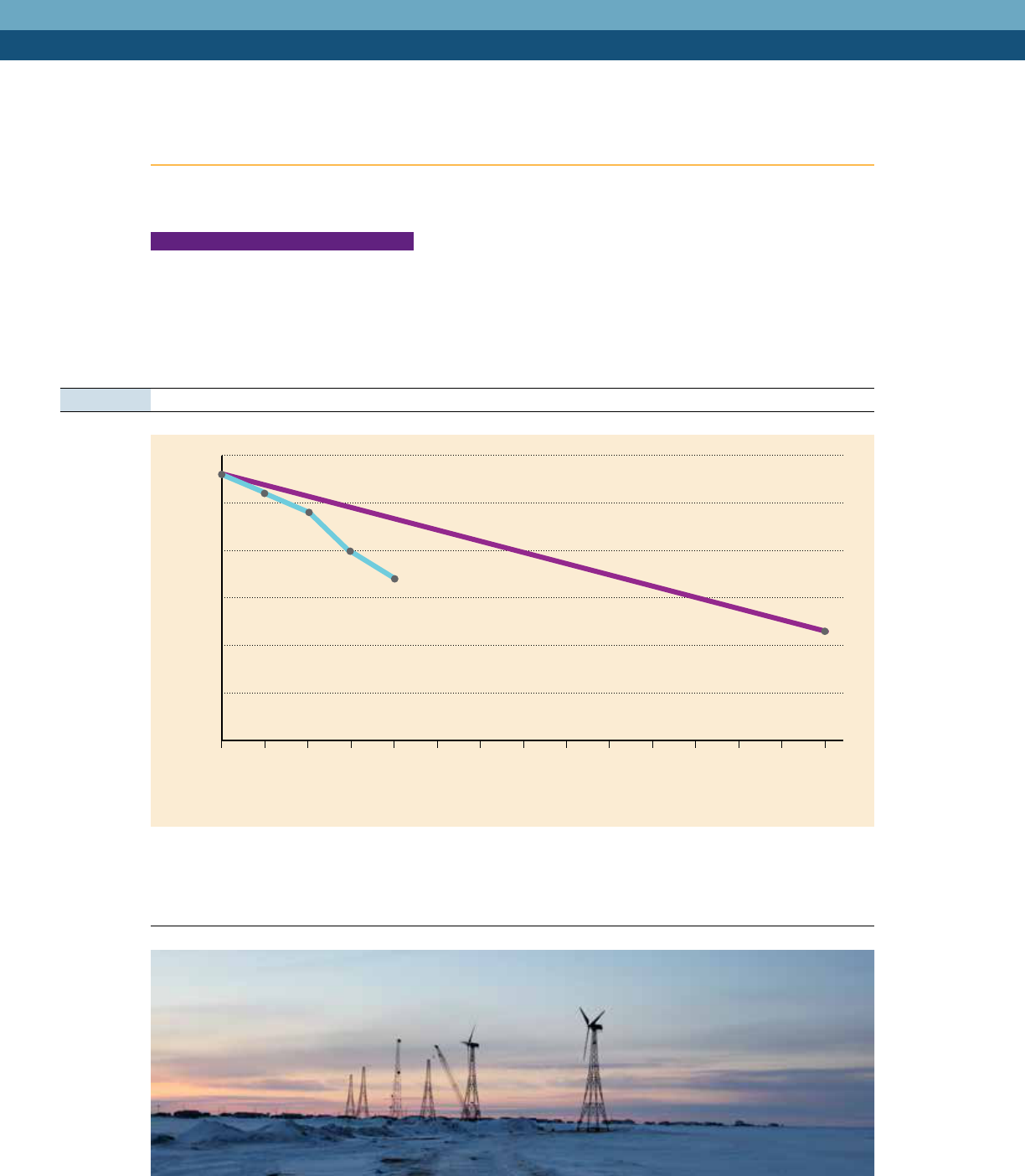

As illustrated in NREL’s 2019 Cost of Wind Energy Review (December 2020), Figure 12: Land-

based wind GPRA cost trajectories for LCOE (in 2015 USD), the actual onshore wind levelized

cost of energy (LCOE) from 2016 to 2020 has declined from $56/MWh to $34/MWh in real $ terms

(-39%) which is considerably faster than the previously projected cost decline trajectory.

Land Based Wind Cost Trajectories (NREL, 2020)

Source: NREL 2019 Cost of Wind Energy Review (December 2020)

Note: The drop in LCOE between 2019 and 2020 is largely because of updates made to the financing assumptions. Prior to the “2018 Cost of Wind Energy Review,”

WETO reported land-based financing using a constant and conservative FCR. The land-based FCR is updated in 2020 to maintain reporting consistency between

land-based wind and oshore wind technologies. Land-based-wind cost of capital data collected by Lawrence Berkeley National Laboratory (Wiser and Bolinger

2020) gives a basis for WACC assumptions for the representative wind project in 2019 and results in a nominal WACC of 6.32%. A sensitivity analysis using the

finance assumptions in last year’s cost report is captured in Appendix A.

FIGURE 12

0

10

20

30

40

50

60

203020292028202720262025202420232022202120202019201820172016

LCDE (2015$/MWh)

56

52

48

40

34

23

■ Actuals ■ GPRA Trajectory

[23]

Alaska’s Renewable Energy Future: New Jobs, Aordable Energy

xOFFSHORE WIND COST TRENDSx

As illustrated in NREL’s 2019 Cost of Wind Energy Review (December 2020), Figure 13: Fixed-

bottom wind GPRA cost trajectories for LCOE, the actual oshore wind levelized cost of energy

(LCOE) declined from $191/MWh to $83/MWh (2016-2020) in real $ terms (-56%). And the cost is

projected to continue to decline toward $51/MWh (2018$).

Fixed Bottom Oshore Wind Cost Trajectories (NREL, 2020)

FIGURE 13

203020292028202720262025202420232022202120202019201820172016

0

20

40

60

80

100

120

140

160

180

200

LCDE (2018$/MWh)

191

180

127

89

83

51

2019 rebaseline analysis

for GPRA reporting

GPRA Projection from rebaseline analyisis

Historical data

for reference

Source: Extract from NREL 2019 Cost of Wind Energy Review (December 2020)

■ Actuals ■ GPRA Trajectory

[24]

Alaska’s Renewable Energy Future: New Jobs, Aordable Energy

xBATTERY STORAGE COST TRENDSx

Electric power markets in the United States are undergoing significant structural change that

are projected to result in the installation of the ability of large-scale battery storage to contribute

10,000 megawatts to the grid between 2021 and 2023 – 10 times the capacity in 2019.

50

Average battery energy storage costs declined from $2012/kWh to $589/kWh from 2015-2019, an

average rate of decline of 27% per year.

51

The EIA Update on Market Trends also reported that,

“Although Alaska and Hawaii represent a significant share of current U.S. battery storage capacity,

their utilization patterns are unique in that batteries need to provide a wider range of additional

services and engineering support than is commonly used in the Lower 48 states.”

52

NREL’s most recent comprehensive cost projections for utility-scale battery storage (2020) anticipate

4-hour battery costs will continue to fall, reaching $208/kWh by 2030 and $156/kWh by 2050.

53

Section summary

Renewable energy costs, including battery storage and the integration of intermittent renewables

into an electric grid, continue to decline. GVEA and HEA leadership in investing in battery storage

resources is to be commended. Additional investments in battery storage should enable the

development of additional intermittent renewable energy resources as well as support additional

variability in demand from the electrification of building and transportation sectors. Centralized

and distributed storage are critical components needed to cost eectively integrate variable

renewable energy resources – around the world, in the U.S. and in Alaska.

[25]

Alaska’s Renewable Energy Future: New Jobs, Aordable Energy

Rising Cost of Fossil Fuels

Against the backdrop of the rapid decline in the cost of renewables and projected future cost

reductions, the electric power sector in Alaska has been experiencing an unusually rapid increase

in the cost of fossil fuels since 2008.

Electric Power Sector Fossil Fuel Prices, Alaska to U.S. Price Ratio, 1970-2019

Source: EIA State Energy Data

Alaska electric sector price premium for coal and natural gas has been escalating at an unusually

high rate since 2008. A State of Alaska Division of Oil and Gas Cook Inlet Natural Gas Availability

study in 2018 projected the costs for Cook Inlet natural gas supply are poised to continue

escalating rapidly.

FIGURE 14

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Alaska / US Price Ratio

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

–

–

–

–

–

–

–

–

–

–

–

–

–

–

–

–

–

–

–

–

–

–

–

–

–

■ Natural Gas ■ Coal ■ Distillate Fuels

[26]

Alaska’s Renewable Energy Future: New Jobs, Aordable Energy

Cook Inlet Natural Gas Breakeven Costs for Incremental Supply

Source: State of Alaska Division of Oil and Gas Cook Inlet Natural Gas Availability study (2018)

Extending the State’s analysis, natural gas price escalation appears likely to continue until LNG

imports become competitive.

Alaska Cook Inlet Natural Gas Prevailing Price of Utility Purchases: History + Outlook with LNG Import

Competition in 2031 & beyond

As Cook Inlet natural gas

prices rise from $8/Mcf

toward a projected $19/Mcf

over the next decade, the

levelized cost of electricity

from natural gas is slated to

increase toward $136/MWh,

rising well above the cost

of competitive renewable

alternatives.

54

FIGURE 15

0

2

4

6

8

10

12

14

16

18

2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

(Real 2016 $/Mcf)

10% Hurdle Rate (real) 15% Hurdle Rate (real) 20% Hurdle Rate (real)

Breakeven Price for Incremental Supply

FIGURE 16

0

5

10

15

20

25

2010

–

2012

–

2014

–

2016

–

2018

–

2020

–

2022

–

2024

–

2026

–

2028

–

2030

–

2032

–

2034

–

2036

–

2038

–

2040

–

2042

–

2044

–

2046

–

2048

–

2050

–

Nominal $ per Mcf

[27]

Alaska’s Renewable Energy Future: New Jobs, Aordable Energy

Transportation Sector

Transportation Sector Fossil Fuels: Alaska to U.S. Price Ratio, 1970-2019

From 1970-2008, the price

premium for Alaska “retail”

transportation fuels (diesel,

motor gasoline) hovered

around 5 to 15%.

From 2008-2019, the price

premium for Alaska motor

gasoline rose to over 40%

above the U.S., the price

premium for diesel fuel

rose to 12% above the U.S.

Source: EIA State Energy Data

Compared to the continental U.S. (aka Lower 48), Alaska motor gasoline prices have taken o

since 2008 and appear poised to continue to escalate due to increasingly limited competitive

alternatives.

Section Summary

Fossil fuel prices are escalating rapidly across the electric, residential, and transportation sectors.

Policy makers can help reduce the exposure to fossil fuel price escalation by providing financial

and policy support for electric vehicle purchases, discounted rates for charging at o-peak times

and extending the electric vehicle charging infrastructure.

And to stay ahead of the growth in the electric demand from electric vehicles, policy makers can

encourage co-investment and a supportive policy environment to accelerate the deployment of

renewable energy resources and the transition to a 100% clean renewable energy future.

FIGURE 17

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

Alaska / US Price Ratio

1970

1974

1978

1982

1986

1990

1994

1998

2002

2006

2010

2014

2018

–

–

–

–

–

–

–

–

–

–

–

–

–

■ Distillate

■ Fuel Oil

■ Jet Fuel ■ Motor Gasoline

[28]

Alaska’s Renewable Energy Future: New Jobs, Aordable Energy

Potential Paths for Renewables to

Replace Fossil Fuels

Former Saudi Oil Minister Sheikh Ahmed Zaki Yamani famously observed (Daily Telegraph, June 25,

2000):

■ “The Stone Age came to an end, not because we had a lack of stones, and the oil age will

come to an end not because we have a lack of oil.”

■ “Oil will remain underground with no buyers in 30 years [2030].”

Indeed, 20 years later as the cost of clean renewable energy continues to decline while the costs

of fossil fuel energy continue to escalate, recent international and national studies highlight the

potential for renewable energy to replace fossil fuels as the primary, if not exclusive, source of

energy by 2050.

Below are highlights of the findings from three studies that were used in the MAFA analysis of

the potential costs and benefits of a transition to 100% clean renewables for Alaska by 2050.

McKinsey & Company, The net-zero transition (January 2022)

■ The Network for Greening the Financial System Net Zero 2050 global scenario would entail

around $275 trillion in cumulative investments over 30 years - around $25 trillion more than

the Current Policies scenario - an increase of 0.3% of the global GDP

55

■ In the Network for Greening the Financial System Net Zero 2050 global scenario, about

200 million direct and indirect jobs would be gained and 185 million lost by 2050 for a net

gain of 15 million jobs

56

■ None of the boroughs in Alaska show up on the list of US counties at high employment risk

in a net zero transition

57

M.Z. Jacobson, Zero Air Pollution and Zero Carbon From All Energy Without Blackouts at Low

Cost in Alaska (December 7, 2021)

58

■ Transitioning Alaska to 100% wind-water-solar (WWS) would create more jobs than lost

■ Save lives from reduced air pollution

■ Eliminate >43 million tonnes-CO2 equivalent per year in 2050

■ Reduces 2050 all-purpose, end-use energy requirements by half

■ Reduces Alaska’s 2050 annual energy costs

■ Reduces annual energy, health plus climate costs

J.H.Williams, et al, Carbon Neutral Pathways for the United States, (12 November 2020)

59

■ The Intergovernmental Panel on Climate Change (IPCC) Special Report on Global Warming

of 1.5°C points to the need for carbon neutrality by mid-century

■ Multiple carbon neutral pathways, including 100% Renewables, met all forecast U.S. energy

needs at a net cost of 0.2–1.2% of GDP in 2050, using only commercial or near-commercial

technologies, and requiring no early retirement of existing infrastructure

■ All pathways employed four basic strategies: energy eciency, decarbonized electricity,

electrification, and carbon capture

[29]

Alaska’s Renewable Energy Future: New Jobs, Aordable Energy

■ Least-cost pathways were based on >80% wind and solar electricity plus thermal generation

for reliability

60

■ We found multiple feasible options for supplying low-carbon fuels for non-electrifiable end

uses in industry, freight, and aviation, which were not required in bulk until after 2035.

■ In the next decade, the actions required in all pathways were similar: expand renewable

capacity 3.5 fold, retire coal, maintain existing gas generating capacity, and increase electric

vehicle and heat pump sales to >50% of market share.

61

Key observations from MAFA’s analysis of the transition to 100% renewable energy by 2050 in

Alaska include:

■ The high cost of fossil fuels in Alaska, including the rapid and continued projected increase

in natural gas prices, accelerate the window in which renewable energy becomes attractive

across the electric and heating sectors in Alaska.

o The relatively higher cost of fossil fuels in the total cost of electricity across Alaska tend

to outweigh the relatively higher capital and operating costs across Alaska [relative to

CONUS cost assumptions used in McKinsey, Jacobson, Williams].

■ The relatively small scale of industrial fuel production plants (H2, Fischer-Tropsch, Liquid

“Synthetic” Fuels) that might be modeled for the domestic Alaska market, not unlike Alaska

in-state petroleum products refineries, tend to driver higher unit costs and, all other things

being equal, increase the cost of 100% renewable fuels by 2050 [relative to potential large

scale plants in Alaska that serve both domestic and transit trac/international markets or

imports from larger scale plants in Canada or CONUS].

[30]

Alaska’s Renewable Energy Future: New Jobs, Aordable Energy

Emerging Opportunities for Decarbonization of Building and

Transportation Sectors

xBUILDING ELECTRIFICATIONx

Building electrification has been incentivized by Alaska utilities with substantial hydroelectric

resources, including AEL&P in Juneau, Kodiak Island Electric Association, AP&T on Prince of Wales

Island, and Sitka.

The Northwest Arctic Borough engaged Analysis North to develop an Alaskan Heat Pump

Calculator to help assess whether a heat pump may be an economic choice for a homeowner and

to compile the results of the application of that model to a wide range of communities and home

energy configurations around the state.

62

The Mini-Split Heat Pumps in Alaska Report concluded:

■ Heat pumps appear competitive in many cases in communities served by home heating oil

or propane.

■ At the then current residential prices for natural gas in the Cook Inlet and Railbelt electric

rates, heat pumps did not appear economically competitive.

When utility prevailing natural gas prices rise into the $15/Mcf range (and residential retail rates

rise toward $1.90/ccf) and electric utilities have migrated to a mix of renewables with residential

electric rates around 20c/kWh, which appears to be a plausible scenario in the 2030-time frame,

building heat pump technology will be competitive with natural gas and poised to quickly capture

market share and grow electric demand.

63

xTRANSPORTATION ELECTRIFICATIONx

Electrifying transportation provides an opportunity to power vehicles and other modes of

transportation with clean energy rather than fossil fuels, thereby reducing carbon emissions. Electric

vehicles (EVs) are a key component of a renewable energy transition. In addition to emissions reductions,

EVs oer health benefits and the future potential to support resilience via power to the grid.

64

In a recent study of the total cost of ownership of electric vehicles for Consumer Reports from

October 2020, the report concluded:

65

■ Both battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEV) are saving

50% on their repair and maintenance costs, when averaged over a typical vehicle lifetime

compared to internal combustion engine (ICE) vehicles.

■ Based on average driving habits, BEVs were estimated to save consumers about 60% on

fuel costs compared to the average ICE vehicles.

■ For all EVs analyzed, the lifetime ownership costs were many thousands of dollars lower

than all comparable ICE vehicles’ costs, with most EVs oering savings of between $6,000

and $10,000.

■ Overall, these results show that the latest generation of mainstream EVs typically cost less

to own than similar gas-powered vehicles, a new development in the automotive industry

with serious potential consumer benefits.

[31]

Alaska’s Renewable Energy Future: New Jobs, Aordable Energy

With the growing interest for EVs in Alaska, the Alaska Center for Energy and Power conducted a

literature review to understand how these vehicles perform in colder weather. The results showed

that EVs generally perform similar to or better than an internal combustion engine in the cold.

66

As of June 2021, Alaska had nearly 1,000 EVs on the road.

67

Currently, there are 62 public level

2 charging plugs and five public direct current fast charging (DCFC) plugs throughout the state.

68

To grow this number, recent funding eorts have been announced. In 2021, the AEA, with support

from the Volkswagen Mitigation Trust Fund and the U.S. Department of Energy’s State Energy

Program, awarded nearly $1 million in grants to add EV charging stations at nine sites along the

state’s backbone highway system.

69

Alaska’s ferry system also presents another opportunity to advance electrification of the

transportation sector. The Infrastructure Investment and Jobs Act will fund at least one program in

Alaska to pilot electric ferries.

70

Electric vehicle purchases and charging have been incentivized and supported by Alaska utilities

with substantial hydroelectric resources including AEL&P and AP&T.

xGREEN HYDROGENBASED FUELSx

Hydrogen gas is anticipated to play a vital role in decarbonization, potentially addressing 30% of

GHG emissions.

71

When the electricity used to electrolyze water and create hydrogen is generated from renewable

energy sources, it is termed “green hydrogen.”

72

A recent comprehensive study from the Columbia Center on Global Energy Policy, Green Hydrogen

in a Circular Economy: Opportunities and Limits, Fan et al., August 2021 has a particularly insightful

set of findings and analysis:

■ Green hydrogen and fuels derived from it, e.g., ammonia, methanol, aviation fuels, can

replace higher carbon fuels in some areas of the transportation sector, industrial sector, and

power sector. They can provide low-carbon heat, serve as low-carbon feedstock, reduce

gas for chemical processes, and act as an anchor for recycling CO2 [executive summary

findings].

■ The cost of green hydrogen is high today, between $6-14/kg on average in most markets

[executive summary findings].

o Dramatic technical improvements in key technologies, e.g., fuel cells and hydrogen

tanks, have stimulated many recent analyses (IEA World Energy Outlook 2021) to see

hydrogen as an essential component of the energy transition, provided its upstream

production and use emit very few greenhouse gases and pollutants [background,

page 16]

o Mean 2030 levelized cost of hydrogen forecasts in the U.S. cluster around $4/kg

[Figure 18].

• With low-cost renewable energy with high capacity factors, the levelized cost

of hydrogen forecasts are as low as $2.30/kg in 2030. These high-quality sites

will likely provide early opportunities to grow green hydrogen and help develop

infrastructure and commercial frameworks [Figure 10 notes].

• See Figure 19 “geographies with resources of high capacity and low cost”

below [opportunities (production), p. 49].

[32]

Alaska’s Renewable Energy Future: New Jobs, Aordable Energy

■ Green hydrogen commercialization is limited by existing infrastructure [executive summary

findings].

■ The governments of Japan, Canada, Australia, Germany, and the EU have published formal

road maps for hydrogen production, use and growth. These plans include subsidies for

manufacturing electrolyzer and fuel cells, port infrastructure, and market aligning policies.

[executive summary findings].

■ Use of green hydrogen and green hydrogen fuels could provide substantial additional

benefits to local economies and environments, including reduction of particulate and sulfur

pollution, maintenance or growth of high-wage jobs, and new export opportunities (fuels,

commodities, and technologies) [executive summary findings].

■ Transportation Market Opportunities for Green Hydrogen

o Medium- and Heavy-Duty Trucks (p. 38)

• Both hydrogen fuel cells and lithium batteries are potential options for

decarbonizing pathways for heavy-duty vehicles. However, batteries are not

practical for many heavy applications for several reasons:

• Batteries have limited range. Hydrogen fuel cells can significantly extend

trucks’ zero emissions range capability to on par with conventional vehicles.

• A typical regional truck haul for trucks of 350 miles requires 16,000

pounds of batteries; the same distance requires 120 pounds of hydrogen

and a 4,000-pound hydrogen storage tank.

• Batteries have long charging times, which for long-haul vehicles could be

hours; by contrast refueling time for hydrogen fuel cell trucks is only 10 to

20 minutes, significantly reducing downtime in a fleet’s daily operations.

• A relatively small number of hydrogen fueling stations at key truck freight hubs

could serve large hydrogen fuel cell powered truck fleets.

o Ships (p. 38-39)

• The global shipping industry currently exclusively uses heavy oil or marine

diesel as fuel. Shipping fuel has a high concentration of sulfur that produces

air polluting chemicals and particulates that are harmful to human health.

These pollutants are concentrated near coastlines where densely populated

communities reside. Changing to cleaner shipping fuels will not only reduce

GHG emissions but also yield significant health benefits, especially to

communities living near ports.

• Similar to medium- and heavy-duty trucks, batteries are impractical for maritime